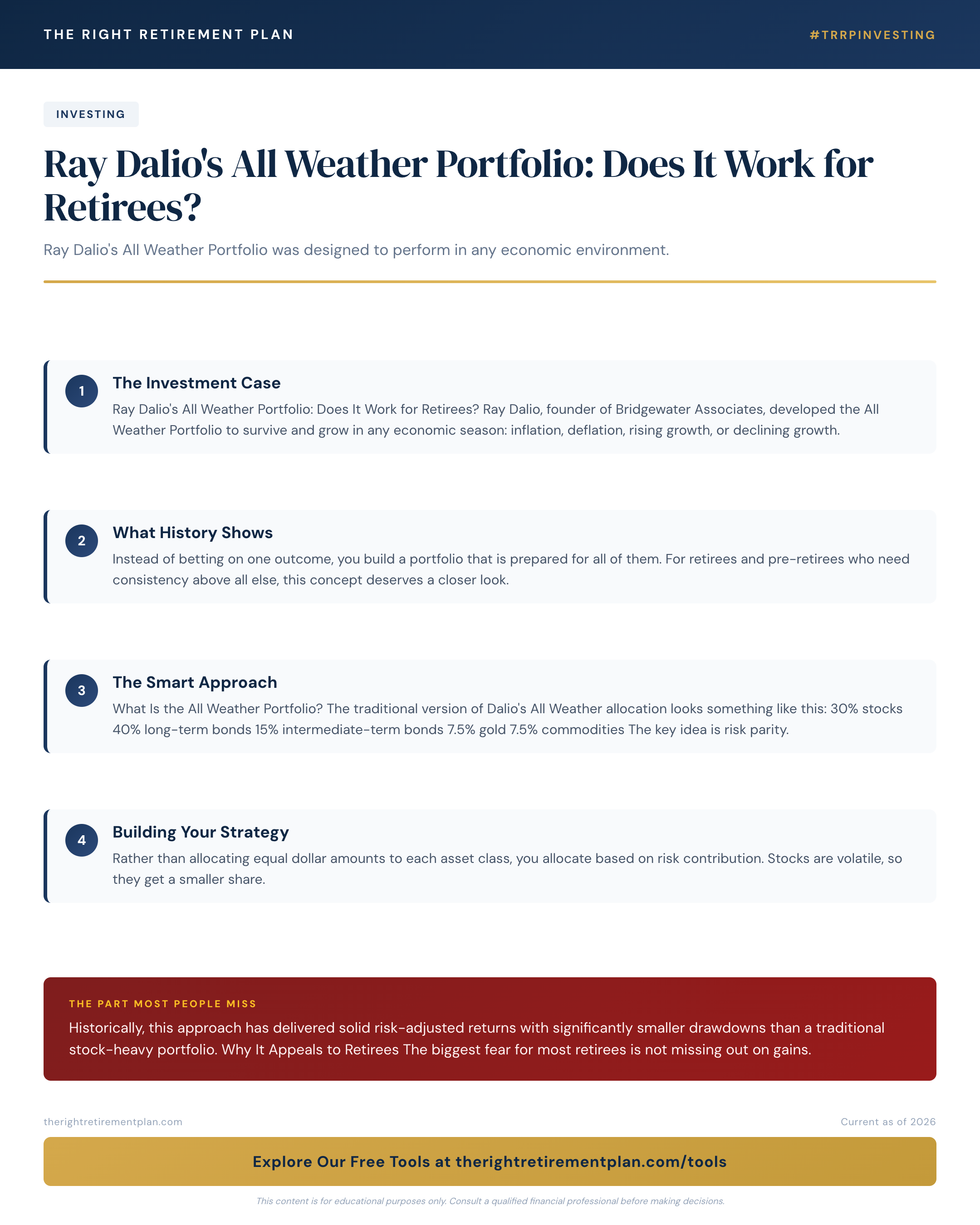

Ray Dalio's All Weather Portfolio: Does It Work for Retirees?

Ray Dalio's All Weather Portfolio was designed to perform in any economic environment. But does a strategy built by one of the world's largest hedge funds translate to the needs of everyday retirees? Here is what you should know before applying risk parity to your retirement savings.