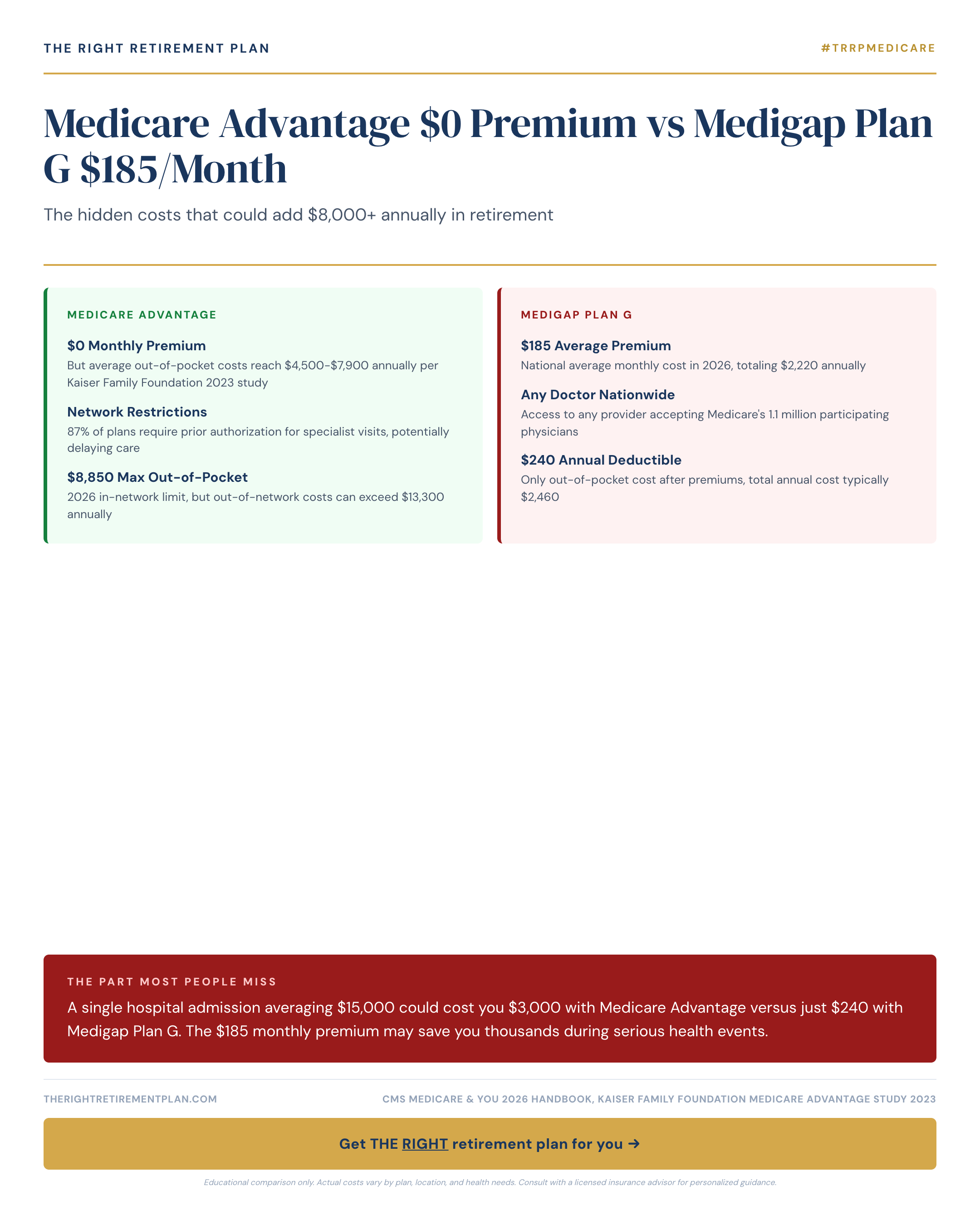

Medicare Advantage $0 Premium vs Medigap Plan G $185/Month

Compare Medicare Advantage $0 premiums to Medigap Plan G's $185/month cost. One hospital stay averaging $15,000 could cost $3,000+ with Medicare Advantage versus just $240 with Plan G.

IRMAA surcharges create income cliffs that can cost high earners over $7,000 more in Medicare premiums, but understanding these thresholds helps Maryland retirees and others plan strategically to avoid costly mistakes.

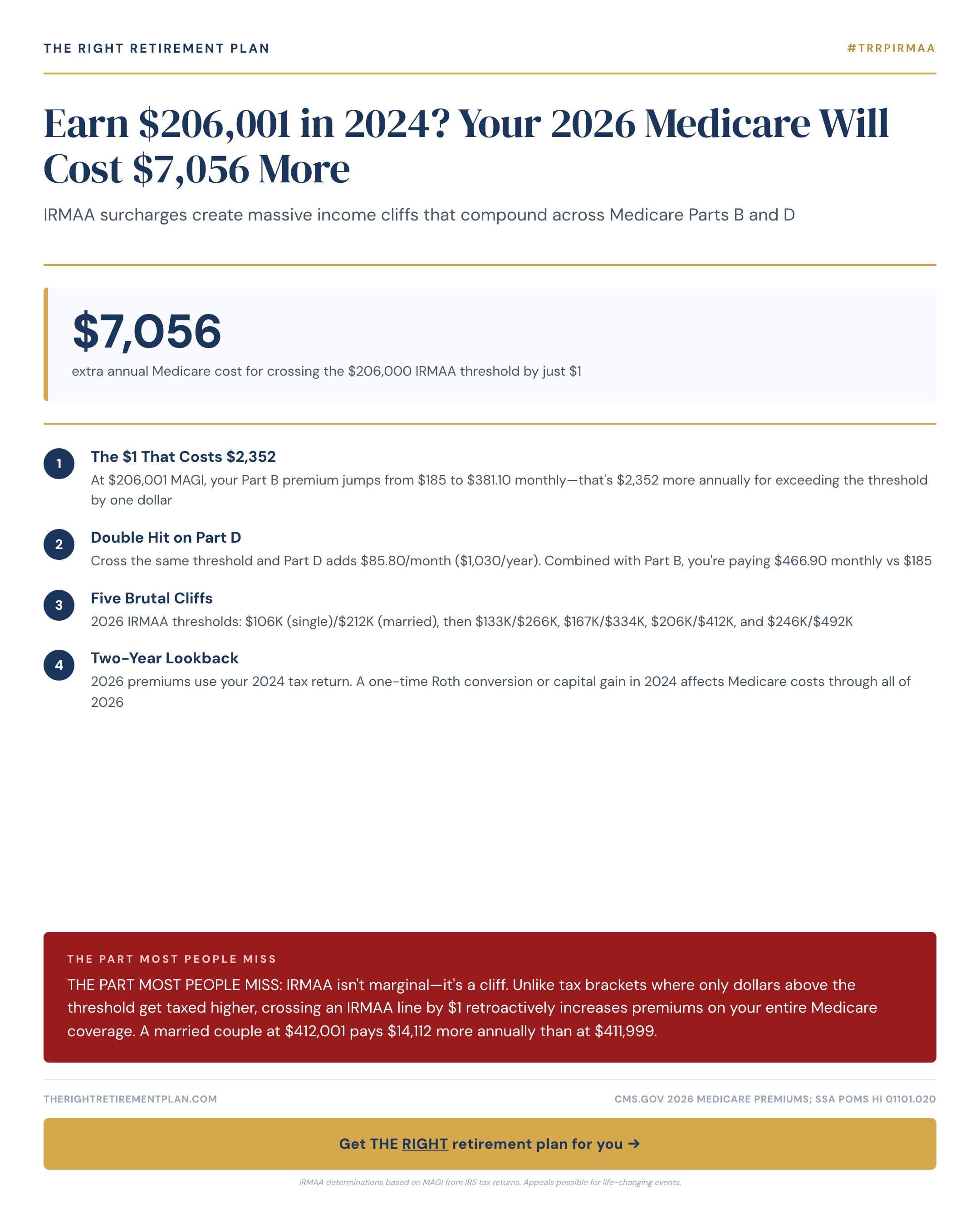

If you earned $206,001 as a married couple filing jointly in 2024, prepare for a shock when your Medicare bills arrive in 2026. The Income-Related Monthly Adjustment Amount (IRMAA) will add $7,056 to your annual Medicare costs compared to someone earning just $2 less.

IRMAA affects Medicare Parts B and D premiums based on your modified adjusted gross income from two years prior. For 2026, the income thresholds create dramatic cost jumps that catch many retirees off guard.

Here's how the 2026 IRMAA brackets work for married couples filing jointly:

• $206,000 or less: Standard Medicare premiums

• $206,001-$258,000: Additional $2,448 annually

• $258,001-$322,000: Additional $6,222 annually

• $322,001-$386,000: Additional $9,996 annually

• $386,001-$750,000: Additional $13,770 annually

• Over $750,000: Additional $15,318 annually

Single filers face similar cliffs at exactly half these amounts.

Unlike tax brackets that only affect income above each threshold, IRMAA creates all-or-nothing cliffs. Cross the line by even $1, and your entire Medicare premium jumps to the higher bracket retroactively.

Consider two Maryland retirees with nearly identical incomes: one couple earns $205,999, while their neighbors in Annapolis earn $206,001. That $2 difference costs the second couple an extra $2,448 per year in Medicare premiums—a 122,400% effective tax rate on those two dollars.

This cliff effect compounds across both Medicare Part B (medical insurance) and Part D (prescription drug coverage), creating substantial financial penalties for crossing income thresholds.

Smart retirement planning can help you avoid these costly IRMAA cliffs:

• Roth conversions: Convert traditional IRA funds to Roth IRAs in lower-income years

• Tax-loss harvesting: Offset gains with investment losses to reduce MAGI

• Timing withdrawals: Coordinate retirement account distributions around IRMAA thresholds

• HSA advantages: Health Savings Account distributions for medical expenses don't count toward IRMAA income

If you want personalized guidance on how IRMAA planning fits into your retirement strategy, consider taking our Retire Ready Score for tailored insights.

Have questions about your specific situation? Take the free Retire Ready Score →

More on medicare from the TRRP editorial team.

Compare Medicare Advantage $0 premiums to Medigap Plan G's $185/month cost. One hospital stay averaging $15,000 could cost $3,000+ with Medicare Advantage versus just $240 with Plan G.

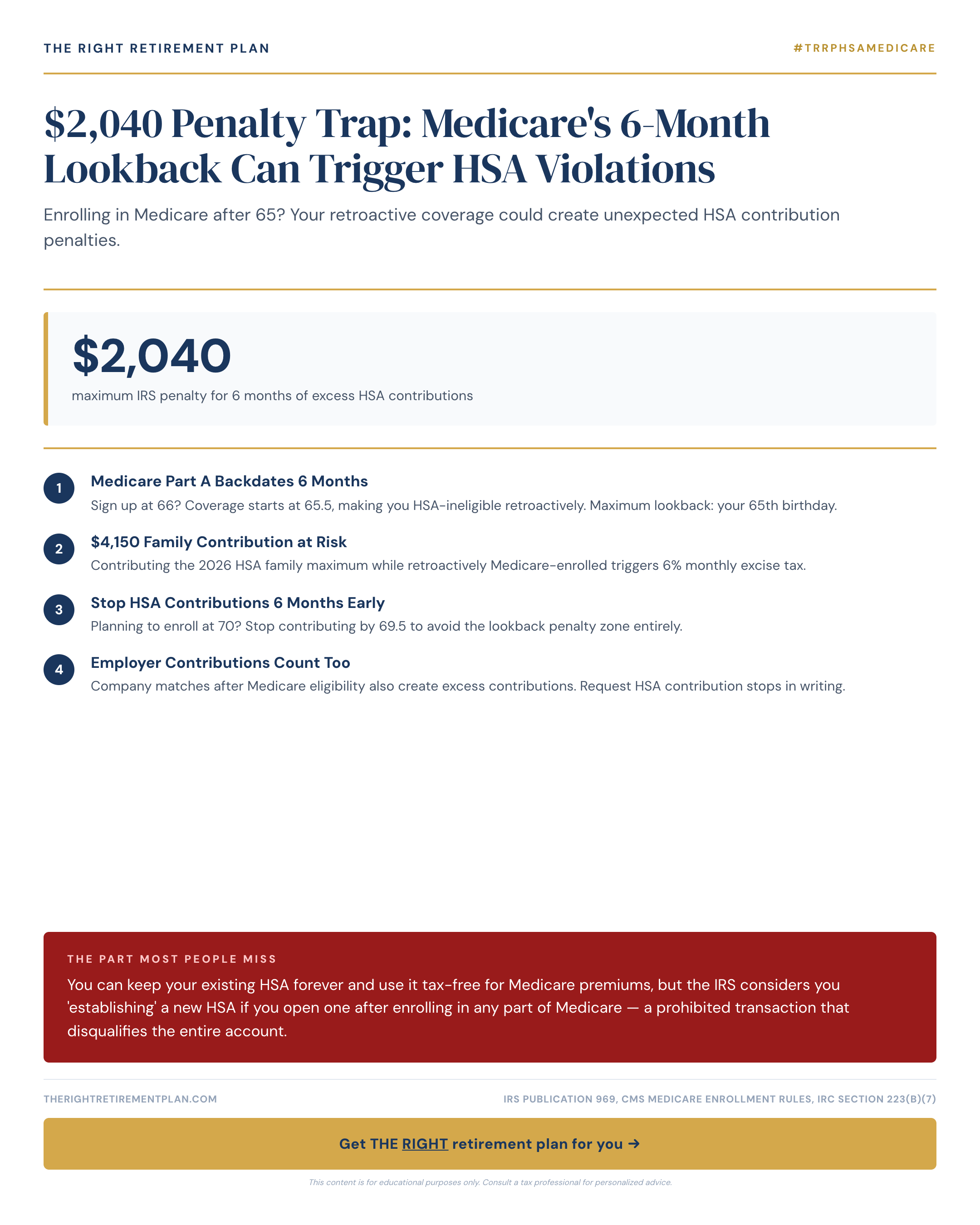

Medicare's 6-month retroactive coverage can invalidate HSA contributions made after age 65, triggering penalties up to $2,040+ annually. Learn how to protect your HSA from this common Medicare enrollment trap.

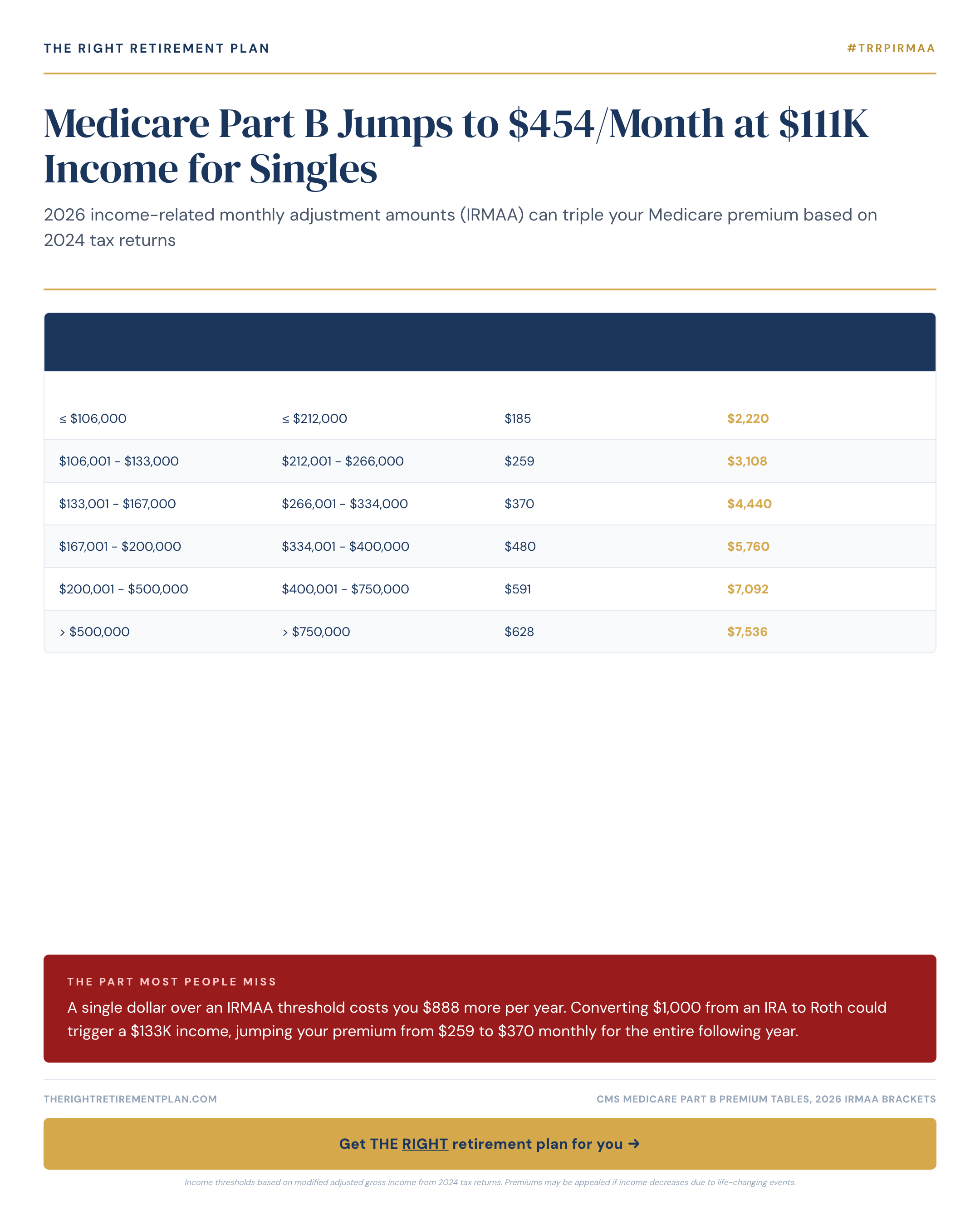

Medicare Part B premiums can jump to $454 monthly in 2026 for singles earning over $111K, based on 2024 tax returns. Understanding IRMAA thresholds helps Maryland retirees avoid costly premium surprises.

Our content gives you the knowledge. A qualified advisor can help you act on it.

Take the Free Assessment