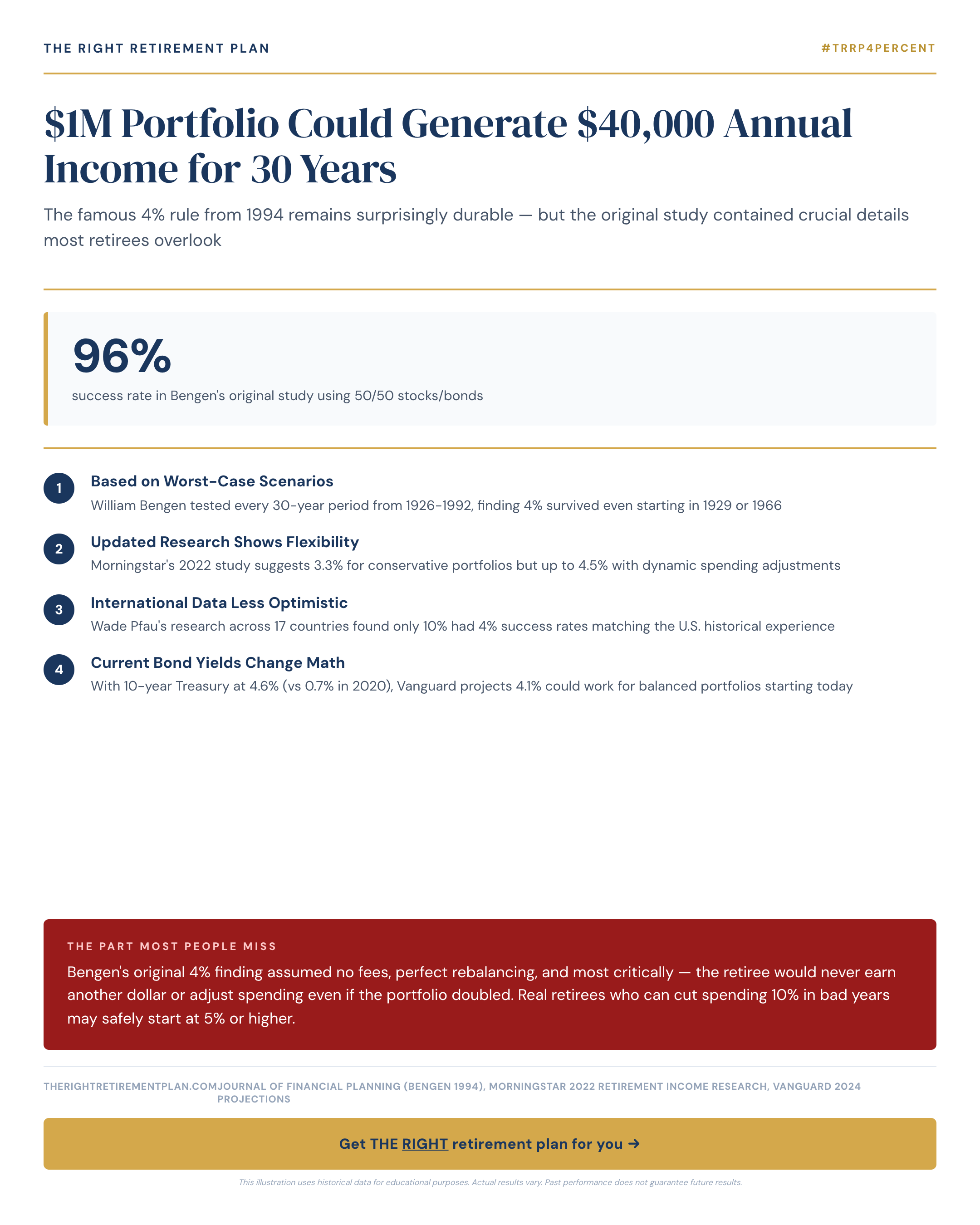

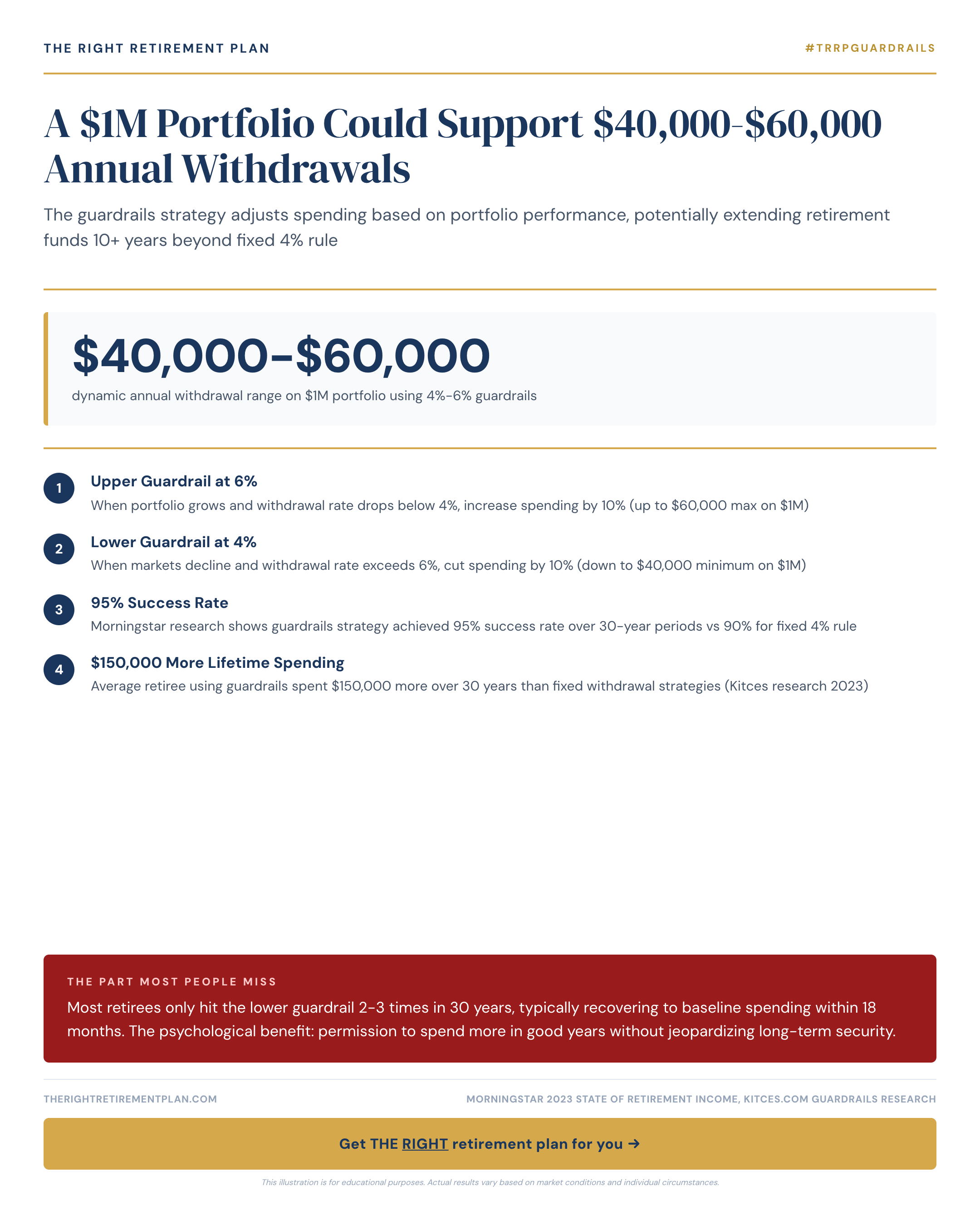

A $1M Portfolio Could Support $40,000-$60,000 Annual Withdrawals

The guardrails strategy lets retirees withdraw $40,000-$60,000 annually from a $1 million portfolio by adjusting spending based on market performance, potentially extending retirement funds 10+ years beyond the traditional 4% rule.