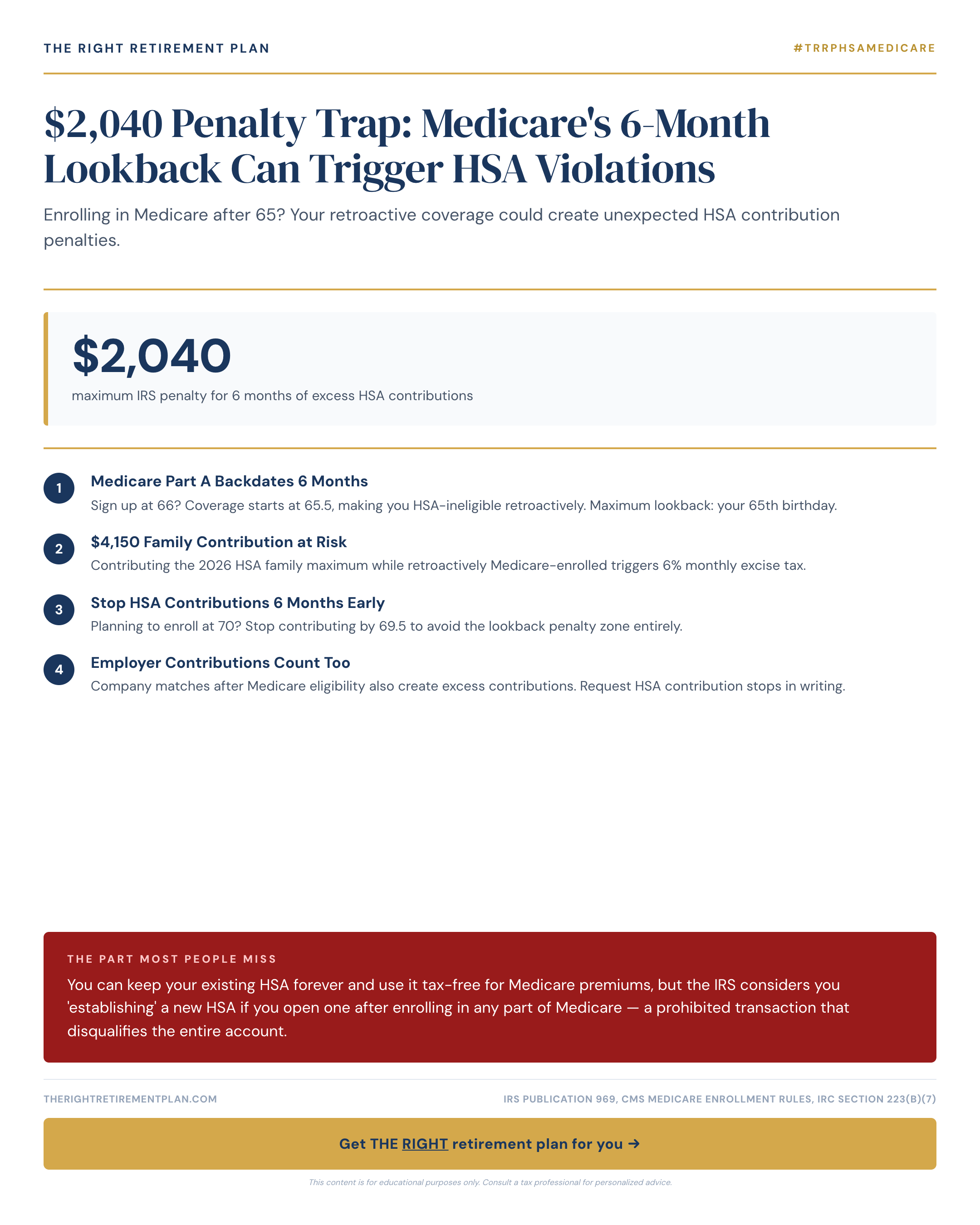

You've been building your Health Savings Account for years, then turn 65, delay Medicare because you're still working, and keep contributing to your HSA. What you don't realize? A single Medicare enrollment decision could trigger a $2,040+ annual penalty and potentially disqualify your entire account.

The culprit is Medicare's six-month retroactive coverage rule. When you enroll in Medicare Part A after age 65, coverage automatically backdates up to six months. Since the IRS prohibits HSA contributions during any month you have Medicare coverage—even retroactively—those contributions become "excess" and subject to penalties.

How Medicare's Lookback Creates HSA Violations

When you enroll in Medicare Part A after 65, the Social Security Administration automatically backdates your coverage up to six months, but no earlier than when you turned 65. This retroactive coverage isn't optional—it's built into Medicare's design.

Here's the conflict: IRS rules state you cannot contribute to an HSA for any month you have Medicare coverage. The IRS doesn't care that you didn't know you were covered retroactively.

Consider this example:

- John turns 65 in March 2026 but keeps working with employer coverage

- He continues HSA contributions through September 2026

- He enrolls in Medicare Part A in October 2026

- Medicare backdates his coverage to April 2026 (six months)

- His HSA contributions from April through September are now excess contributions

For 2026, maximum HSA contributions for those 55+ are $4,300 (individual) or $8,550 (family), plus a $1,000 catch-up contribution. Six months of family coverage contributions could total $4,775 in excess contributions.

The penalties compound quickly:

- 6% excise tax annually on excess contributions until corrected

- Potential income tax on withdrawn excess amounts

- Loss of tax deduction for those contributions

Who Faces the Highest Risk

Working Past 65

You're still employed with group health insurance and maximizing HSA contributions. When you retire and enroll in Medicare, the lookback invalidates months of contributions. About 19% of workers 65+ continue with employer coverage, creating significant exposure.

Delayed Social Security Claims

If you're not receiving Social Security at 65, you won't auto-enroll in Medicare. But claiming Social Security benefits after 65 typically triggers Medicare Part A enrollment—with retroactive coverage attached.

Premium-Free Part A Qualifiers

Most people qualify for "free" Medicare Part A. But that zero-cost coverage becomes expensive if you've been contributing to an HSA, since the six-month lookback applies regardless of premiums.

Calculating and Correcting Excess Contributions

For 2026, potential six-month excess contributions:

- Individual coverage (55+): $2,650

- Family coverage (55+): $4,775

Correction options:- Withdraw before tax deadline: Remove excess contributions plus earnings to avoid the 6% excise tax

- Pay ongoing penalties: 6% annually on excess amounts until corrected (that's $287 yearly on $4,775)

- File Form 5329: Required to report excess contributions and excise taxes

Maryland retirees and others in the Mid-Atlantic often discover this issue when preparing taxes, making timely correction crucial.

Action steps:

- Stop HSA contributions at least six months before planned Medicare enrollment

- If working past 65, delay both Medicare AND Social Security to preserve HSA eligibility

- Monitor enrollment deadlines to avoid late-enrollment penalties

If you want personalized guidance on coordinating Medicare timing with your retirement accounts, consider taking our Retire Ready Score assessment for tailored recommendations.