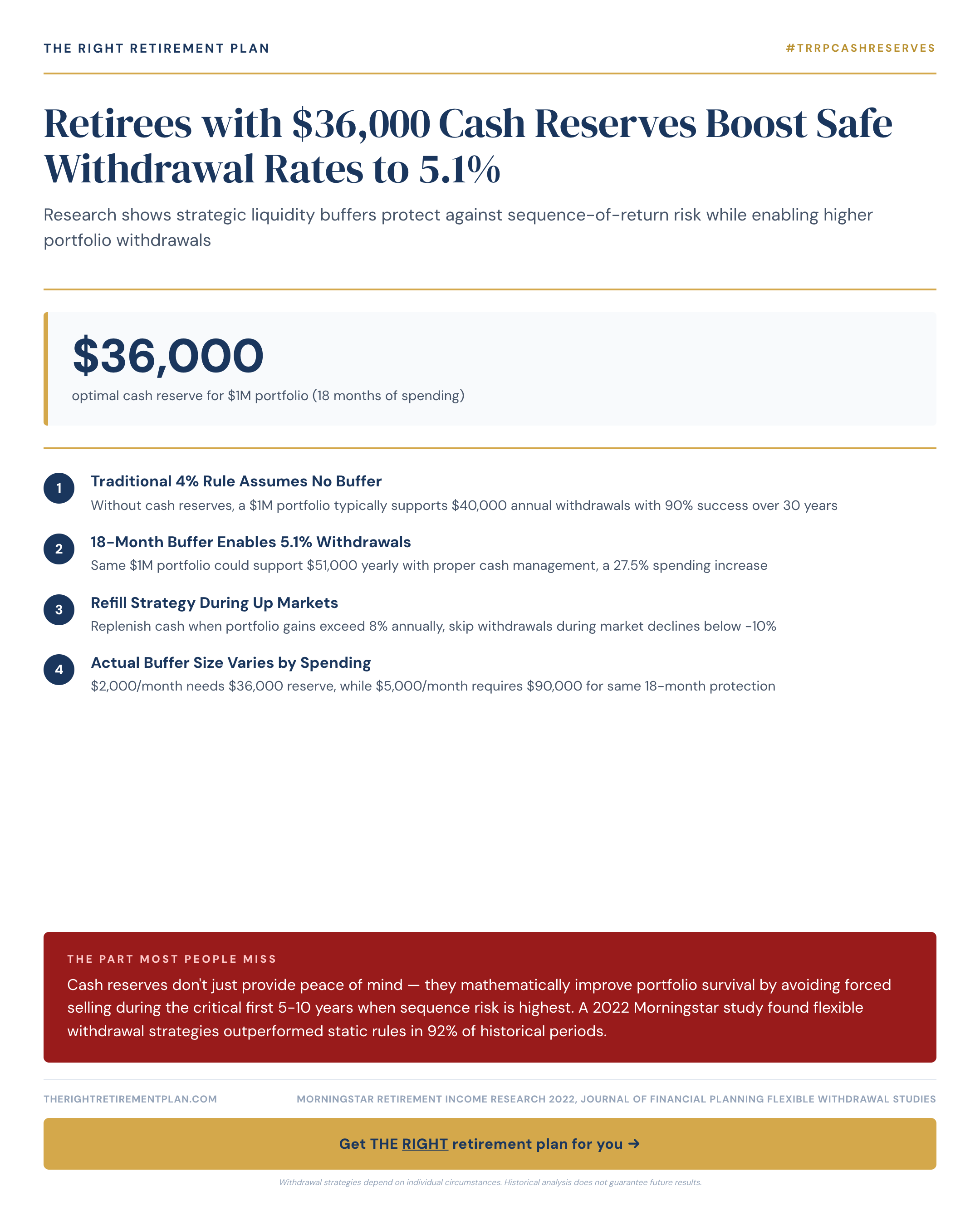

Most retirees think cash reserves are "dead money" earning minimal returns. But research reveals a stunning truth: maintaining strategic cash buffers can mathematically increase your safe withdrawal rate from 4% to 5.1%, adding $7,920 annually to spending from a $720,000 portfolio.

The secret lies in protecting against sequence-of-return risk—the danger that market downturns early in retirement force you to sell investments at the worst possible time.

Why Cash Buffers Beat the 4% Rule

The traditional 4% withdrawal rule assumes you'll stick to a rigid schedule regardless of market conditions. But Morningstar's 2022 retirement study found that flexible withdrawal strategies, including cash buffer approaches, outperformed static rules in 92% of historical periods.

Here's the math that matters: two retirees with identical $720,000 portfolios and 7% average returns can have drastically different outcomes based solely on when market downturns occur.

Retiree A (bad returns early): Portfolio depleted by year 22

Retiree B (bad returns late): Portfolio worth $340,000 at year 30

When you withdraw from a falling portfolio, you're selling more shares to generate the same income. Those shares never participate in recovery. Cash reserves break this destructive cycle by providing a "bridge" during downturns.

The Federal Reserve's Survey of Consumer Finances shows median retiree households hold only $12,400 in liquid savings—leaving most dangerously exposed to sequence risk.

Calculating Your Optimal Cash Buffer for 2026

Your ideal cash reserve isn't a random number—it's 18-24 months of essential expenses minus guaranteed income sources.

Step-by-step calculation:

- Essential monthly expenses (housing, utilities, food, healthcare)

- Subtract Social Security (average 2026 benefit: $1,976/month)

- Subtract any pension income

- Multiply remaining gap by 18-24 months

Example for Maryland retirees:- Essential expenses: $4,500/month

- Social Security: $2,200/month

- Monthly gap: $2,300

- Cash buffer needed: $41,400-$55,200

For 2026, remember Medicare Part B premiums are $185 monthly, with IRMAA surcharges if your income exceeds $106,000 (single) or $212,000 (married filing jointly).

Where to hold your cash:

- High-yield savings accounts (4.5-5.0% APY)

- Short-term Treasury bills (26-week T-bills yielding ~4.3%)

- Money market funds within brokerage accounts

Avoid CDs with early withdrawal penalties—accessibility during market stress is the entire point.

Tax Advantages You're Probably Missing

Cash buffers create powerful tax optimization opportunities during market downturns. While others are forced to realize gains for living expenses, you can:

- Harvest capital losses to offset future gains

- Execute Roth conversions at depressed asset values

- Manage tax bracket positioning strategically

2026 tax brackets for reference:

- Single filers: 12% bracket ends at $48,475, 22% bracket ends at $103,350

- Married filing jointly: 12% bracket ends at $96,950, 22% bracket ends at $206,700

The Employee Benefit Research Institute estimates tax-efficient withdrawal sequencing adds 0.5-1.0% annually in after-tax returns—benefits that compound over decades.

Vanguard research shows retirees with adequate cash buffers are 73% less likely to panic-sell during market corrections. The behavioral benefit may matter more than the mathematical advantage. Retirees who run out of money rarely do so because their portfolio earned 6% instead of 7%—they run out because they sold at the worst possible time and never recovered.

A $36,000 cash buffer may be the cheapest insurance against portfolio destruction you'll ever find. For advisors in the Annapolis area and nationwide, this strategy represents a fundamental shift from viewing cash as portfolio drag to recognizing it as withdrawal rate enhancement.

If you'd like personalized guidance on sizing your cash reserves and optimizing your withdrawal strategy, consider taking our Retire Ready Score to identify potential gaps in your retirement income plan.