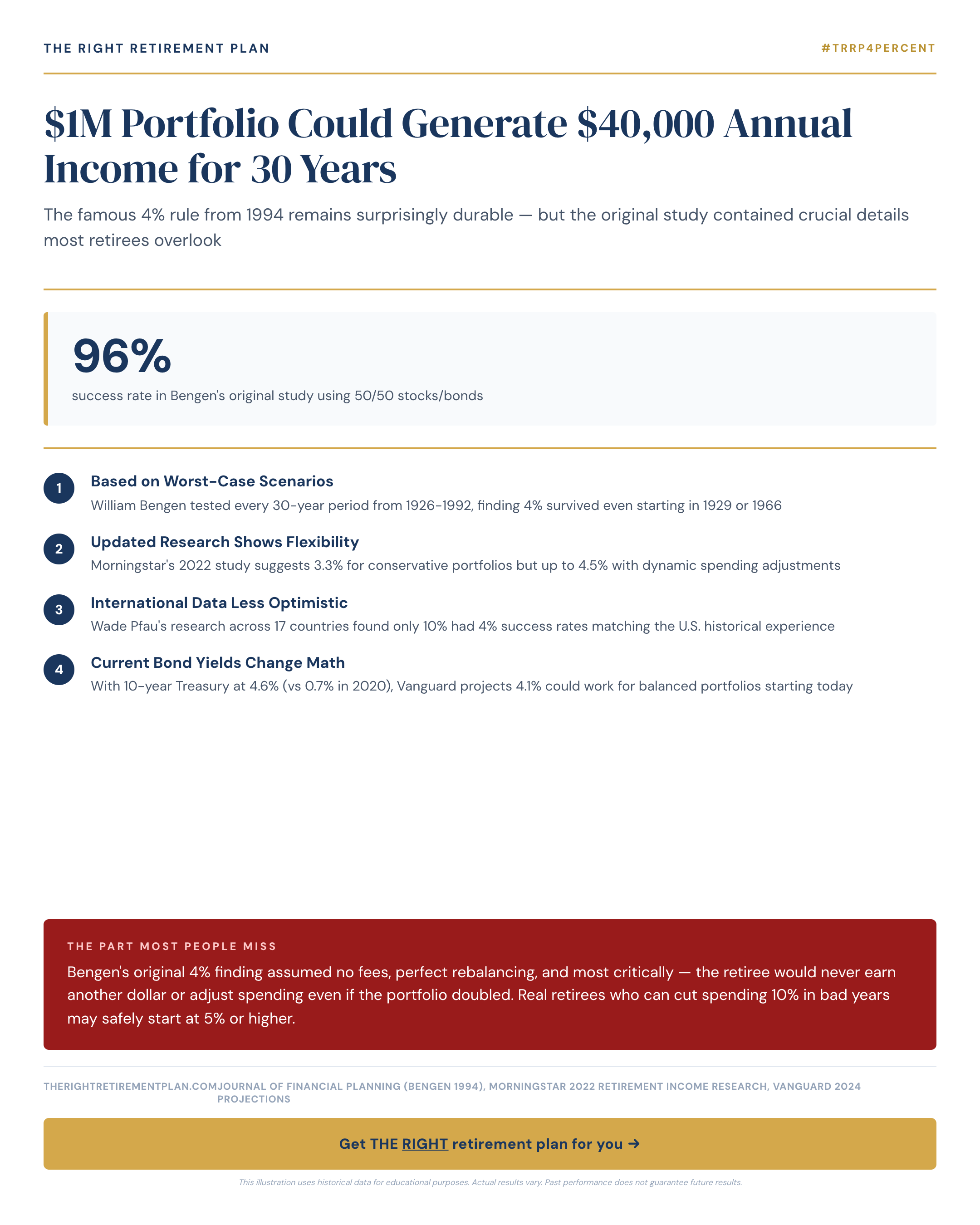

The famous 4% retirement withdrawal rule suggests that a $1 million portfolio could safely generate $40,000 in annual income for 30 years. This guidance, developed by financial planner William Bengen in 1994, remains one of the most cited strategies in retirement planning. But here's what most people don't realize: the original study contained critical assumptions that dramatically affect how the rule works in practice.

Understanding the Original 4% Study

Bengen's research made several key assumptions that rarely match real-world retirement scenarios. The study assumed zero investment fees, perfect annual rebalancing, and most importantly — that retirees would never adjust their spending regardless of market conditions.

The original framework also assumed retirees would never earn another dollar after retirement. No part-time work, no Social Security adjustments, no pension income. For many Maryland retirees and others approaching retirement, this assumption feels unrealistic.

Perhaps most significantly, the study assumed retirees would maintain the exact same spending level even if their portfolio doubled in value. This rigid approach doesn't reflect how most people actually behave during retirement.

Real-World Flexibility Changes Everything

Modern retirement income planning research shows that retirees who maintain some flexibility can often start with higher withdrawal rates. Those willing to reduce spending by 10% during market downturns may safely begin with 5% or even higher initial withdrawals.

Consider these practical adjustments:

- Reducing discretionary spending during bear markets

- Taking advantage of part-time work opportunities

- Optimizing Social Security claiming strategies

- Adjusting withdrawal timing based on market conditions

Geographic factors matter too. Retirees in areas like Annapolis often have different cost structures and income opportunities compared to other regions, which can impact safe withdrawal calculations.

Building Your Personalized Strategy

Sustainable retirement withdrawals require more than following a single rule. Consider your complete financial picture: Social Security benefits, pension income, healthcare costs, and your willingness to adjust spending during challenging market periods.

The key is understanding that retirement decisions compound over time. Getting withdrawal strategy wrong can cost tens of thousands of dollars across a 30-year retirement. However, most mistakes are completely avoidable when you understand how flexible withdrawal strategies actually work in practice.

If you want personalized guidance on how these principles apply to your specific situation, consider taking our Retire Ready Score for tailored insights.