How QCDs Save You Money

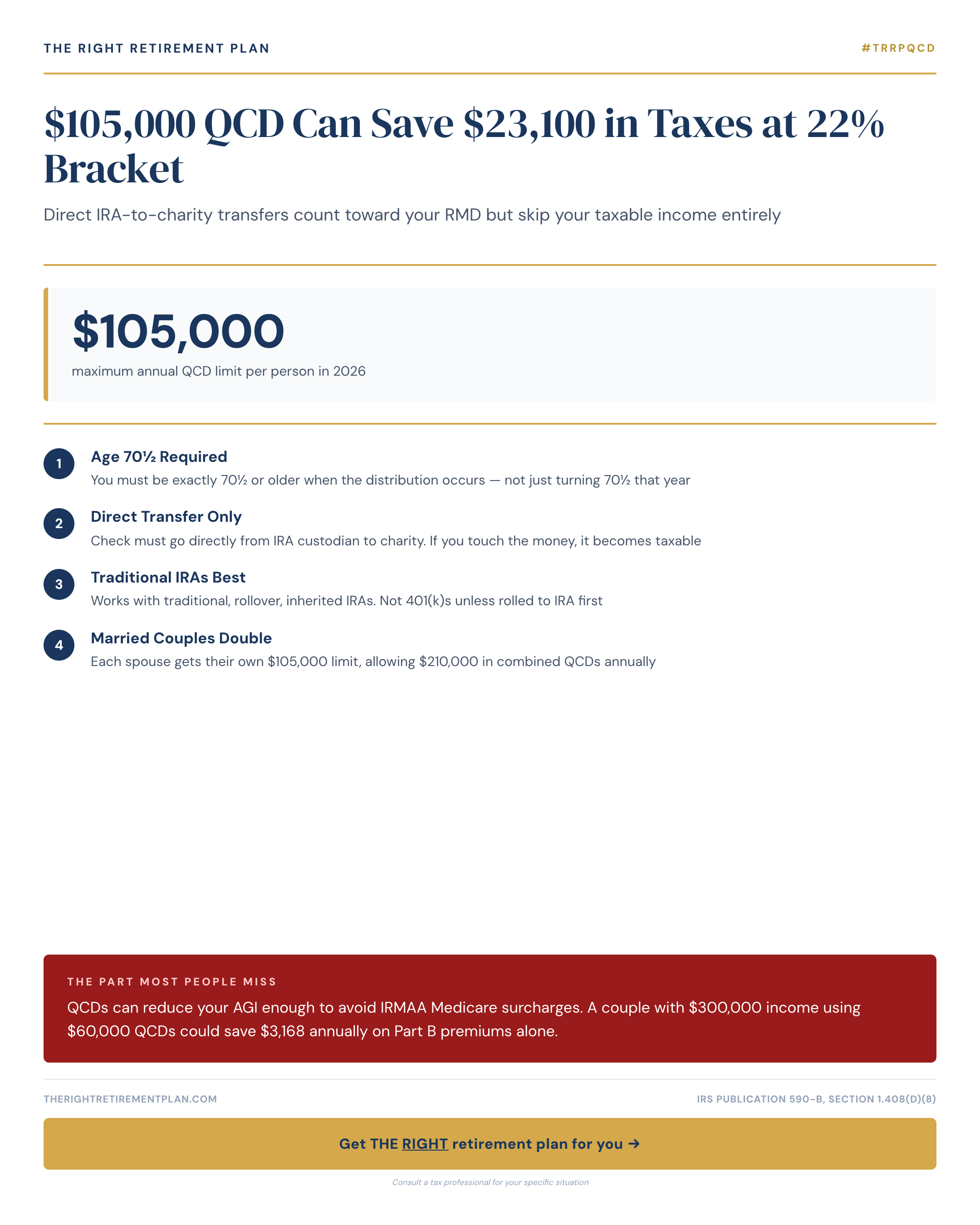

A Qualified Charitable Distribution (QCD) allows you to transfer up to $105,000 directly from your IRA to charity in 2026, satisfying your Required Minimum Distribution without adding to your taxable income. This powerful strategy can generate significant tax savings for charitable-minded retirees.

Here's the math: If you're in the 22% tax bracket and donate $105,000 through a QCD instead of taking a regular distribution, you'll save approximately $23,100 in federal taxes. That's money that stays in your pocket instead of going to the IRS.

The beauty of qualified charitable distributions lies in their simplicity. The transfer goes directly from your IRA custodian to the qualified charity, bypassing your tax return entirely. You still get the satisfaction of supporting causes you care about, but without the tax hit of a traditional distribution.

The Medicare Premium Connection

Beyond direct tax savings, QCDs offer another valuable benefit: Medicare IRMAA avoidance. When you reduce your adjusted gross income through charitable distributions, you may avoid or minimize Medicare's Income-Related Monthly Adjustment Amount surcharges.

Consider a Maryland couple with $300,000 in retirement income. By using $60,000 in QCDs, they could:

- Lower their AGI to $240,000

- Avoid higher Medicare Part B premium brackets

- Save approximately $3,168 annually on Part B premiums alone

- Potentially save on Part D prescription drug premiums too

These Medicare savings compound year after year, making the total benefit far greater than just the immediate tax reduction. For Annapolis-area retirees managing substantial retirement accounts, this strategy becomes even more valuable as IRMAA thresholds remain relatively low.

Key Requirements and Limitations

To qualify for QCD treatment, you must:

- Be age 70½ or older when making the distribution

- Transfer funds directly from your IRA to a qualified 501(c)(3) organization

- Ensure the charity provides proper acknowledgment

- Stay within the annual $105,000 limit per person ($210,000 for couples)

The distribution cannot go to a donor-advised fund or supporting organization, and you cannot receive any goods or services in return.

If you'd like personalized guidance on how charitable distributions might fit into your retirement plan, consider taking our Retire Ready Score for a comprehensive assessment.