How State Tax Residency Really Works

When planning your retirement move from high-tax states like California, New York, or here in Maryland, understanding state tax residency rules becomes critical. The infamous "183-day rule" isn't just about counting days—it's about avoiding potentially devastating tax consequences that could cost you six figures.

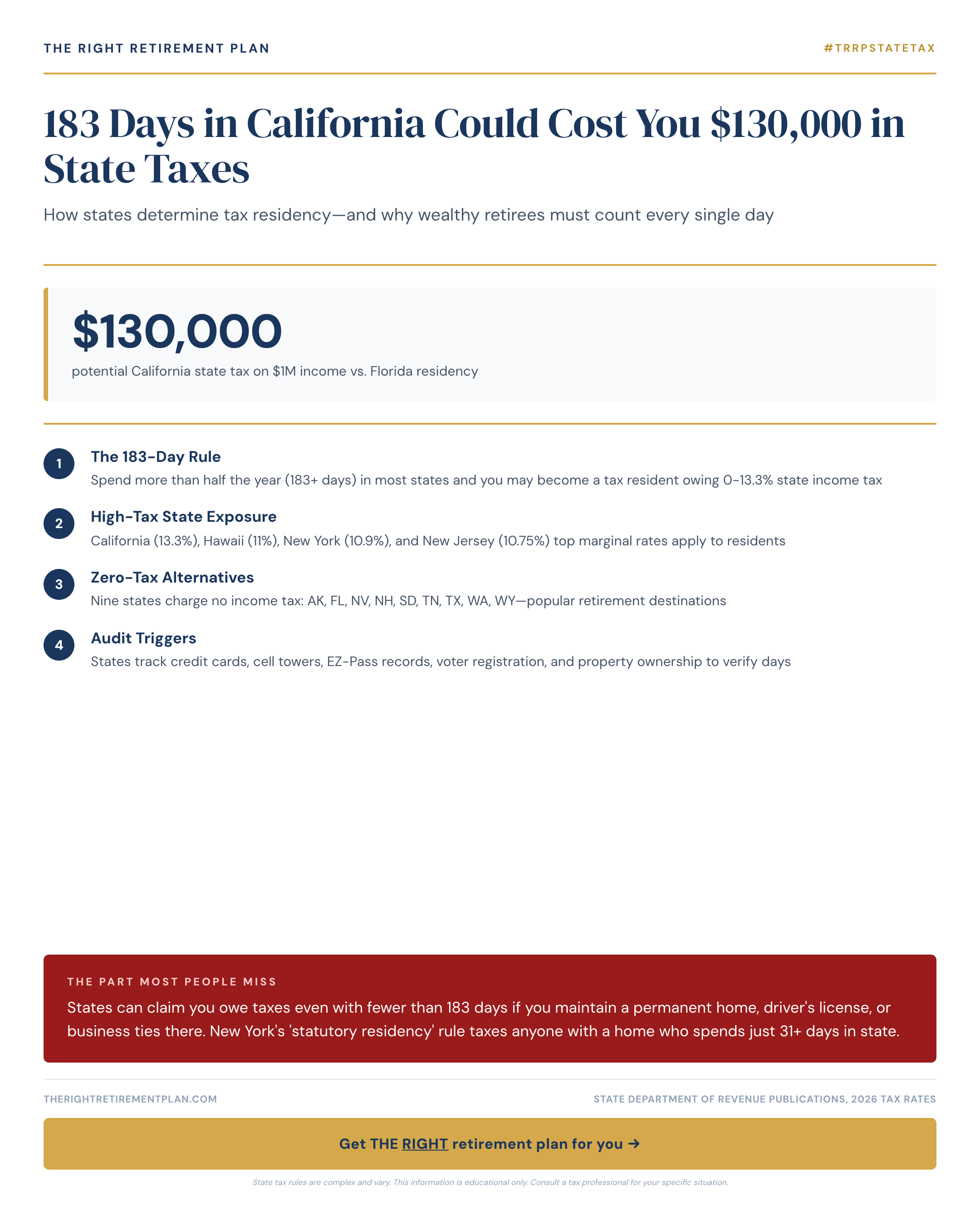

California determines tax residency through a combination of factors. If you spend 183 or more days in the state during any tax year, you're automatically considered a resident for tax purposes. But here's what catches many retirees off-guard: states can still claim you owe taxes with fewer than 183 days if you maintain other ties.

These ties include keeping a permanent home, California driver's license, voter registration, or significant business connections. For a retiree with substantial income from investments, pensions, or retirement account withdrawals, this could mean paying California's top tax rate of 13.3% on your entire income—not just California-sourced earnings.

The New York Trap and Other State Pitfalls

New York's "statutory residency" rule is even more aggressive. If you maintain a permanent place of abode in New York and spend just 31 days or more in the state, you're considered a resident for tax purposes. This catches many retirees who keep their family home while spending most of their time in Florida.

Other states have their own variations. Some focus on where your primary residence is located, while others look at where you conduct business or maintain professional licenses. Retirement tax planning requires understanding these nuances before you make your move.

For high-income retirees, the financial impact is substantial. Consider someone with $1 million in annual retirement income moving from California to Nevada. California's 13.3% rate versus Nevada's 0% state income tax creates a potential $133,000 annual difference—money that could fund years of retirement lifestyle.

Creating a Clean Break

Successfully changing your state residency for retirees requires methodical planning. This includes updating your driver's license, voter registration, and will within the first few months of your move. Establish new banks, doctors, and service providers in your new state. Most importantly, maintain detailed records of your whereabouts—many successful retirees keep a simple daily log.

Maryland retirees considering moves to tax-friendly states like Florida, Tennessee, or Texas should start this process at least a year before their planned relocation date. Small oversights in timing or documentation can result in dual residency claims that take years and significant legal fees to resolve.

If you want personalized guidance on how state tax residency rules might affect your specific retirement situation, consider taking our Retire Ready Score assessment.