Understanding the 10-Year Rule for Inherited IRAs

The SECURE Act fundamentally changed how non-spouse beneficiaries handle inherited IRAs. Instead of stretching distributions over their lifetime, inherited IRA beneficiaries must now empty the entire account within 10 years of the original owner's death.

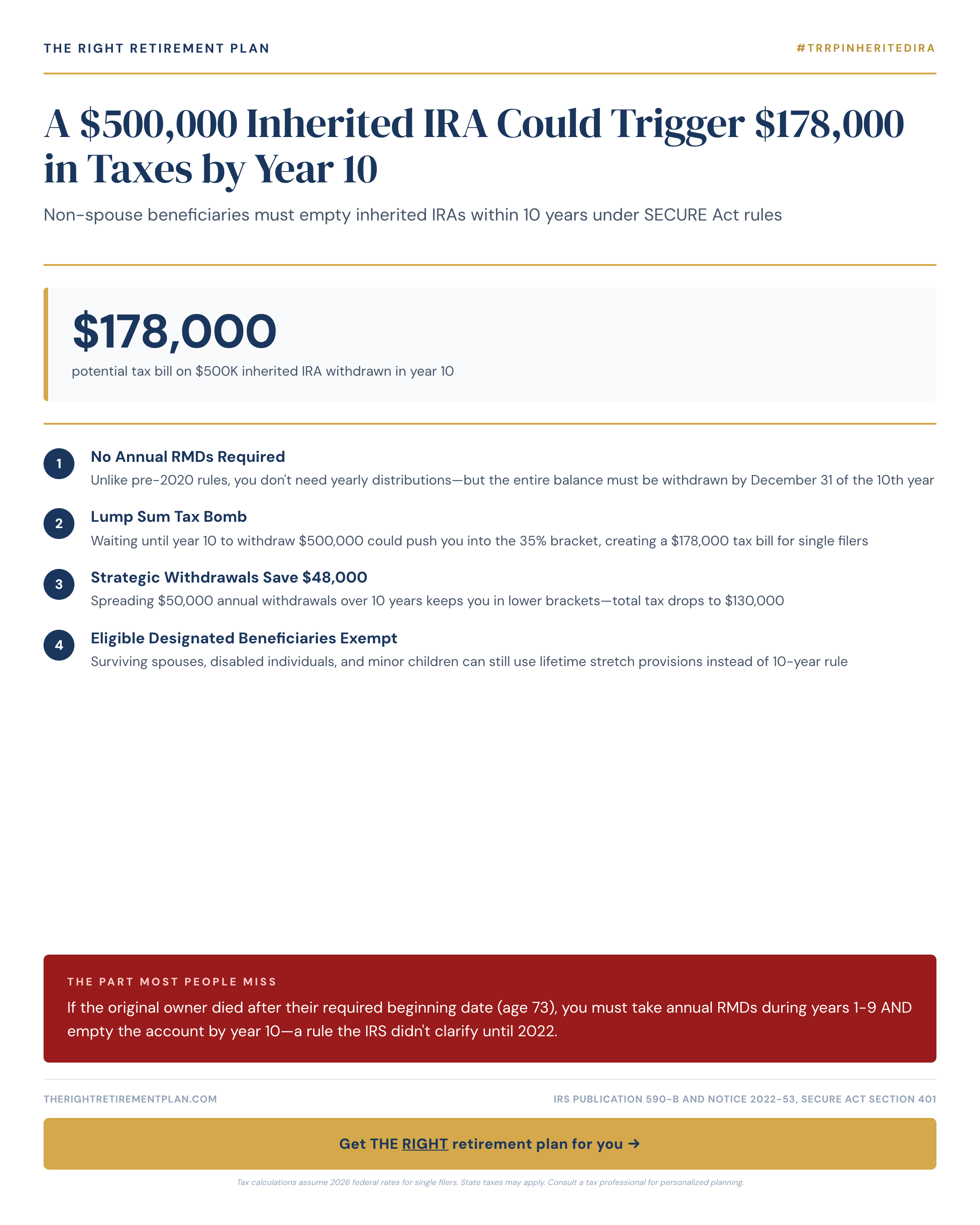

Here's where it gets costly: that $500,000 inheritance doesn't just trigger taxes once. If you're forced to take large distributions, you could push yourself into higher tax brackets year after year. A beneficiary in the 24% bracket taking $50,000 annually would pay $12,000 in federal taxes each year—$120,000 over the decade. Add state taxes, and Maryland residents could see total taxes approaching $178,000.

The Hidden RMD Requirement Most People Miss

The IRS threw a curveball that many financial advisors missed initially. If the original IRA owner died after their required beginning date (age 73 in 2026), beneficiaries face a double requirement:

- Take annual required minimum distributions (RMDs) in years 1 through 9

- Empty the remaining balance by December 31 of year 10

For inherited traditional IRAs, every dollar withdrawn gets taxed as ordinary income. Without careful planning, beneficiaries often find themselves paying far more in taxes than necessary.

Smart Strategies to Minimize the Tax Hit

The key is managing your tax brackets strategically across the 10-year period. Consider these approaches:

- Roth conversions: Convert portions of the inherited traditional IRA to a Roth IRA during low-income years

- Income timing: Coordinate distributions with retirement, lower-earning years, or tax-loss harvesting

- Split distributions: Take larger amounts in years when you're in lower brackets

If you've inherited an IRA or want to better understand how these rules might affect your family's financial plan, consider taking our Retire Ready Score for personalized guidance on your retirement strategy.