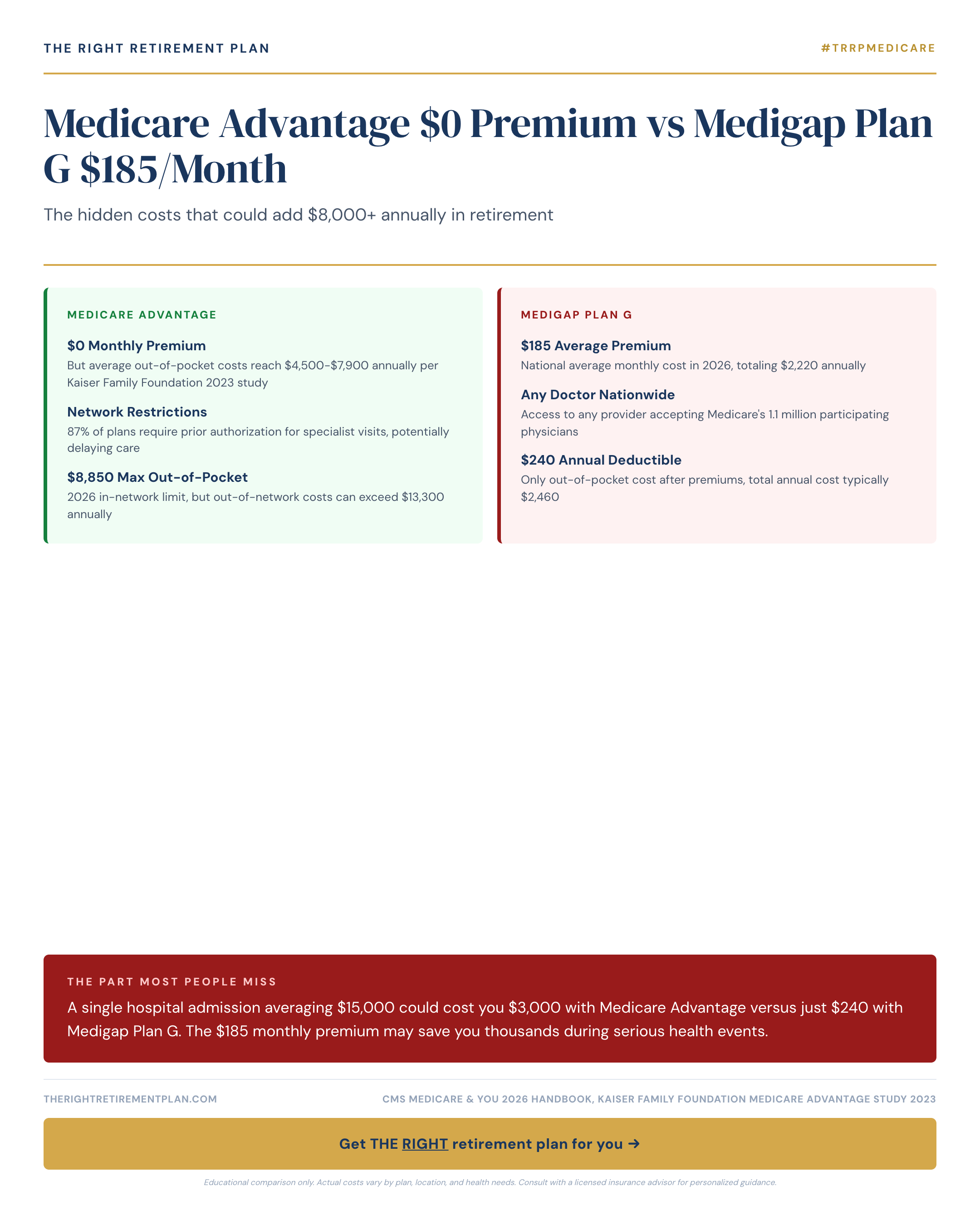

That $0 premium Medicare Advantage plan looks appealing—no monthly cost, often includes dental and vision, maybe even a gym membership. Meanwhile, Medigap Plan G wants $185 every month, or $2,220 annually, just for supplemental coverage.

The math seems obvious until you end up in the hospital.

How One Hospital Stay Changes Everything

A single inpatient admission averaging $15,000 could cost you roughly $3,000 out-of-pocket with many Medicare Advantage plans. That same stay with Medigap Plan G? Approximately $240—just the Part B deductible for 2026.

The premium you thought you were saving vanishes in a single health event, potentially with thousands more following it out the door.

For the 65 million Americans on Medicare, this choice represents one of retirement's most consequential healthcare decisions. According to the Kaiser Family Foundation, roughly 51% of Medicare beneficiaries now choose Medicare Advantage, up from 19% in 2007. But enrollment popularity doesn't necessarily mean it's the right choice for your situation.

Breaking Down the Real Costs

Medicare Advantage replaces Original Medicare entirely. Private insurers contract with CMS to provide at least the same benefits as Parts A and B, typically adding prescription drug coverage and extras. The trade-off: you generally must use network providers and face cost-sharing through copays and deductibles.

For 2026, CMS allows Medicare Advantage plans to set maximum out-of-pocket limits up to $8,850 for in-network services. Many plans set lower limits, but the national average hovers around $5,000–$6,000.

Medigap Plan G works differently. You keep Original Medicare as primary coverage and add standardized supplement insurance to cover gaps. Plan G covers:

- Part A hospital coinsurance and deductible ($1,676 for 2026)

- Part B coinsurance (the 20% you'd otherwise owe)

- Skilled nursing facility coinsurance

- Blood costs and hospice coinsurance

- 80% of foreign travel emergency coverage

The only remaining gap: the annual Part B deductible of $240 for 2026. After that, Plan G typically covers everything Original Medicare approves at 100%.

Let's follow a real scenario: a 68-year-old Maryland retiree admitted for pneumonia requiring five days of hospitalization. Medicare-approved charges total $15,000.

With a typical Medicare Advantage plan, common cost-sharing might include:

- Hospital copay: $350–$500 per day for days 1–5

- Physician services copay during stay

- Various ancillary service fees

This often results in $2,500–$4,000 out-of-pocket for this single admission. With Medigap Plan G, the patient pays only the $240 Part B deductible if not already met for the year.

Beyond Hospital Stays: Other Critical Factors

Network restrictions matter significantly. Medicare Advantage plans typically require in-network providers, with exceptions for emergencies. Original Medicare with Medigap allows you to see any provider nationwide who accepts Medicare—approximately 93% of non-pediatric physicians.

Prior authorization requirements can create delays. A 2022 HHS Office of Inspector General report found that 13% of prior authorization denials in Medicare Advantage plans were for services that actually met Medicare coverage rules.

Prescription drug coverage adds complexity. Medicare Advantage often bundles Part D drug coverage, while Medigap requires purchasing separate Part D coverage, adding $15–$100+ monthly depending on your medications.

Premium trajectory varies between options. Both can increase annually, but Medigap policyholders own their policy and cannot be dropped for health reasons.

The $2,220 annual premium for Plan G suddenly looks different when one moderate health event could cost $3,000+ with Medicare Advantage. For retirees managing chronic conditions or those who value predictable healthcare costs, the math often favors Medigap's comprehensive coverage approach.

If you're weighing these Medicare options as part of your broader retirement planning, consider taking our Retire Ready Score for personalized guidance on how healthcare decisions fit into your overall financial picture.