Most retirees think Roth IRA contributions stop at $8,000 annually for those over 50 in 2026. Yet wealthy investors routinely convert $500,000 or more to Roth accounts each year without limits. Here's how the Roth conversion strategy works—and the costly rule that trips up most people.

How Unlimited Roth Conversions Work

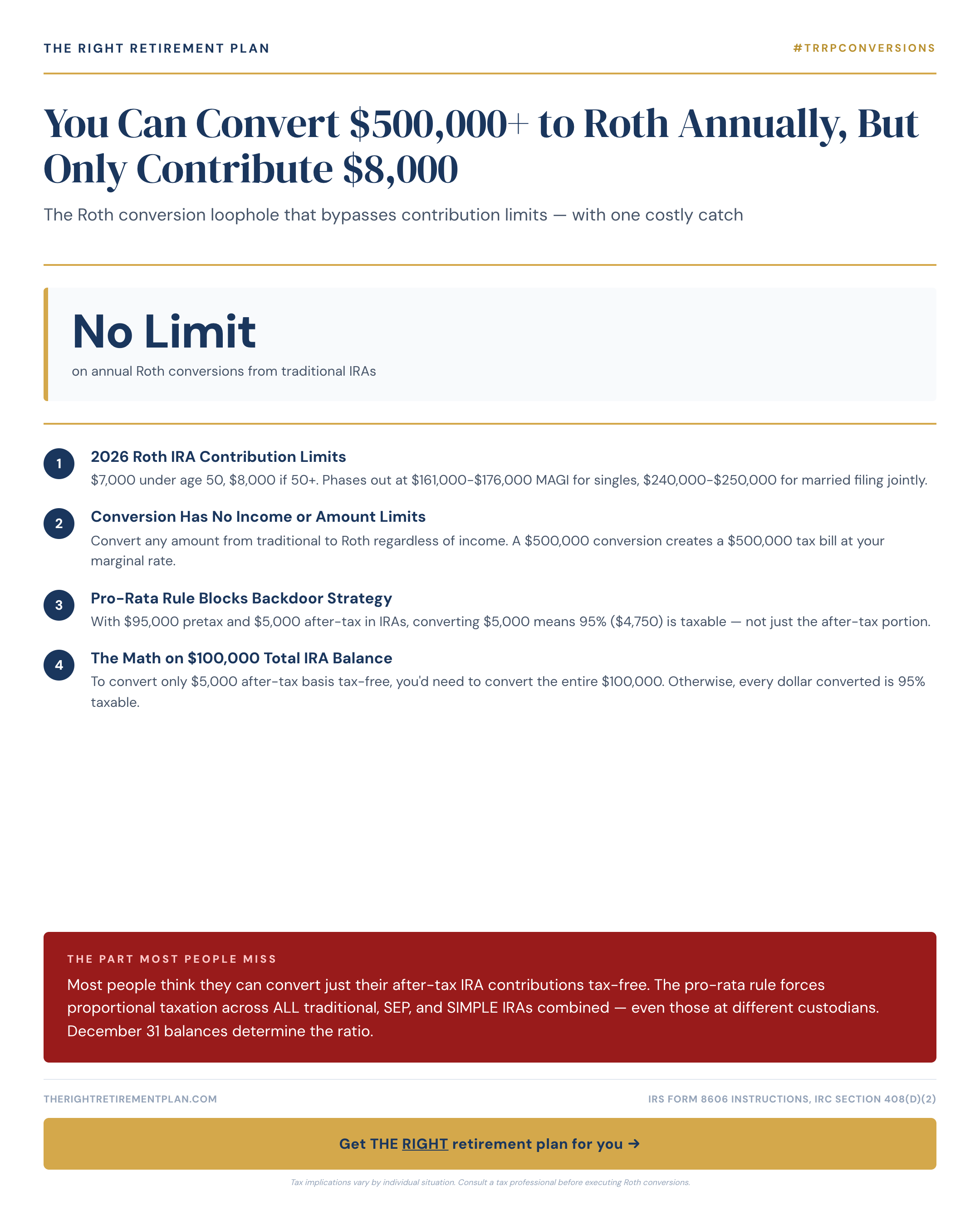

Unlike contributions, Roth conversions have no income or dollar limits. You can convert any amount from traditional IRAs, 401(k)s, or other pre-tax accounts to Roth status. The catch? You'll owe ordinary income tax on the converted amount in the year of conversion.

This strategy appeals to:

- High earners excluded from direct Roth contributions

- Retirees managing tax brackets across multiple years

- Investors seeking tax-free growth for heirs

- Those anticipating higher future tax rates

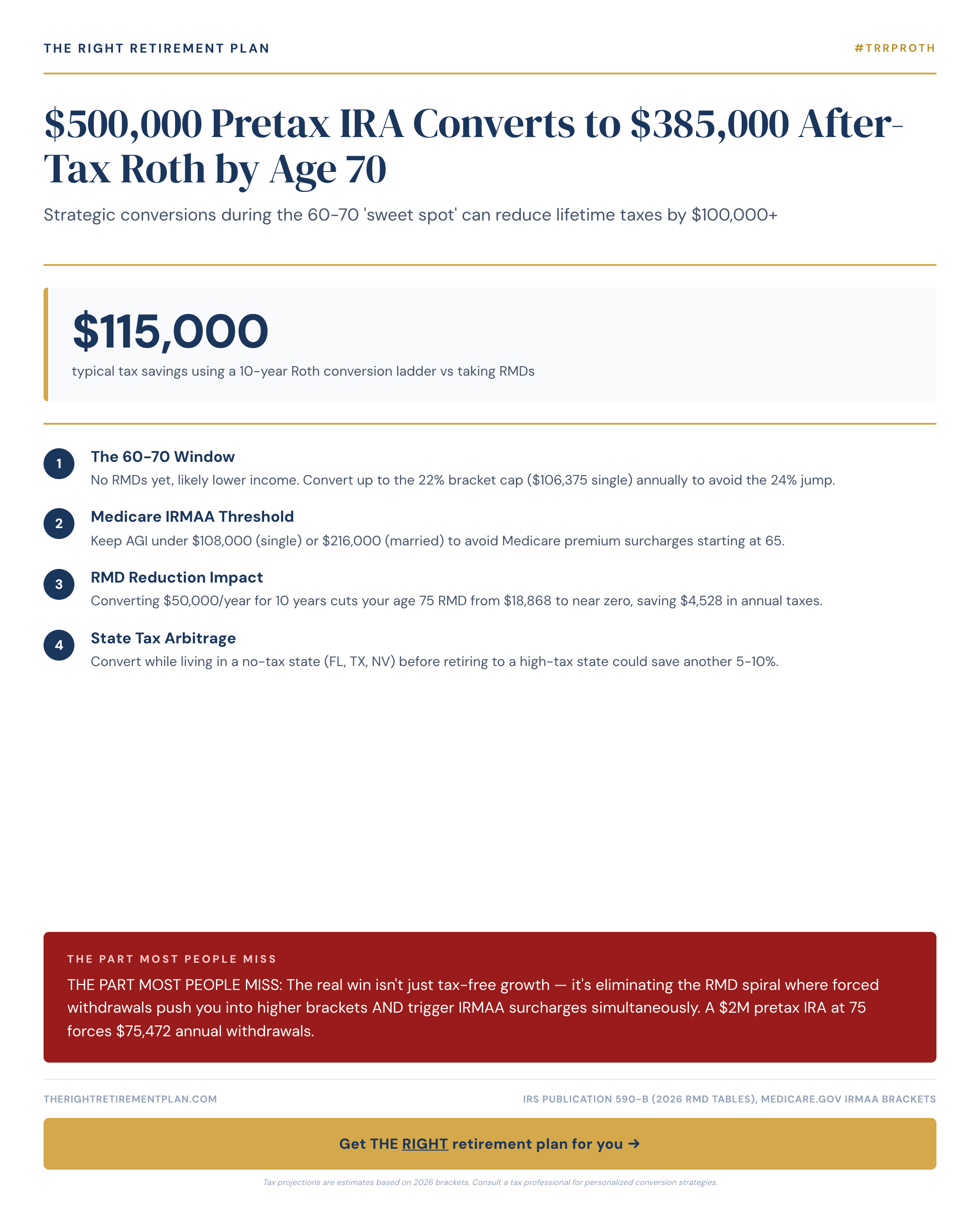

Many Maryland retirees use conversions to fill lower tax brackets during early retirement years before Required Minimum Distributions begin at age 73.

The Pro-Rata Rule Trap

Here's where most people stumble. The IRS pro-rata rule treats all your traditional, SEP, and SIMPLE IRAs as one giant account—regardless of which custodian holds them.

When you convert any amount, the IRS calculates what percentage represents after-tax contributions versus pre-tax money across your entire IRA universe. Your December 31 balances determine this ratio.

For example: You have $90,000 in pre-tax IRAs and $10,000 in after-tax contributions. Any conversion will be 90% taxable, 10% tax-free—even if you try converting only from the after-tax portion.

This rule applies to:

- All traditional IRAs combined

- SEP and SIMPLE IRAs

- Accounts at different brokerage firms

- Your spouse's accounts (calculated separately)

Strategic Timing Matters

Smart retirement planning involves timing conversions when tax brackets are favorable. Consider converting during:

- Years with lower income (early retirement)

- Market downturns (convert more shares for less tax)

- Before Medicare kicks in (avoiding income-related premium adjustments)

The 2026 tax brackets make this particularly relevant as current rates expire after 2025.

Getting these details right requires careful planning around your specific situation, timeline, and goals. If you want personalized guidance on how Roth conversion strategies might fit your retirement plan, consider taking our Retire Ready Score for tailored insights.