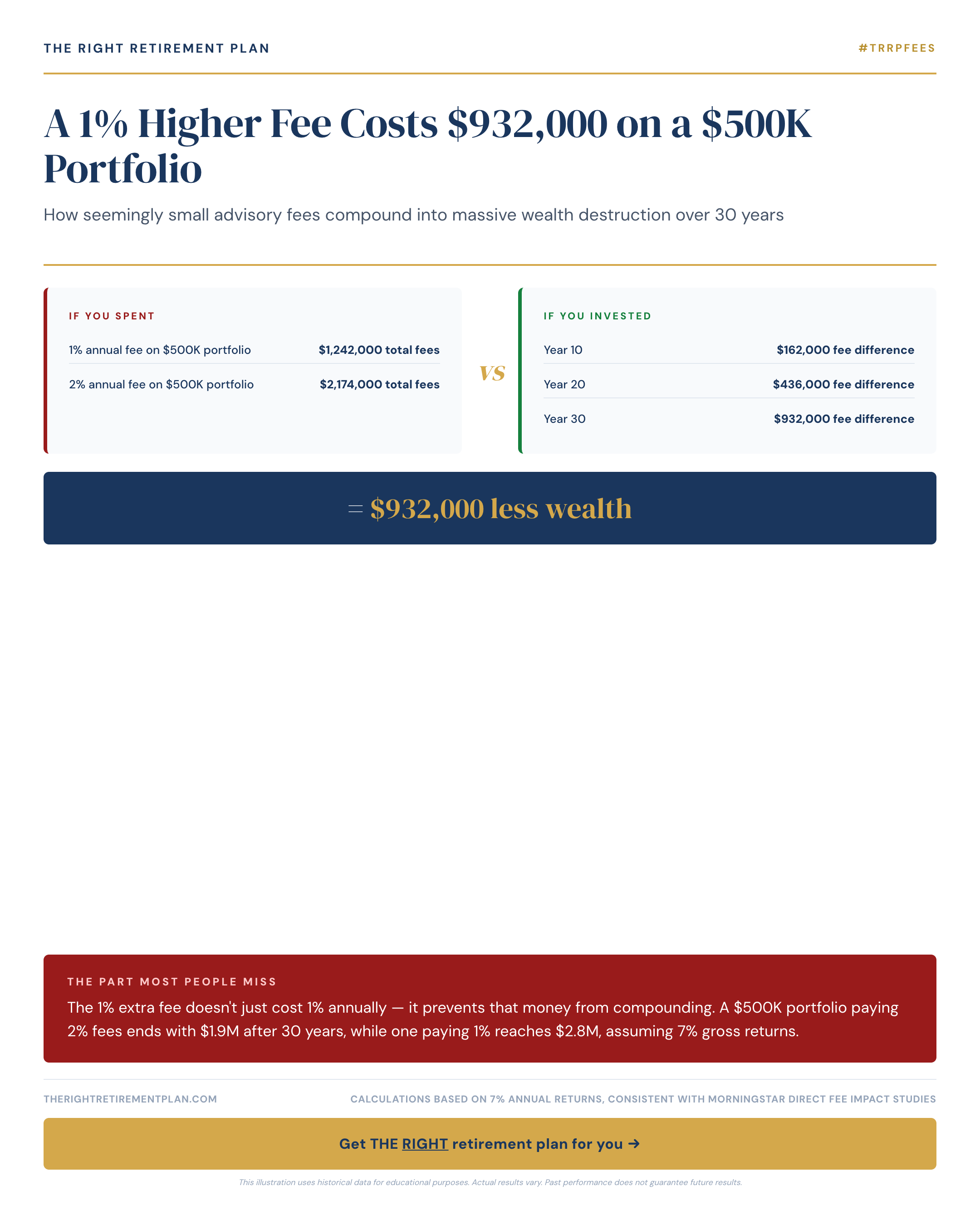

Most pre-retirees focus on picking the right stocks or timing the market, but advisory fees represent one of the biggest threats to long-term wealth accumulation. A seemingly small 1% difference in annual fees can devastate your retirement nest egg through the power of reverse compounding.

The Million-Dollar Math Behind Advisory Fees

Consider a $500,000 portfolio with 7% gross annual returns over 30 years. Here's where investment fees create massive divergence:

- 1% annual fee: Portfolio grows to $2.8 million

- 2% annual fee: Portfolio grows to only $1.9 million

- Difference: $932,000 in lost wealth

The higher fee doesn't just cost you 1% each year—it prevents that money from compounding and growing. Over three decades, this creates an almost $1 million wealth gap that many Maryland retirees never recover from.

This math applies whether you're paying mutual fund expense ratios, advisory management fees, or wrap account charges. The fee structure matters less than the total annual cost.

Why Small Percentages Create Big Problems

Fee compounding works against you in two devastating ways:

- Direct cost: You pay more each year in absolute dollars as your account grows

- Opportunity cost: Money paid in fees can't compound and grow over time

A 2% fee on a $500,000 account costs $10,000 in year one. But on a $1.5 million account 20 years later, that same 2% costs $30,000 annually. Meanwhile, all those fee payments missed decades of potential growth.

Many investors underestimate this impact because they think in annual terms rather than cumulative wealth destruction over retirement timeframes.

Finding Fee-Conscious Solutions

Lower-cost alternatives include:

- Index funds with expense ratios under 0.20%

- Fee-only financial advisors charging flat rates

- Target-date funds from reputable providers

- Self-directed investing with educational support

The key is understanding exactly what you're paying across all investment accounts and whether those fees deliver proportional value.

Take the next step: If you want personalized guidance on optimizing your retirement plan while minimizing unnecessary costs, consider taking our free Retire Ready Score assessment.