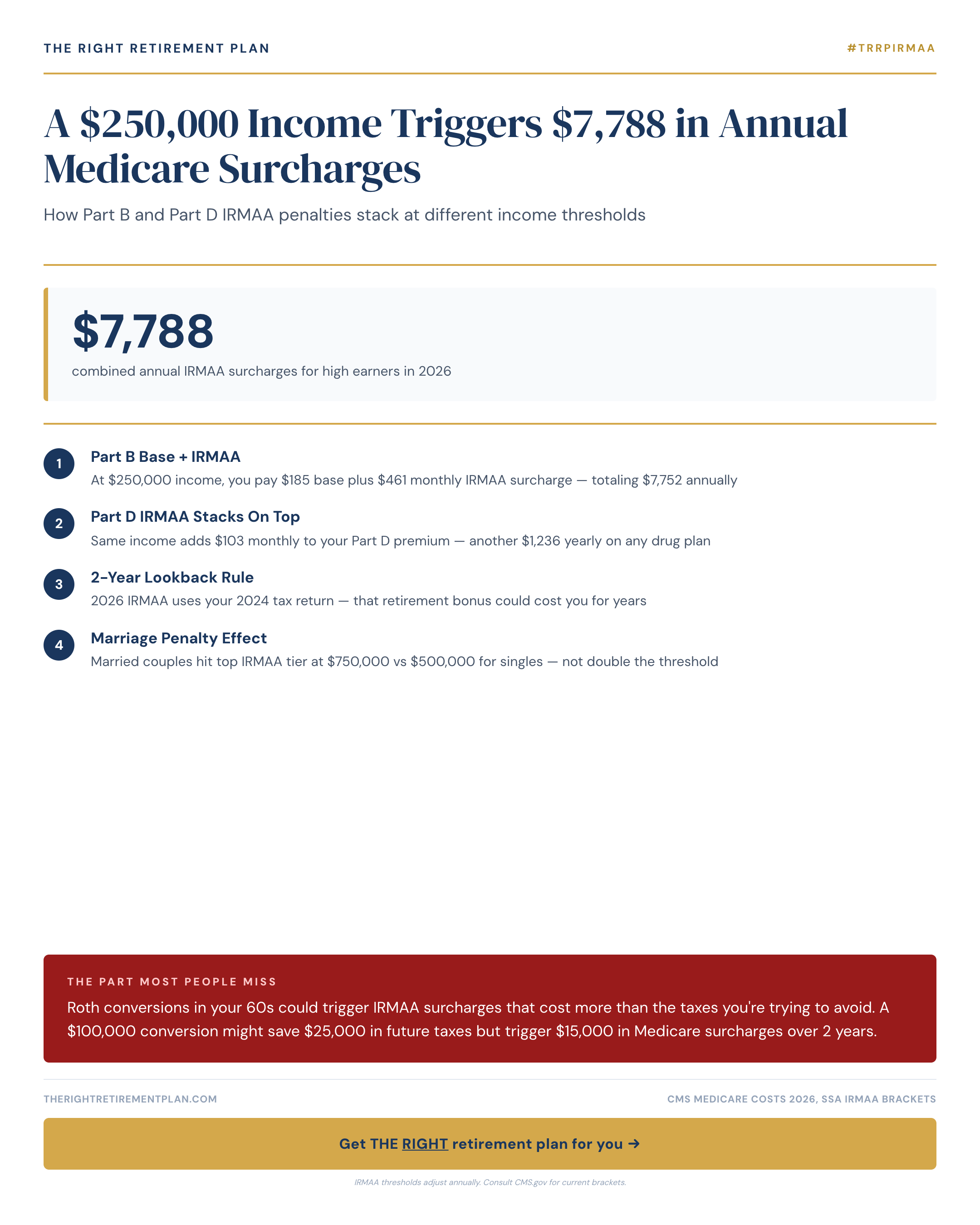

Medicare's Income-Related Monthly Adjustment Amount (IRMAA) can significantly impact your retirement budget if you're not prepared. For 2026, retirees with modified adjusted gross income (MAGI) of $250,000 or more face substantial Medicare surcharges that many don't see coming.

Understanding IRMAA Penalties

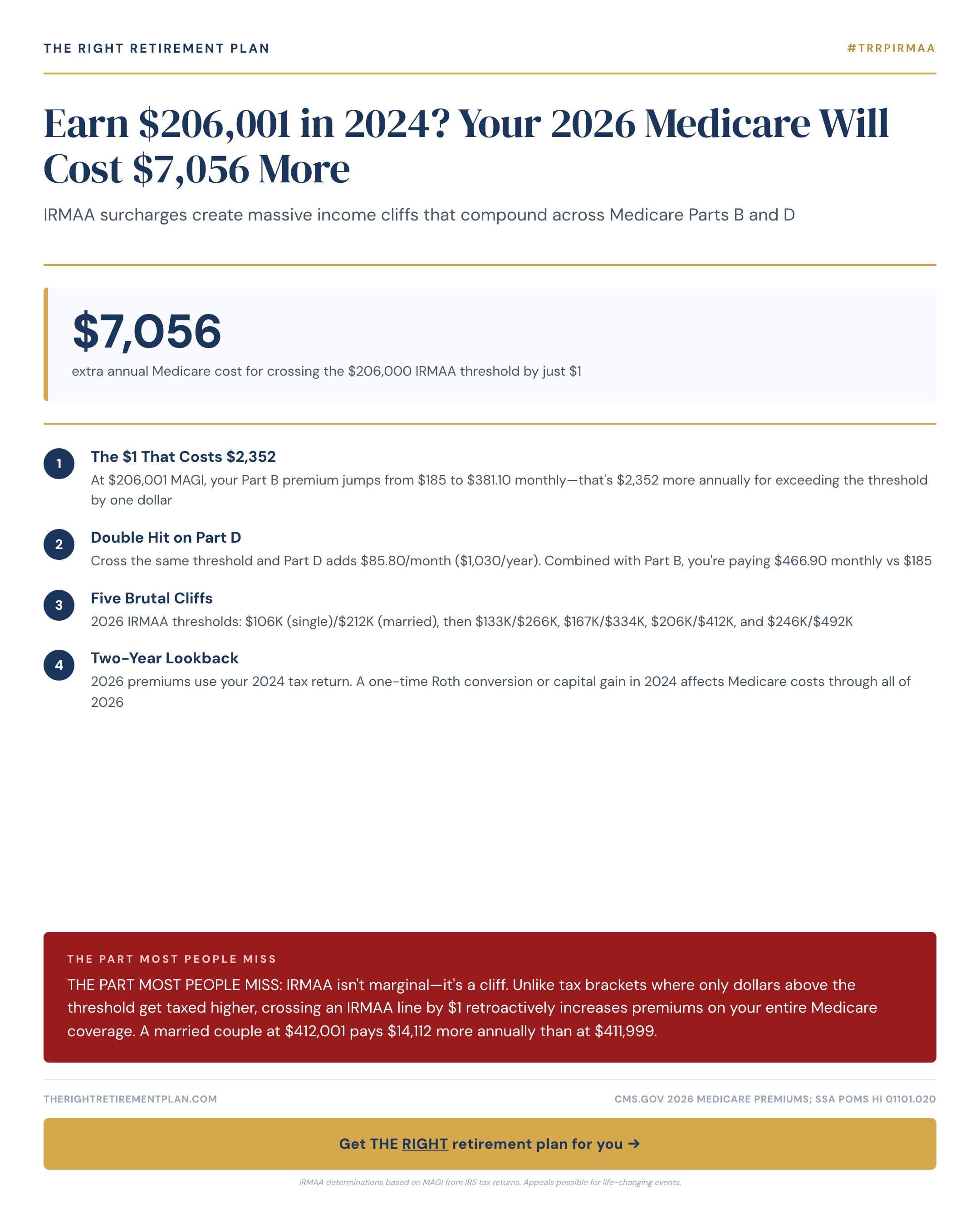

IRMAA affects both Medicare Part B (medical insurance) and Part D (prescription drug coverage). The surcharges are based on your income from two years prior, meaning your 2026 Medicare costs depend on your 2024 tax return.

For single filers earning $250,000 in 2024, the annual Medicare surcharges in 2026 will total $7,788:

- Part B surcharge: $5,893 annually ($491 monthly)

- Part D surcharge: $1,895 annually ($158 monthly)

- Combined impact: Nearly $8,000 in additional healthcare costs

These Medicare IRMAA penalties stack on top of standard Part B and Part D premiums, creating a substantial financial burden for higher-income retirees. The surcharges increase further at higher income thresholds, reaching over $12,000 annually for those earning $500,000 or more.

Strategic Planning Considerations

Income management becomes critical when you're approaching these thresholds. Maryland retirees and others in higher-cost regions often find themselves unexpectedly subject to IRMAA due to pension distributions, investment gains, or Roth conversion strategies.

Consider these planning opportunities:

- Roth conversions in lower-income years before age 65

- Timing of asset sales to avoid income spikes

- Charitable giving strategies that reduce MAGI

- Municipal bond investments for tax-free income

Roth conversions, while beneficial long-term, can trigger immediate IRMAA consequences. A $100,000 conversion might save $25,000 in future taxes but could trigger $15,000 in Medicare surcharges over two years, reducing your net benefit significantly.

Understanding Medicare IRMAA thresholds and planning around them can save thousands annually in healthcare costs. The key is proactive income management before you reach Medicare eligibility, not reactive adjustments after enrollment.

If you want personalized guidance on how Medicare surcharges might affect your retirement plan, consider taking our free Retire Ready Score assessment.