Converting a traditional IRA to a Roth IRA sounds appealing — tax-free growth and no required distributions. But for high earners expecting modest retirement income, this strategy can backfire spectacularly.

The Math That Matters

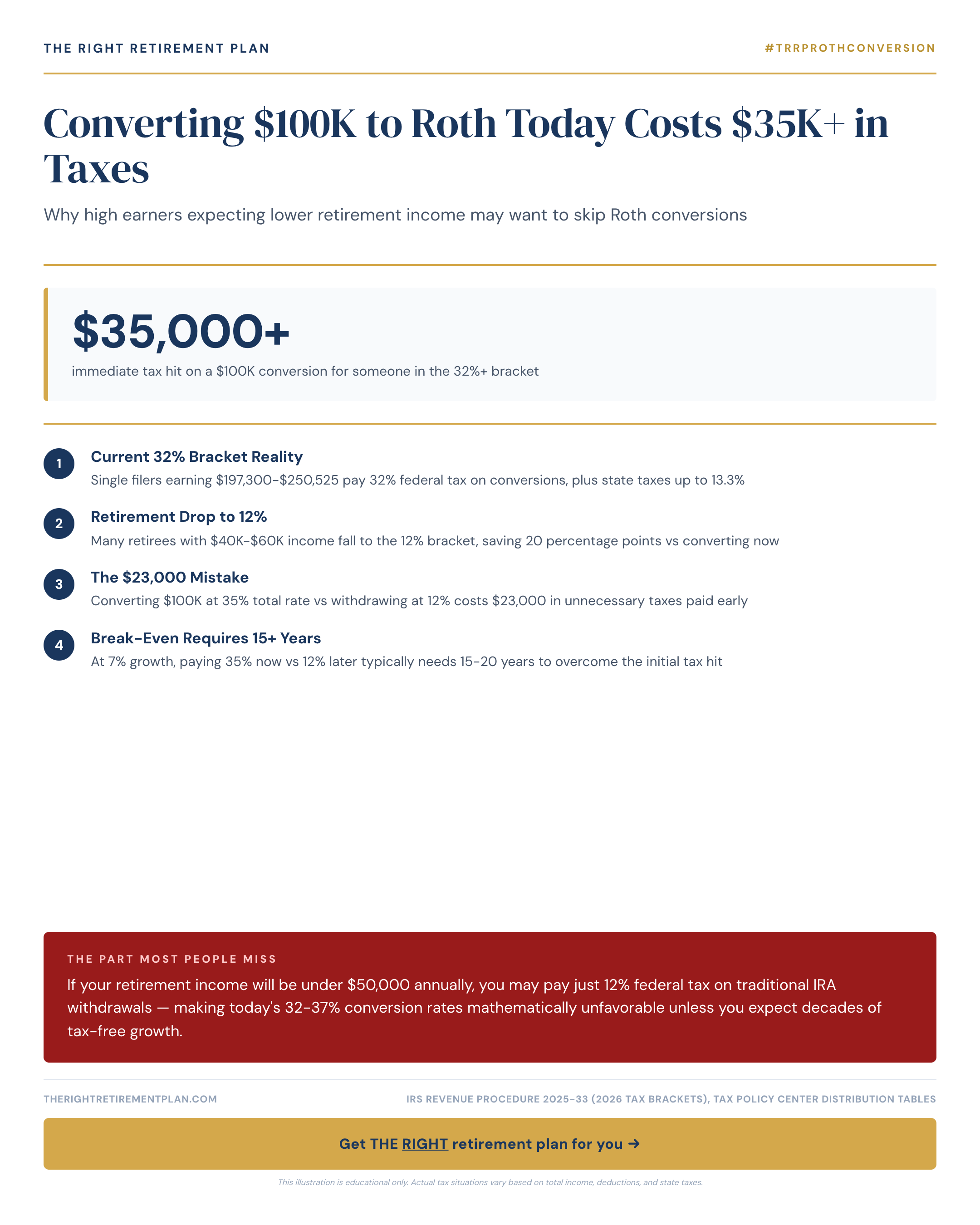

Here's the reality: converting $100,000 from a traditional IRA to a Roth in 2026 could cost you $35,000 or more in federal taxes if you're in the 32% or 37% tax bracket. That's a substantial upfront cost for a benefit you might not need.

Consider this scenario: you're earning $200,000 annually but expect your retirement income to be around $50,000 per year. At that income level, you'll likely pay just 12% federal tax on traditional IRA withdrawals — assuming 2026 tax brackets remain similar to today's structure.

The numbers tell the story:

- Current conversion cost: 32-37% tax rate

- Future withdrawal cost: 12% tax rate

- Net difference: 20-25% penalty for converting early

When Lower Income Works in Your Favor

Many Maryland retirees discover their retirement income sits comfortably in lower tax brackets. Social Security benefits are often partially tax-free, and without employment income, total taxable income drops significantly.

If your retirement income stays under the 12% bracket threshold (approximately $23,200 for singles, $46,400 for married couples in 2026), you're essentially paying today's high rates to avoid tomorrow's low rates.

This strategy makes even less sense when you consider:

- Medicare premiums increase with higher income

- Social Security benefits may become more taxable

- State tax implications vary significantly

Smart Alternatives to Consider

Instead of wholesale conversions, consider these approaches:

- Partial conversions during low-income years

- Converting only enough to stay in your current bracket

- Waiting until early retirement when income gaps appear

- Using conversions strategically before Medicare enrollment

The key is matching the timing to your specific income trajectory, not following generic advice.

If you want personalized guidance on whether Roth conversions make sense for your situation, consider taking our Retire Ready Score for insights tailored to your retirement plan.