How IRMAA Makes Medicare More Expensive

Medicare Part B doesn't cost the same for everyone. If your modified adjusted gross income exceeds certain thresholds, you'll pay income-related monthly adjustment amounts (IRMAA) on top of the standard premium.

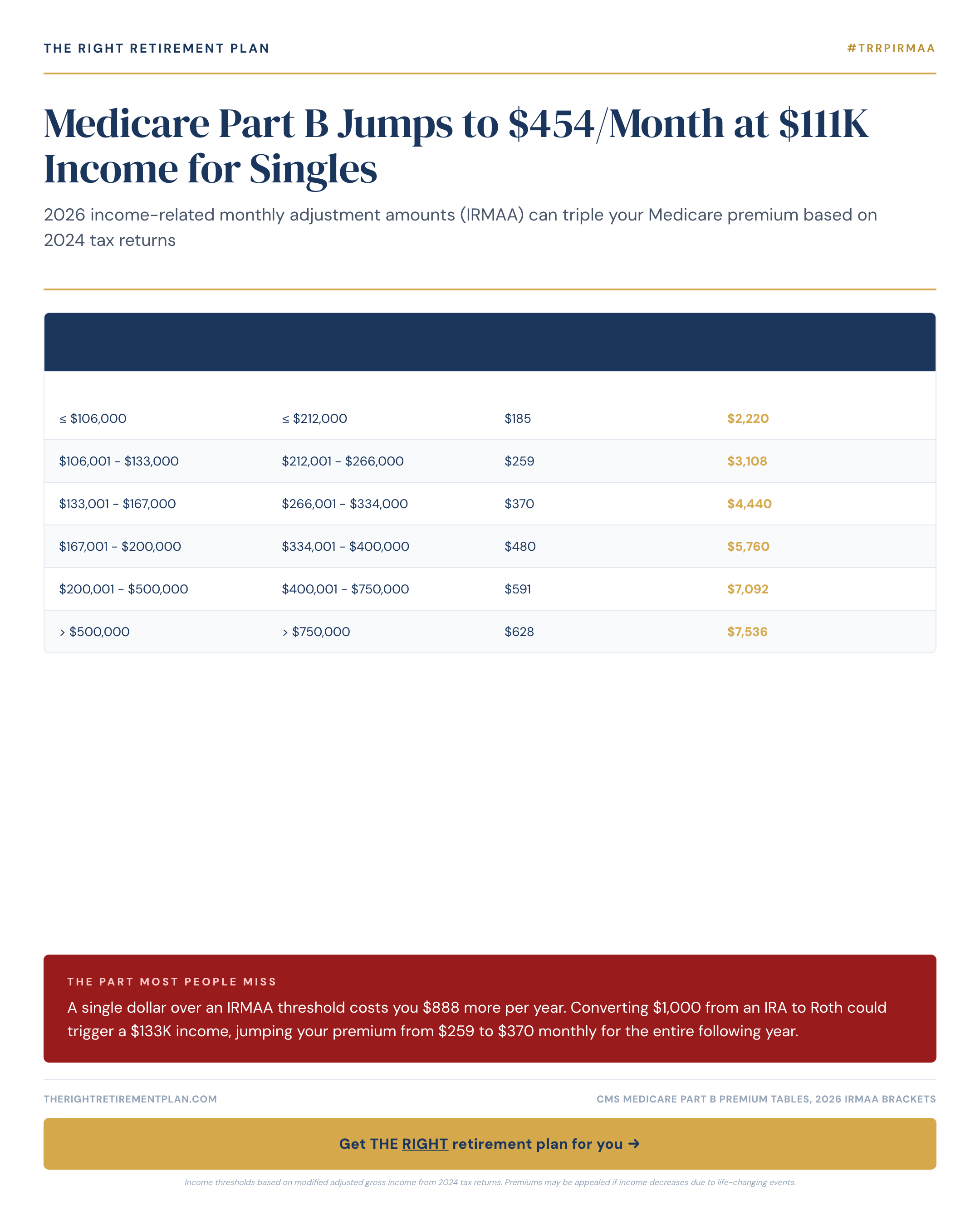

For 2026, singles earning between $111,000-$139,000 in 2024 will pay $454 monthly for Medicare Part B. That's nearly double the standard premium of $259. The adjustment applies to both Medicare Part B and Part D prescription coverage.

Here's how the 2026 IRMAA brackets break down for singles:

- Under $111,000: $259/month (standard premium)

- $111,000-$139,000: $454/month

- $139,000-$174,000: $649/month

- $174,000-$218,000: $844/month

- Over $218,000: $1,039/month

For married couples filing jointly, these thresholds double. The premium jumps occur at $222,000, $278,000, $348,000, and $436,000.

The Costly Timing Trap

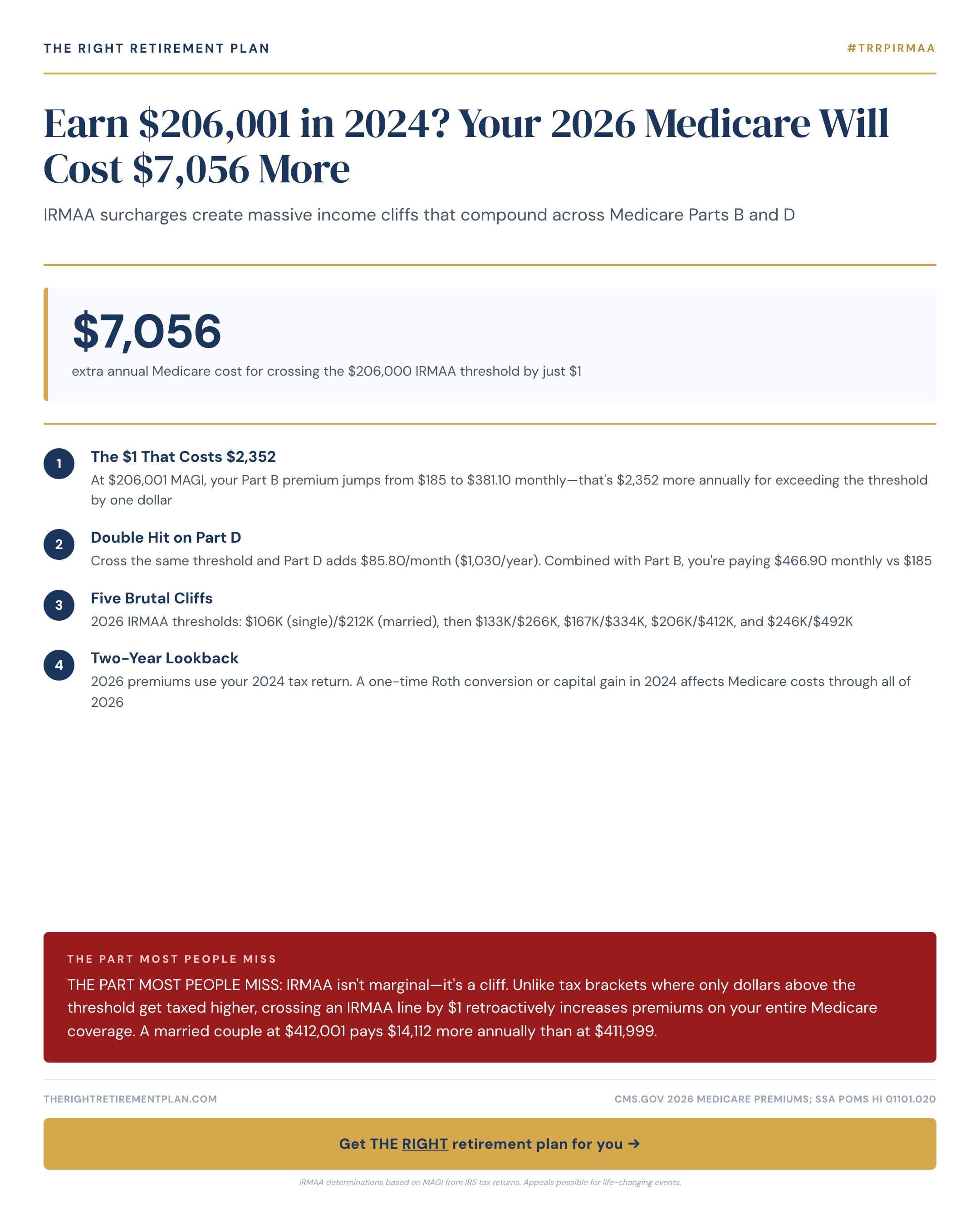

IRMAA calculations use your tax return from two years prior. Your 2026 Medicare premiums depend on your 2024 income—income you may have already reported.

This creates planning challenges many Maryland retirees don't anticipate. A single dollar over an IRMAA threshold costs $2,340 annually in extra premiums. Converting $1,000 from a traditional IRA to Roth could push your income from $110,999 to $111,999, triggering the higher bracket for the entire following year.

The timing gets trickier because Social Security also counts toward IRMAA calculations. Many retirees in the Annapolis area discover their combined pension, Social Security, and investment income pushes them into higher premium brackets unexpectedly.

Large retirement account withdrawals, Roth conversions, or one-time capital gains can trigger IRMAA surcharges. Even selling your home could affect Medicare premiums if the gain pushes you over income thresholds.

Planning Around IRMAA

Smart retirement income planning considers both tax efficiency and Medicare premium impacts. Spreading large withdrawals across multiple years, timing Roth conversions strategically, and coordinating Social Security claiming decisions all help manage IRMAA exposure.

If extraordinary circumstances caused a temporary income spike, you can appeal IRMAA adjustments. Qualifying events include retirement, marriage, divorce, or loss of pension income.

If you want personalized guidance on how IRMAA planning fits your retirement strategy, consider taking our Retire Ready Score assessment.