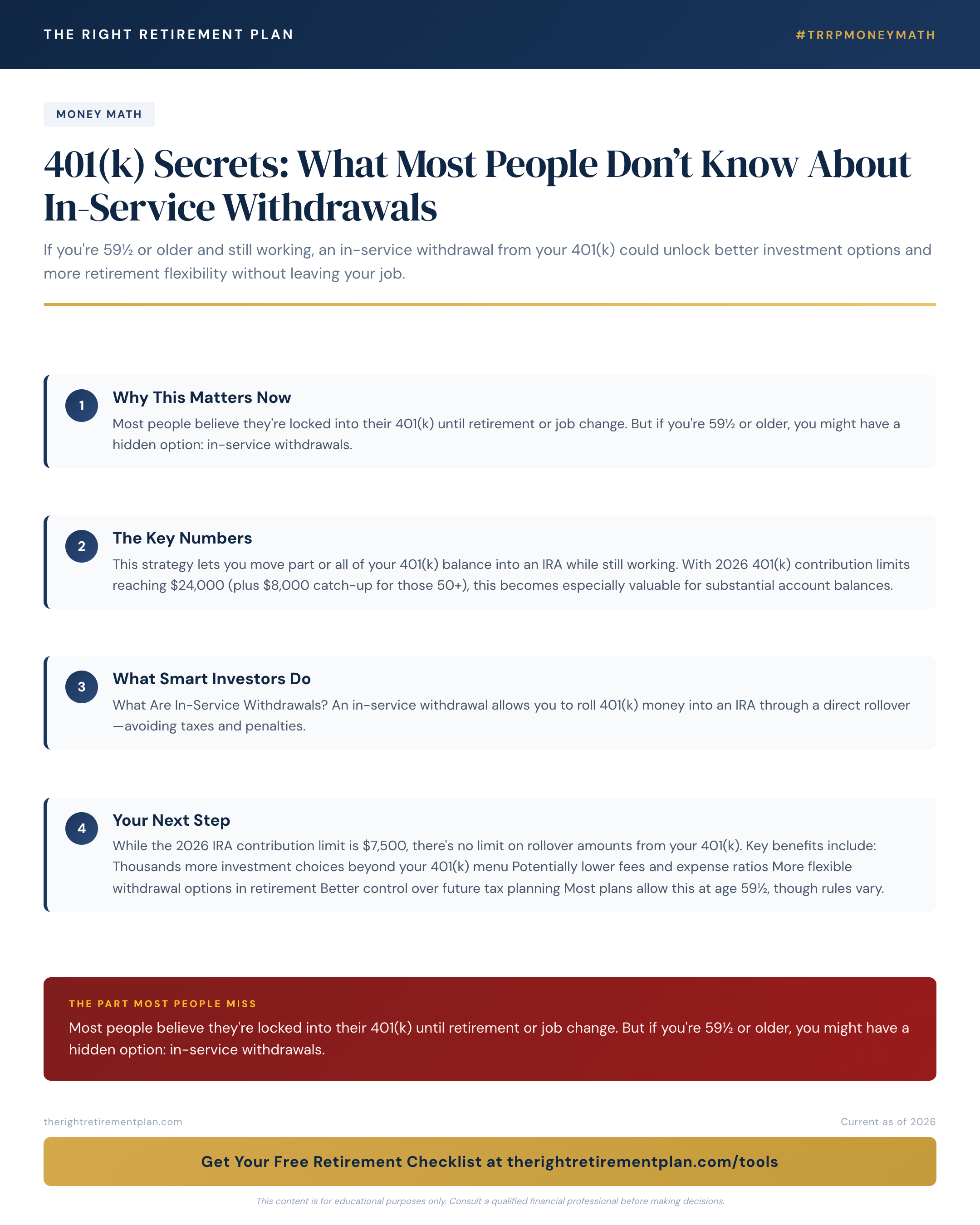

401(k) Secrets: What Most People Don’t Know About In-Service Withdrawals

If you're 59½ or older and still working, an in-service withdrawal from your 401(k) could unlock better investment options and more retirement flexibility without leaving your job. Here's what Maryland pre-retirees need to know about this powerful but overlooked strategy.