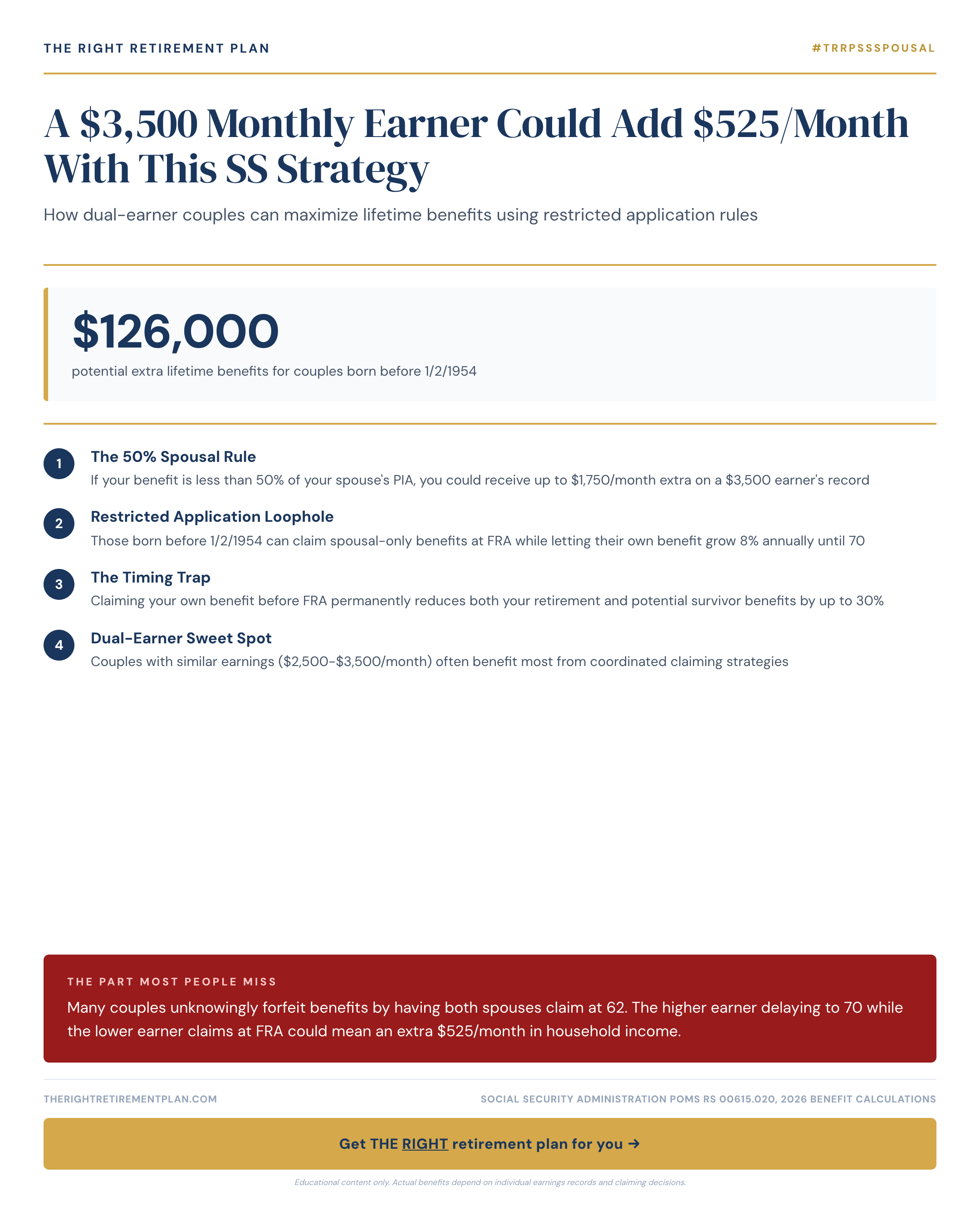

How Strategic Timing Creates Extra Income

Many dual-earner couples make a costly mistake: both spouses claim Social Security at 62, thinking they're maximizing their benefits. In reality, this strategy often leaves substantial money on the table.

Here's how the math works for a couple where one spouse earns around $3,500 monthly. If the higher-earning spouse delays claiming until age 70, their monthly benefit grows by approximately 8% each year past full retirement age. Meanwhile, the lower-earning spouse can claim at their full retirement age without penalty.

This coordinated approach can generate an additional $525 per month in household Social Security income compared to both spouses claiming early. Over a 20-year retirement, that's an extra $126,000 in lifetime benefits.

The Optimal Social Security Strategy Breakdown

The most effective Social Security maximization strategy for dual-earner couples involves careful timing:

- Higher earner: Delay benefits until age 70 to earn delayed retirement credits

- Lower earner: Claim at full retirement age (66-67 depending on birth year)

- Spousal benefits: The lower earner may qualify for spousal benefits worth up to 50% of the higher earner's benefit

For 2026, the maximum Social Security benefit at full retirement age is $3,822 monthly. By delaying to age 70, this could grow to approximately $4,743 monthly—a significant boost that compounds over decades.

Maryland retirees and couples throughout the Mid-Atlantic region often overlook these nuances, focusing instead on when they can first claim rather than when they should claim for maximum benefit.

Avoiding the Early Claiming Trap

Claiming Social Security at 62 reduces your benefit permanently. For someone with a full retirement age of 67, claiming at 62 means accepting just 70% of their full benefit for life. There's no "do-over" once you start receiving payments.

The reduction affects not just the primary earner but also impacts survivor benefits. When one spouse passes away, the surviving spouse receives the higher of the two benefits—making the higher earner's delayed claiming strategy even more valuable.

Smart Social Security timing can add hundreds of dollars monthly to your retirement income. If you want personalized guidance on how this strategy might work for your situation, consider taking our Retire Ready Score to see where you stand.