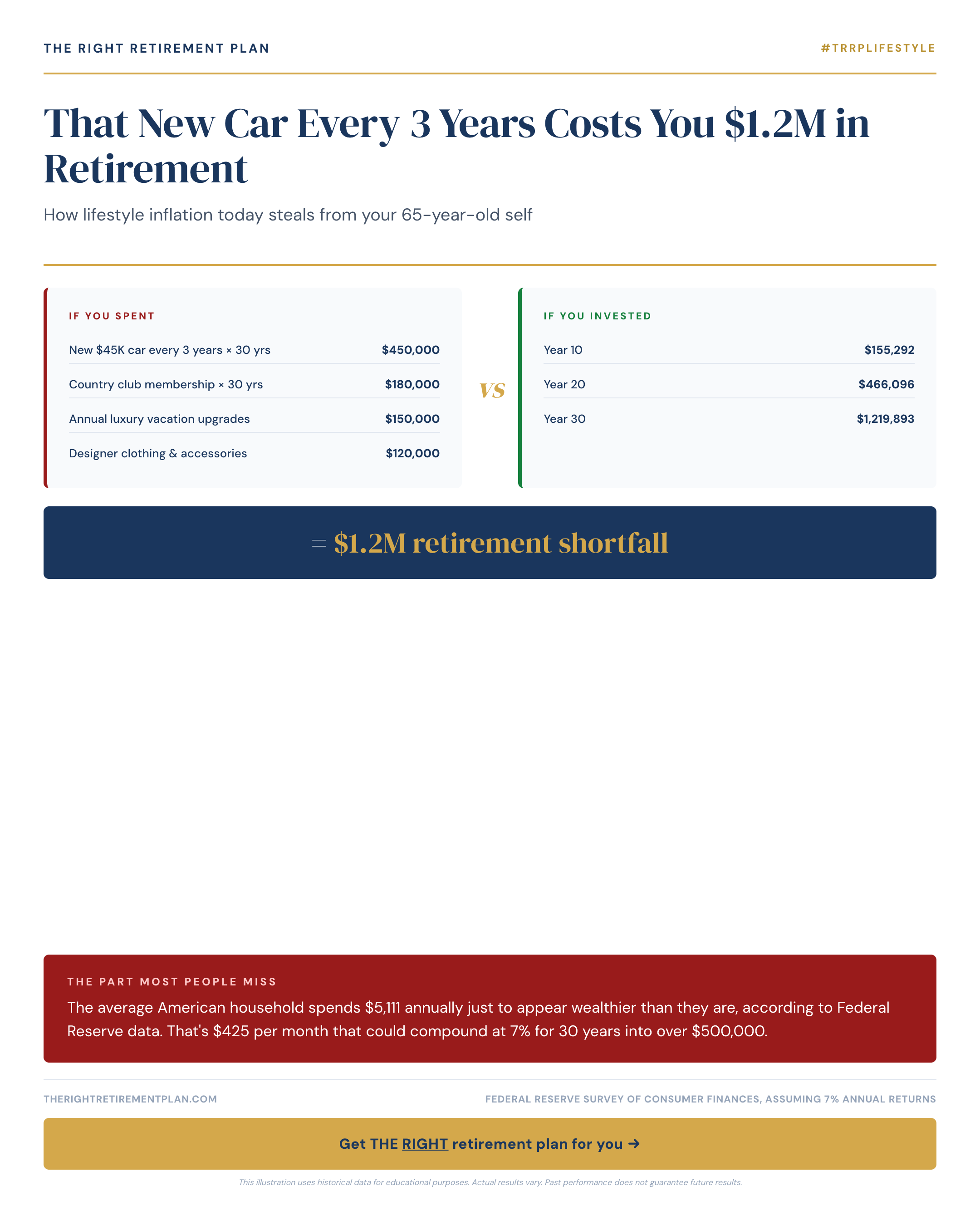

The Hidden Cost of Lifestyle Inflation

Every time you upgrade your lifestyle, you're making a choice between today's comfort and tomorrow's security. The numbers are sobering: that shiny new car every three years doesn't just cost you monthly payments—it can steal over $1.2 million from your retirement.

Here's the math that most people never calculate. A typical car payment of $600 monthly, repeated every three years for 30 years, represents $216,000 in total payments. But the real cost? The opportunity cost of not investing that money.

If those same dollars went into retirement accounts earning 7% annually, you'd have approximately $1.2 million by age 65. That's the difference between financial stress and financial freedom in retirement.

The $425 Monthly Trap

The Federal Reserve reports that average American households spend $5,111 annually—roughly $425 monthly—just to appear wealthier than they are. This lifestyle inflation affects everything from dining out more frequently to upgrading homes, gadgets, and yes, cars.

Maryland retirees who tracked their spending often discover they were unconsciously competing in this expensive game. The pressure to "keep up" costs them compound interest—the most powerful force in building retirement wealth.

Consider these common lifestyle inflation triggers:

- Trading up homes when income increases

- Buying premium brands instead of quality basics

- Adding subscription services without canceling others

- Financing purchases instead of saving first

Each upgrade feels reasonable in isolation, but collectively they redirect money from your 2026 contribution limits of $23,000 for 401(k)s (or $30,500 if you're 50+) toward maintaining appearances.

Breaking the Cycle

Start by calculating the true cost of major purchases over 30 years. That $40,000 kitchen renovation? It's really $300,000 in lost retirement wealth. The extra $200 monthly for premium cable and streaming? Nearly $200,000.

The solution isn't living like a monk—it's being intentional. Before any significant lifestyle upgrade, ask: "Is this worth X dollars from my retirement?" Often, the answer shifts your perspective entirely.

If you want personalized guidance on balancing today's lifestyle with tomorrow's security, consider taking our Retire Ready Score to see how your current plan stacks up.