Why Your 60s Are a Tax Goldmine

The decade before age 70 represents the most overlooked opportunity in retirement planning. Most retirees sit in artificially low tax brackets during these years—they've stopped earning salaries but haven't yet started Social Security or Required Minimum Distributions.

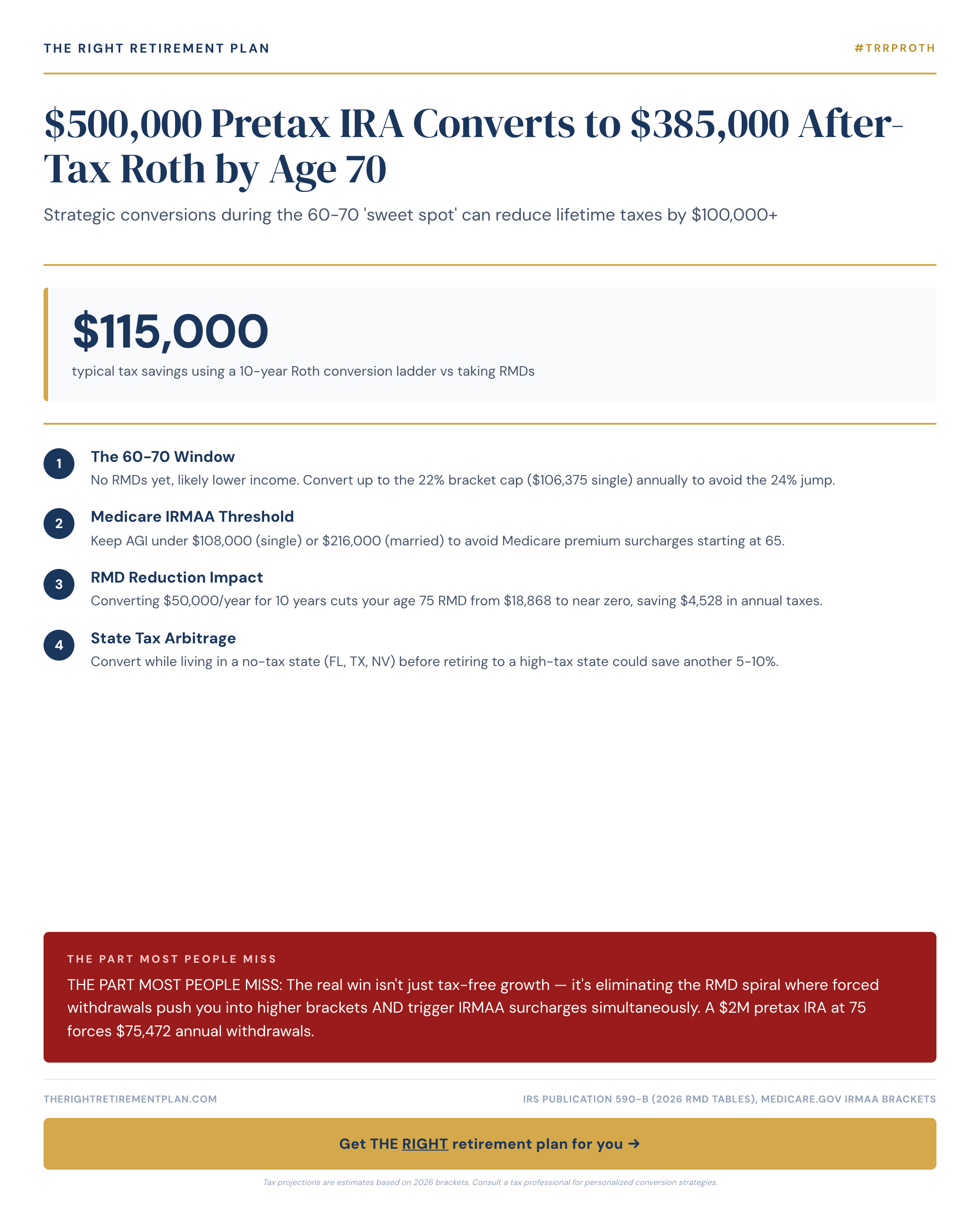

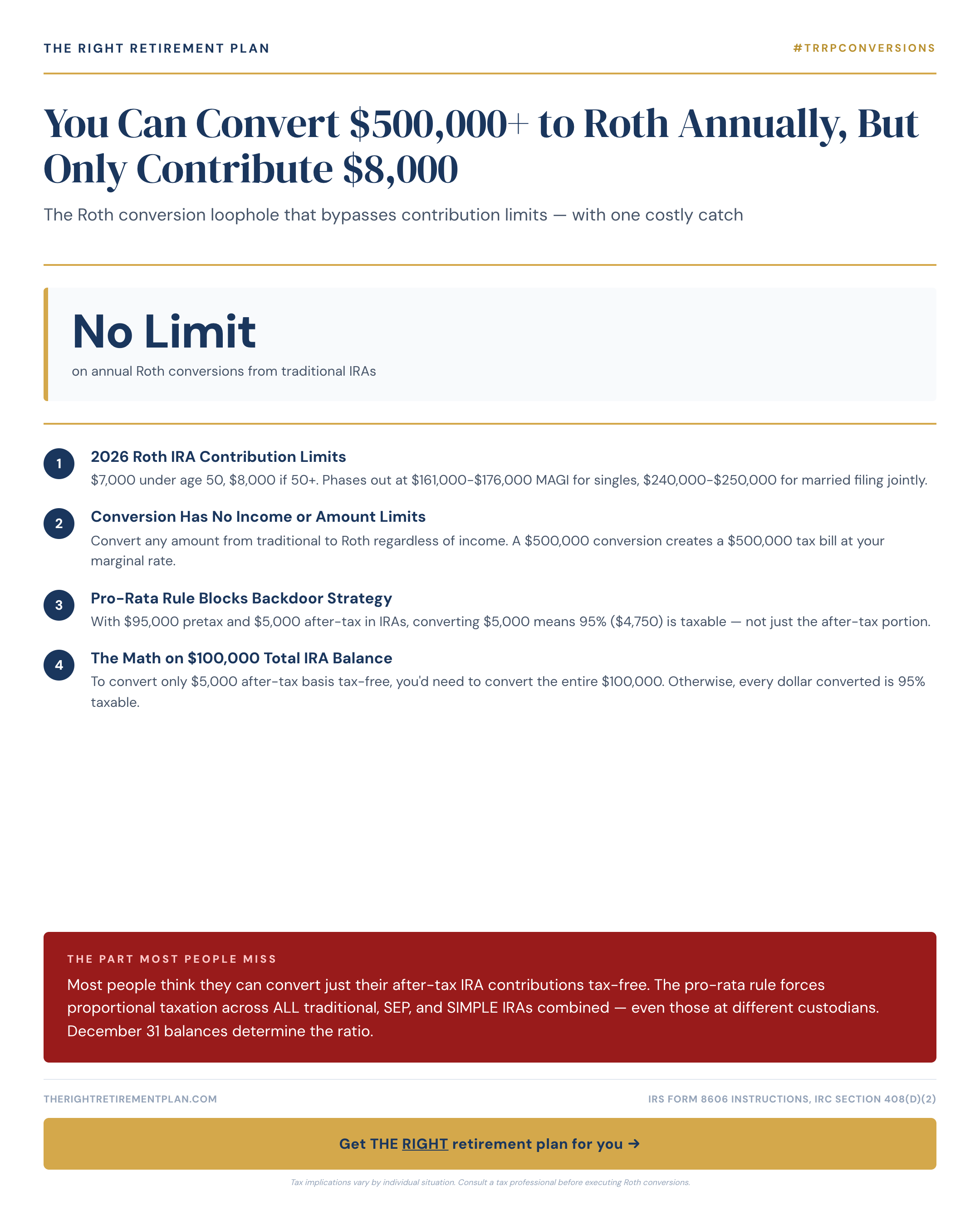

Here's compelling proof: A $500,000 pretax IRA can become approximately $385,000 in after-tax Roth value through strategic conversions. You voluntarily pay roughly $115,000 in taxes over several years to potentially save far more later.

The math works because of timing. Your taxable income might drop from $150,000 to $30,000 overnight when you retire. That creates conversion opportunities that disappear permanently once RMDs begin at age 73.

The Roth Conversion Math for 2026

Strategic Roth conversions work best when you understand the 2026 federal tax brackets. For married couples filing jointly:

- 12% bracket: Income up to approximately $94,000

- 22% bracket: Income from $94,000 to roughly $201,000

- 24% bracket: Income from $201,000 to approximately $383,000

Consider a retired Maryland couple with $40,000 in pension income and $24,000 in taxable Social Security benefits. Their baseline income of $64,000 leaves substantial room in the 12% and 22% brackets.

A practical conversion schedule might include:

- Ages 62-65: Convert $50,000 annually, paying about $11,000 in federal taxes each year

- Ages 66-69: Continue converting $50,000-60,000 annually

- Total converted: $500,000 over eight years

- Total taxes paid: Approximately $115,000

Research from Vanguard shows systematic Roth conversions during low-income years can improve after-tax retirement income by 10-15% over a 30-year retirement.

The Hidden Cost of Waiting

Required Minimum Distributions create a devastating spiral that most people don't see coming. At age 73, the IRS forces withdrawals whether you need the money or not.

A $2 million pretax IRA at age 75 requires approximately $75,472 in annual RMDs. This forced income triggers multiple consequences:

- Tax bracket creep: RMDs push many retirees from the 22% bracket into 24% or higher

- IRMAA surcharges: Medicare premiums jump when income exceeds $206,000 for couples, adding $1,678+ annually per spouse

- Social Security taxation: Higher income means up to 85% of benefits become taxable

- Net Investment Income Tax: An additional 3.8% tax on investment income above certain thresholds

Retirees across the Mid-Atlantic region often underestimate this tax burden by 15-25%, according to Employee Benefit Research Institute data.

The conversion strategy breaks this cycle before it starts, giving you control over your tax bracket in retirement instead of letting the IRS dictate your income through forced withdrawals.

Converting during your 60s typically costs 12-22% in taxes on money you'll eventually owe 24-32% on anyway—plus IRMAA surcharges and higher Social Security taxation. The math strongly favors acting during the low-bracket window.

If you'd like personalized guidance on how Roth conversions might fit your retirement timeline, consider taking our free Retire Ready Score to identify opportunities specific to your situation.