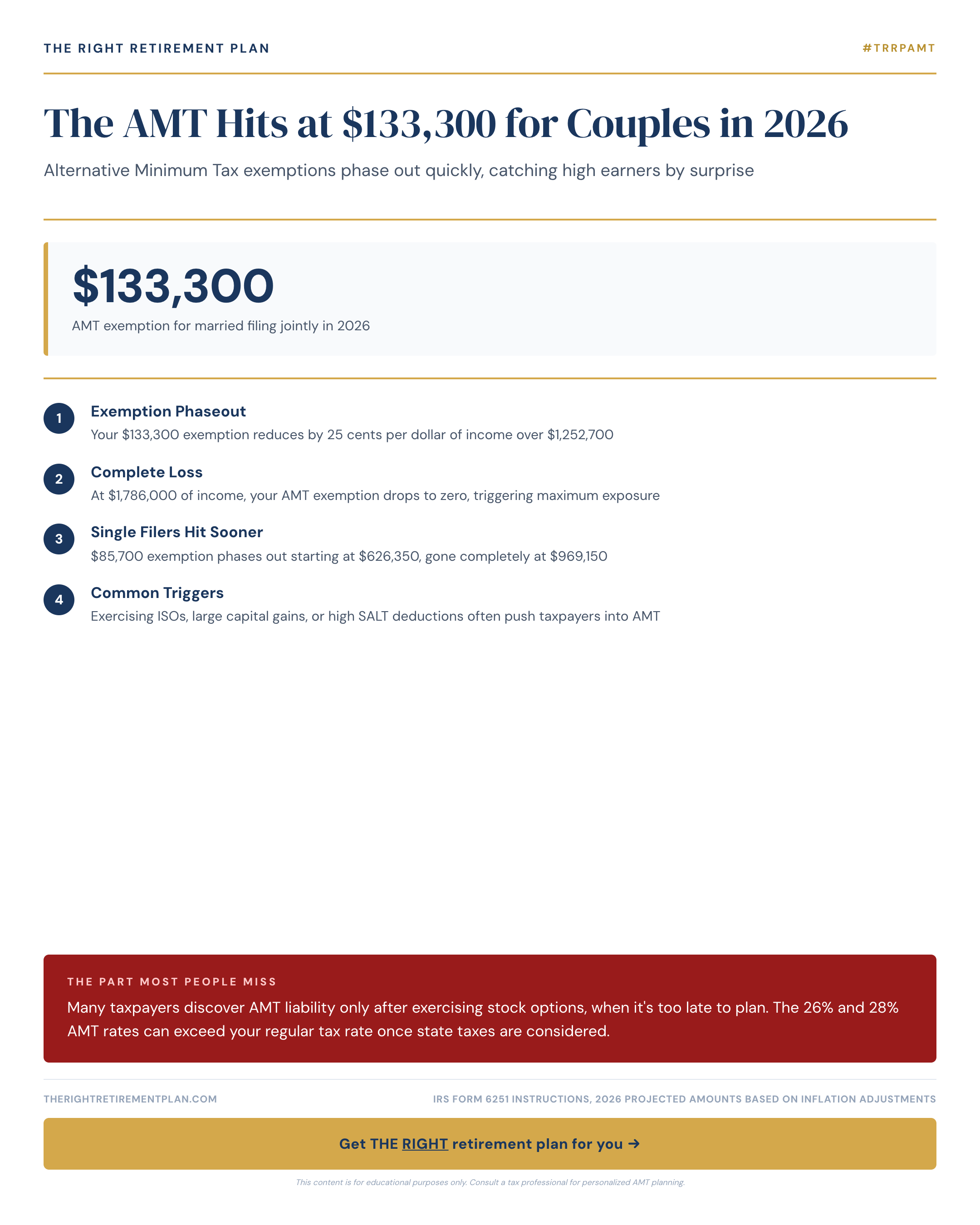

The Alternative Minimum Tax (AMT) catches many pre-retirees off guard, especially when retirement planning involves stock options or significant deductions. For 2026, married couples filing jointly face AMT exemption phase-out starting at $133,300 in adjusted gross income—a threshold that's easier to hit than many realize.

How the AMT Exemption Phase-Out Works

The AMT operates as a parallel tax system designed to ensure high earners pay a minimum amount of tax. In 2026, the AMT exemption for married couples is $133,300, but this exemption phases out completely once income reaches $888,350.

Here's what triggers AMT liability for many pre-retirees:

- Exercising incentive stock options (ISOs)

- Large state and local tax deductions

- Significant miscellaneous itemized deductions

- Tax-exempt interest from private activity bonds

The AMT rates of 26% and 28% might seem reasonable, but when combined with state taxes, your effective rate often exceeds regular federal income tax rates. Maryland retirees, for instance, face state rates up to 5.75% on top of federal AMT.

Pre-Retirement AMT Planning Strategies

Timing is everything when it comes to AMT planning. Many discover their AMT liability only after exercising stock options during retirement transition—when planning opportunities have already passed.

Consider these strategies before retirement:

- Spread ISO exercises across multiple years to stay below AMT thresholds

- Accelerate regular income in non-AMT years to offset AMT preference items

- Consider Roth conversions in low-AMT years to reduce future required minimum distributions

- Time charitable deductions to maximize benefit in regular tax years

The key is identifying potential AMT years early in your retirement planning process. This allows you to structure withdrawals, Roth conversions, and other income events to minimize the overall tax impact.

Alternative Minimum Tax planning requires a comprehensive view of your retirement income sources and timing. Getting these details wrong can cost tens of thousands over retirement, but most AMT surprises are completely avoidable with proper planning.

If you want to see how AMT planning fits into your specific retirement situation, take our free Retire Ready Score for personalized guidance.