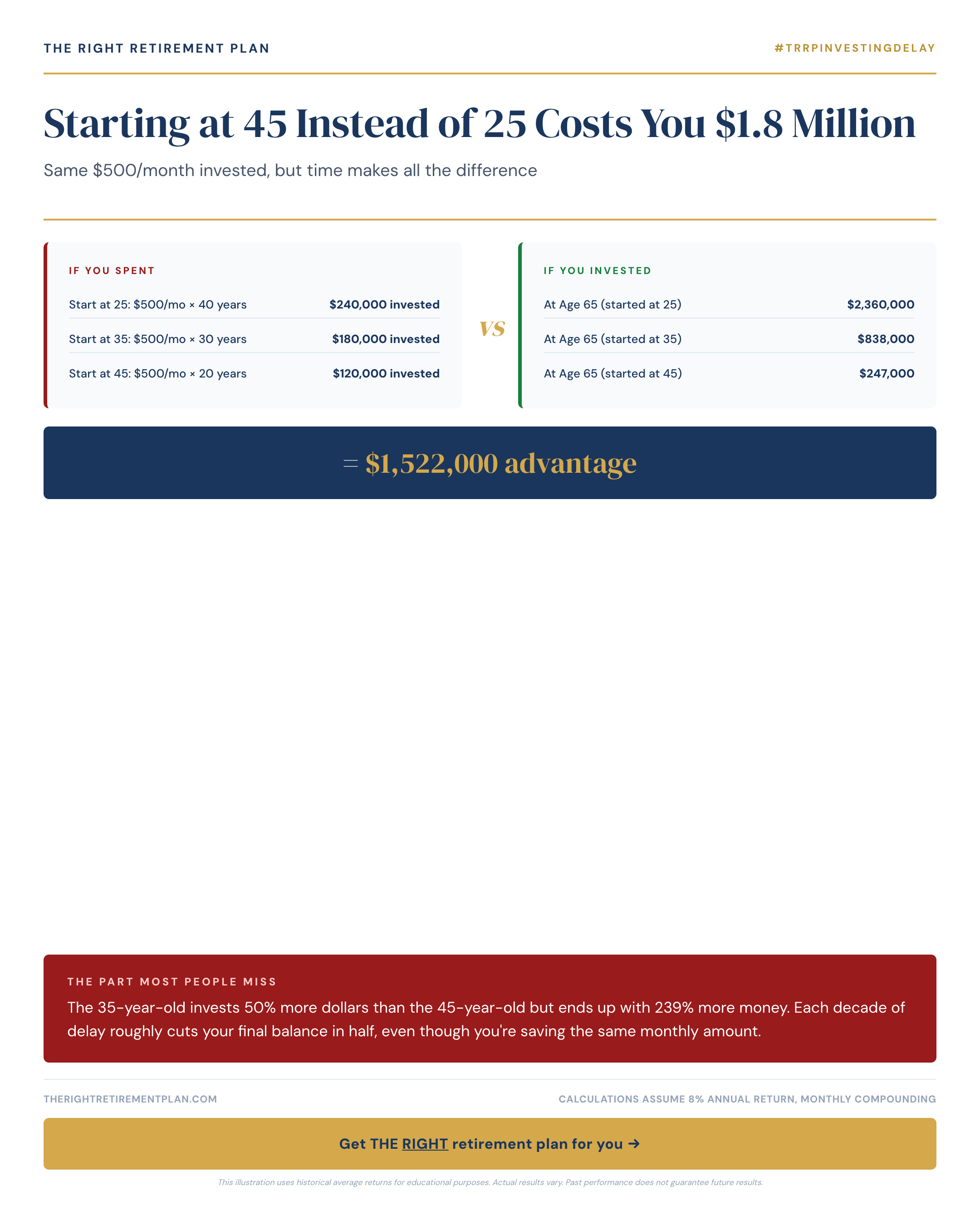

The math behind retirement savings timing is sobering. An investor who starts at 25 and contributes $500 monthly until age 65 accumulates approximately $2.1 million. Wait until 45 to begin the same $500 monthly contributions, and you'll end up with just $328,000 by retirement.

That 20-year delay costs you $1.8 million, despite investing the exact same amount each month.

Why Time Trumps Everything in Retirement Planning

The power of compound growth explains this dramatic difference. When you start at 25, your money has 40 years to grow and compound. Each dollar invested early benefits from decades of market returns building upon previous returns.

Consider these key factors:

- Investment timeline: The 25-year-old invests for 40 years versus 20 years for the 45-year-old

- Compound growth: Early investments experience exponential growth over time

- Market returns: Assuming a 7% annual return, money doubles approximately every 10 years

The 45-year-old actually invests 50% more total dollars ($120,000 versus $240,000) but ends up with 239% less money. Each decade of delay roughly cuts your final retirement balance in half.

Recovery Strategies for Late Starters

If you're starting retirement planning later in life, don't panic. Maryland retirees and others across the Mid-Atlantic have several catch-up options available in 2026:

- Increased 401(k) contributions: Workers 50 and older can contribute an additional $7,500 in catch-up contributions beyond the standard $23,500 limit

- IRA catch-up contributions: An extra $1,000 annually for those 50-plus, on top of the $7,000 standard limit

- Delayed retirement: Working even two extra years can significantly boost your retirement security

- Higher savings rate: Consider increasing your monthly contributions to 15-20% of income

The key is maximizing every available year of compound growth while taking advantage of catch-up contribution limits designed specifically for older workers.

Starting your retirement planning journey requires understanding these timing dynamics and creating a strategy that maximizes your remaining years until retirement. If you want personalized guidance on how these principles apply to your specific situation, consider taking our Retire Ready Score for a comprehensive assessment.