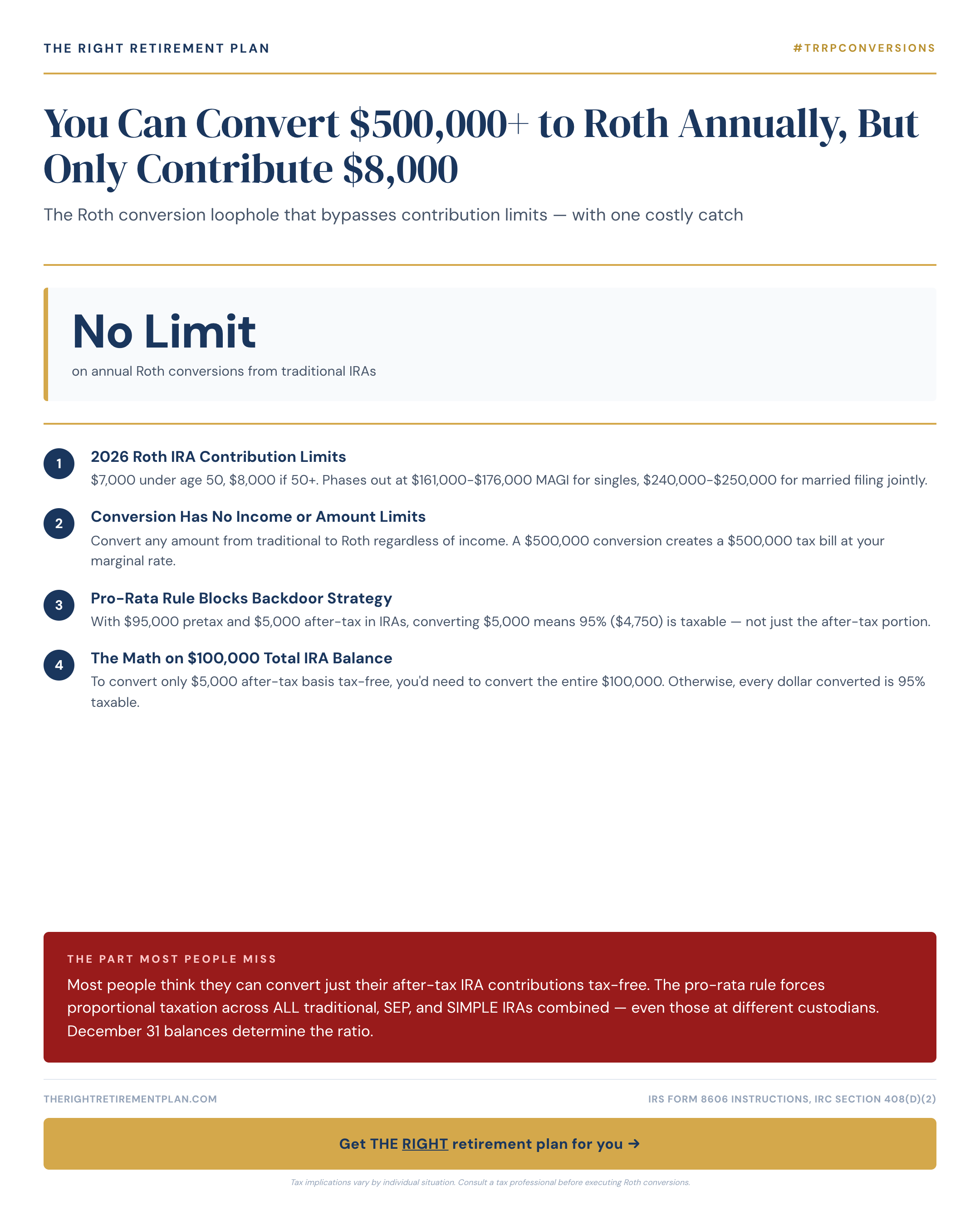

You Can Convert $500,000+ to Roth Annually, But Only Contribute $8,000

Learn how wealthy retirees convert unlimited amounts to Roth IRAs annually while contribution limits cap others at $8,000. The pro-rata rule creates a costly catch most advisors miss.