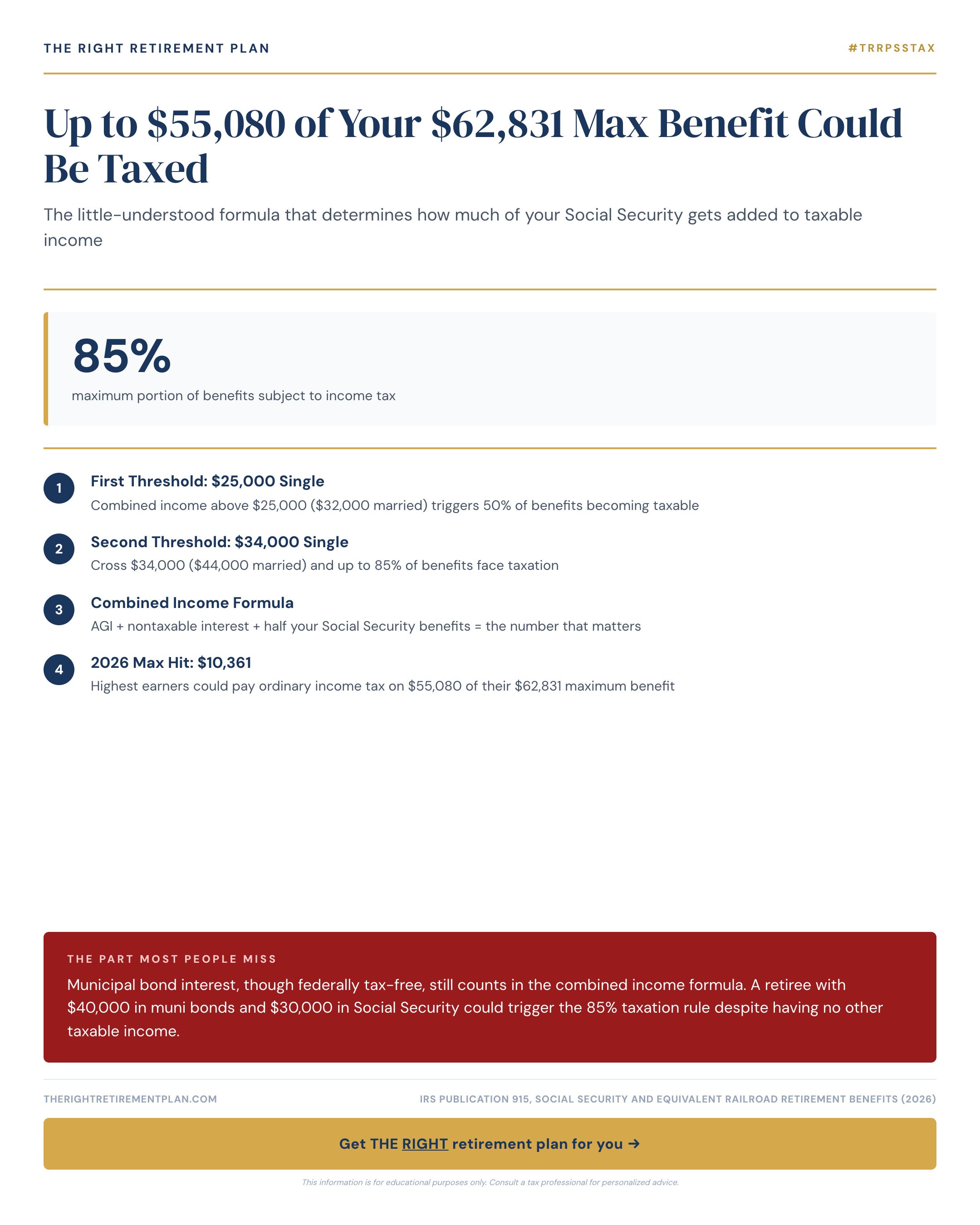

When you hit your maximum Social Security benefit of $62,831 in 2026, you might assume you're set. But here's the reality: up to $55,080 of that benefit could become taxable income if you're not careful about how the IRS calculates what they call "combined income."

How Social Security Taxation Really Works

The Social Security taxation formula catches many retirees off guard. Your "combined income" includes your adjusted gross income, plus half of your Social Security benefits, plus any tax-exempt interest income.

Here are the key thresholds for 2026:

- Single filers: 50% of benefits taxed if combined income exceeds $25,000; 85% taxed above $34,000

- Married filing jointly: 50% of benefits taxed above $32,000; 85% taxed above $44,000

This means a single retiree receiving the maximum benefit needs only $9,416 in other income to trigger the 85% taxation rule. For married couples, it's just $22,415 in additional income between both spouses.

The Hidden Tax Trap Nobody Talks About

Municipal bond interest creates a particularly sneaky trap. While these bonds are federally tax-free, they still count toward your combined income calculation for Social Security purposes.

Consider this example: A Maryland retiree with $40,000 in municipal bond interest and $30,000 in Social Security benefits would have a combined income of $55,000 ($40,000 + $15,000). Despite having no other "taxable" income, this person would still face taxation on 85% of their Social Security benefits.

The same trap applies to:

- Traditional IRA and 401(k) withdrawals

- Pension income

- Part-time work earnings

- Investment dividends and capital gains

Strategic Planning Makes the Difference

Retirement tax planning isn't just about this year—it's about the next 20-30 years. Small decisions about withdrawal timing, Roth conversions, and asset allocation can save you tens of thousands of dollars over your retirement.

Working with experienced advisors in the Annapolis area or anywhere in the Mid-Atlantic can help you model different scenarios and find strategies that minimize your lifetime tax burden while maximizing your Social Security benefits.

If you want personalized guidance on how Social Security taxation might affect your specific situation, consider taking our Retire Ready Score for a comprehensive assessment of your retirement readiness.