Understanding the Wash Sale Rule's 61-Day Trap

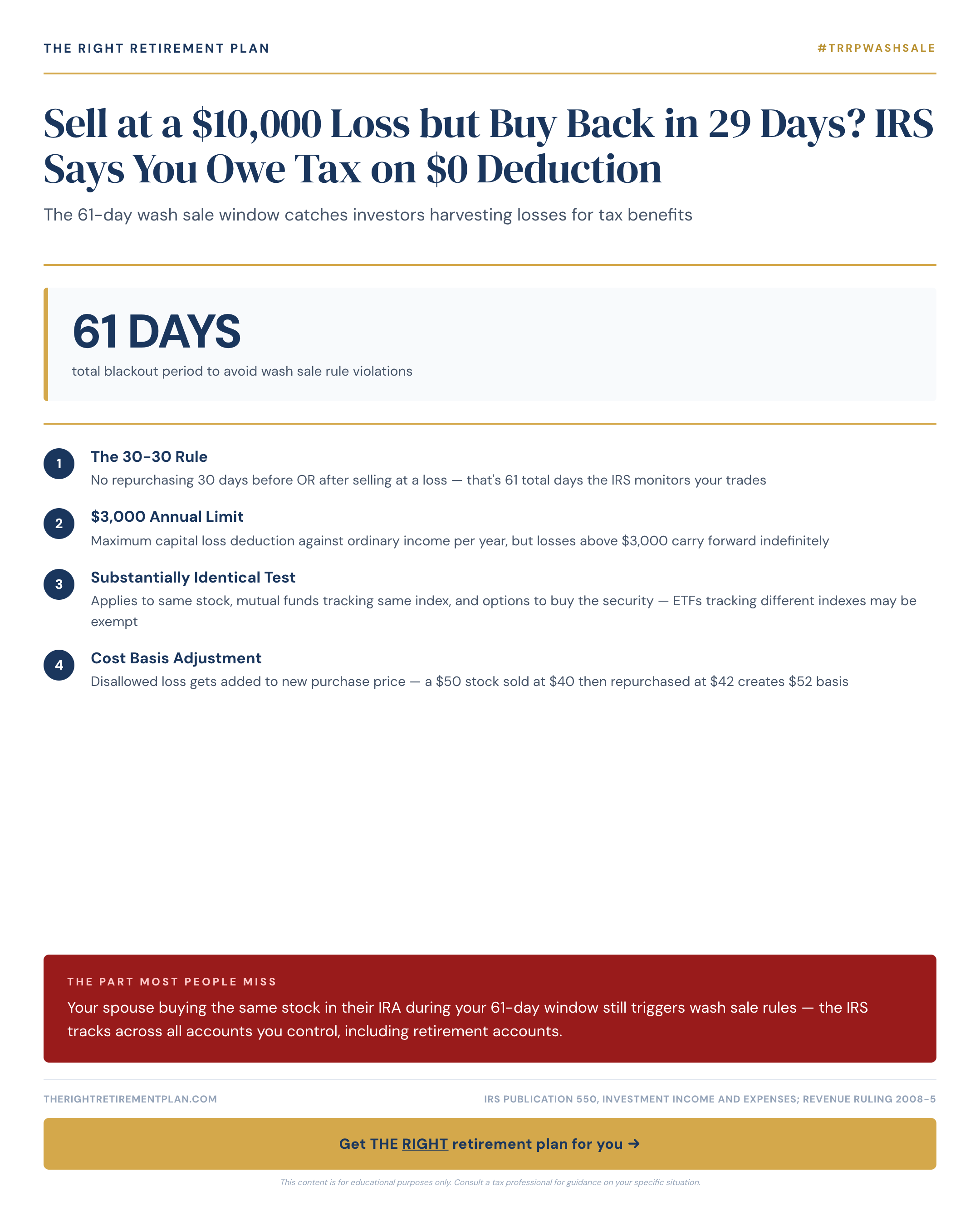

The wash sale rule prevents investors from claiming tax deductions on investment losses while immediately repurchasing the same or "substantially identical" securities. Here's the catch: the IRS doesn't just look at the day you sell—they examine a full 61-day period (30 days before plus 30 days after your sale, plus the sale date itself).

Let's say you sell 100 shares of Apple stock on December 15th for a $10,000 loss. If you buy Apple shares again anytime between November 15th and January 14th, the IRS disallows your entire $10,000 loss deduction. This applies even if you wait 29 days—you need to wait at least 31 days to avoid the wash sale rule.

The rule gets more complex when family members are involved. If your spouse purchases the same stock during your 61-day window, it still triggers the wash sale provisions. The same applies to purchases in IRAs, 401(k)s, or any retirement account you control.

Why This Matters for Pre-Retirees

Tax loss harvesting becomes increasingly important as you approach retirement, especially when managing taxable investment accounts alongside retirement savings. Many advisors in the Annapolis area emphasize this strategy during year-end planning sessions.

Consider these scenarios where wash sale rules commonly trip up investors:

- Selling losing positions in December for tax benefits, then repurchasing in January

- Automatic dividend reinvestment programs buying shares during your wash sale window

- Spouse or family members unknowingly purchasing the same securities

- Rebalancing retirement accounts while harvesting losses in taxable accounts

The financial impact compounds over time. A $10,000 disallowed deduction could cost you $2,200-$3,700 in additional taxes, depending on your bracket. For pre-retirees managing multiple accounts, these mistakes can accumulate significantly.

Avoiding Costly Wash Sale Mistakes

To safely harvest tax losses while maintaining market exposure, consider purchasing securities in different sectors or asset classes during the waiting period. Alternatively, buy a similar but not substantially identical investment—such as swapping one S&P 500 ETF for another that tracks a different broad market index.

Understanding these tax planning nuances becomes crucial as retirement approaches and your investment strategy shifts toward preservation and income generation. If you want personalized guidance on how wash sale rules and other tax strategies apply to your situation, consider taking our Retire Ready Score assessment.