How Delayed Social Security Credits Work

Waiting to claim Social Security past your full retirement age of 67 earns you delayed retirement credits worth 8% annually. This isn't a one-time bonus — it's a permanent increase that affects every check for life, plus any future survivor benefits.

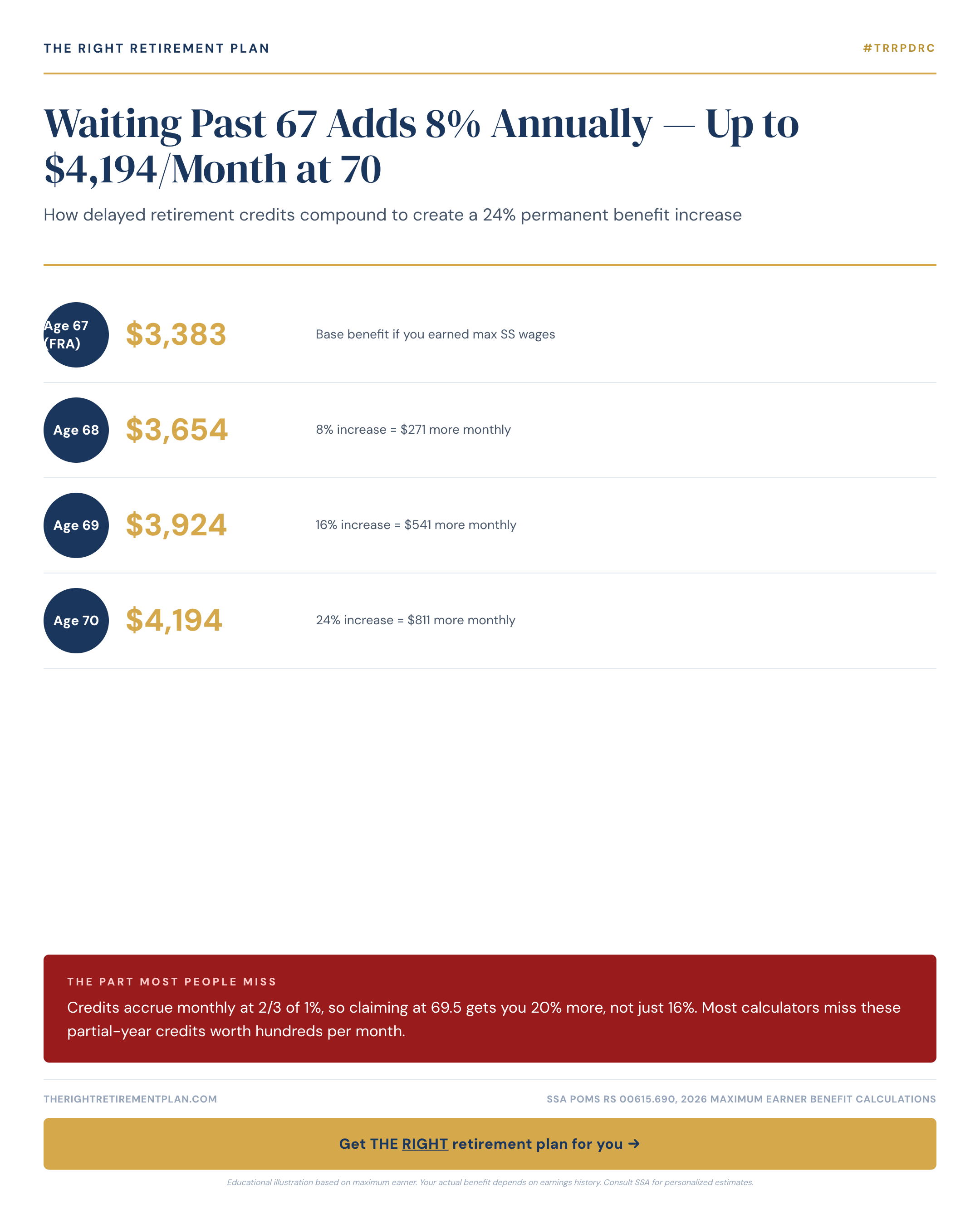

The math is compelling. According to the Social Security Administration, the maximum benefit at full retirement age in 2026 is $3,822 per month. Wait until 70, and that jumps to $4,194 — an extra $372 monthly or $4,464 annually. Over a 20-year retirement, that's nearly $90,000 in additional guaranteed income.

Here's what most people miss: Credits accrue monthly at 2/3 of 1%, making partial-year delays valuable:

- Age 68: 8% increase

- Age 69: 16% increase

- Age 69.5: 20% increase

- Age 70: 24% increase

That seemingly small difference between 69 and 69.5 adds $100 monthly for life on a $2,500 base benefit — potentially worth $24,000 over retirement.

Break-Even Math and Life Expectancy

Every delayed claiming decision involves trading current benefits for larger future payments. The break-even point typically falls around age 82-83.

Consider a $2,800 monthly benefit at age 67. Delaying to 70 means forfeiting $100,800 over three years but gaining $672 extra monthly thereafter. You'd need roughly 150 months of higher payments to break even — about 12.5 years.

According to SSA life tables, a 67-year-old man can expect to live to 84.5, and a woman to 87. For married couples, there's a 72% chance at least one spouse lives past 85. These numbers generally favor delaying, especially for the higher-earning spouse whose benefit becomes the survivor benefit floor.

Factors favoring delay include:

- Good health and family longevity

- Younger spouse who may need survivor benefits

- Sufficient other income during gap years

- Desire for maximum guaranteed lifetime income

Tax and Medicare Considerations

Higher Social Security benefits can trigger additional taxes and Medicare premium surcharges. In 2026, Social Security becomes partially taxable when "combined income" exceeds $25,000 for singles or $32,000 for married couples filing jointly.

A retiree with $41,664 in annual Social Security benefits and $30,000 in other income faces combined income of roughly $50,832 — meaning 85% of benefits become taxable. Maryland retirees and others in higher-tax states should factor state income taxes into their calculations as well.

Medicare's Income-Related Monthly Adjustment Amount (IRMAA) adds another wrinkle. The 2026 thresholds begin at $106,000 for singles, potentially adding $70-$419 monthly to Medicare premiums for high earners.

Your Social Security decision intersects with tax planning, Medicare costs, and retirement income sequencing in complex ways. If you want to see how these factors apply to your complete financial picture, our Retire Ready Score can help assess where your current plan stands.