Required minimum distributions become more aggressive as you age, and the math behind these increases catches many retirees off guard. The IRS Uniform Lifetime Table doesn't just require steady withdrawals—it forces accelerating percentages that can push you into higher tax brackets faster than expected.

How RMD Percentages Accelerate

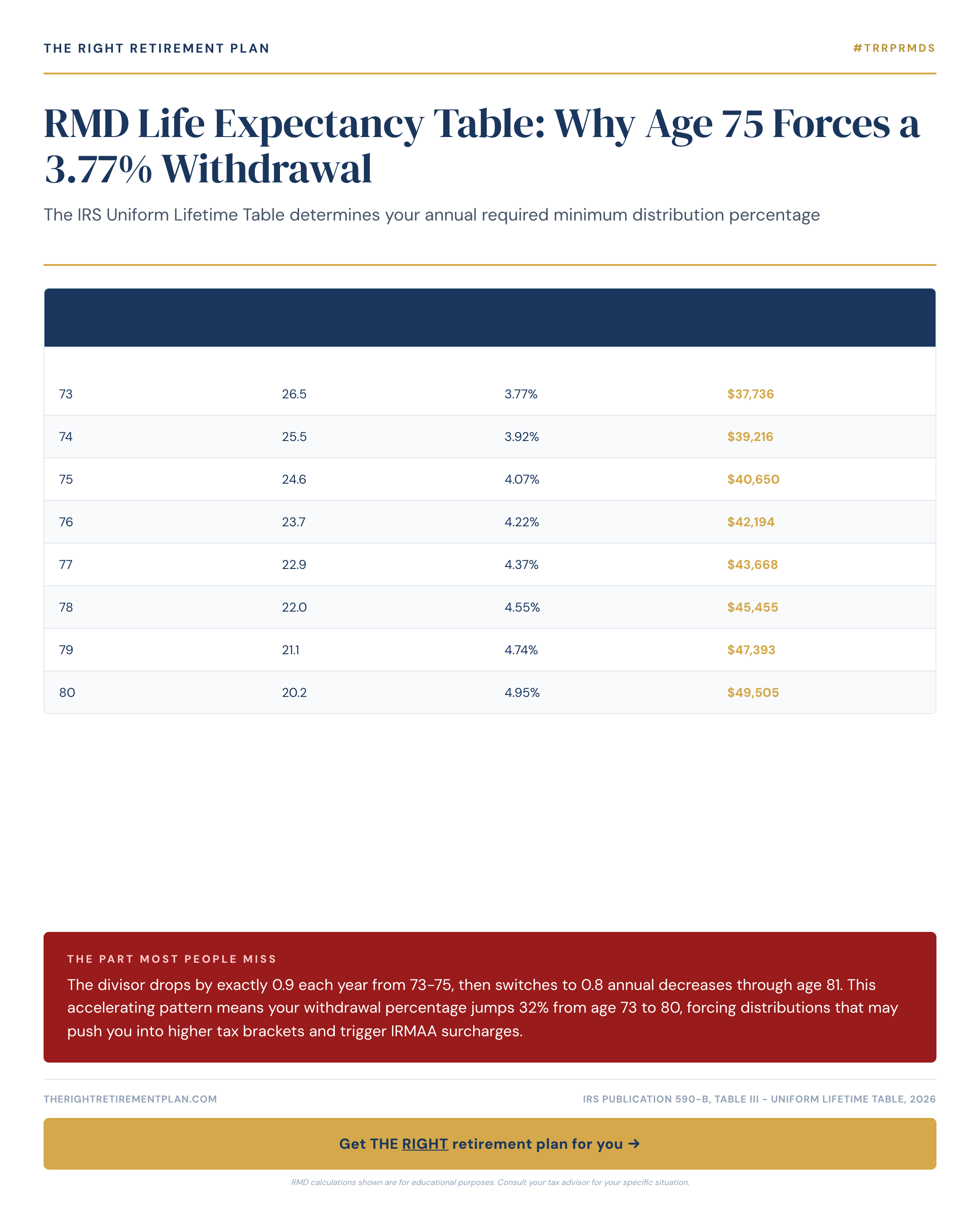

At age 73, you'll withdraw 2.74% of your retirement account balance (divisor of 26.5). By age 75, that percentage jumps to 3.77% (divisor of 24.6). This represents a 38% increase in your withdrawal rate in just two years.

The pattern becomes more pronounced as you age:

- Ages 73-75: Divisor drops by 0.9 each year

- Ages 76-81: Divisor drops by 0.8 annually

- Age 82+: Decreases become more variable

This accelerating structure means your RMD percentage climbs from 2.74% at 73 to 4.95% at age 80—an 81% increase that forces much larger distributions whether you need the income or not.

Tax Bracket and Medicare Implications

These escalating required minimum distributions create planning challenges that extend beyond simple tax calculations. As your mandatory withdrawals increase, you may find yourself pushed into higher federal tax brackets, paying 22% or even 24% on income you didn't necessarily want to receive.

Maryland retirees face additional considerations, as the state taxes retirement account distributions as ordinary income. More concerning are potential Medicare IRMAA surcharges, which can add hundreds of dollars monthly to your Medicare Part B and Part D premiums when your modified adjusted gross income exceeds certain thresholds.

The 2026 IRMAA thresholds start at $103,000 for single filers and $206,000 for married couples filing jointly. Once your RMDs push you over these limits, you'll pay income-related monthly adjustment amounts that can persist for years.

Strategic Planning Approaches

Smart RMD planning starts years before your first distribution. Consider Roth conversions during lower-income years to reduce future account balances subject to RMDs. Some retirees benefit from qualified charitable distributions, which satisfy RMD requirements without adding to taxable income.

Working with qualified advisors in the Annapolis area or your local region can help model these scenarios using your specific account balances and income projections.

Understanding these distribution requirements helps you maintain better control over your retirement tax situation. If you want personalized guidance on how RMD planning fits into your overall retirement strategy, consider taking our Retire Ready Score assessment.