The SECURE Act 2.0 fundamentally changed when you must start taking Required Minimum Distributions from your retirement accounts. Instead of the old universal age of 70½, the new law phases in later RMD ages based on your birth year, ultimately reaching age 75 by 2033.

Your RMD Timeline by Birth Year

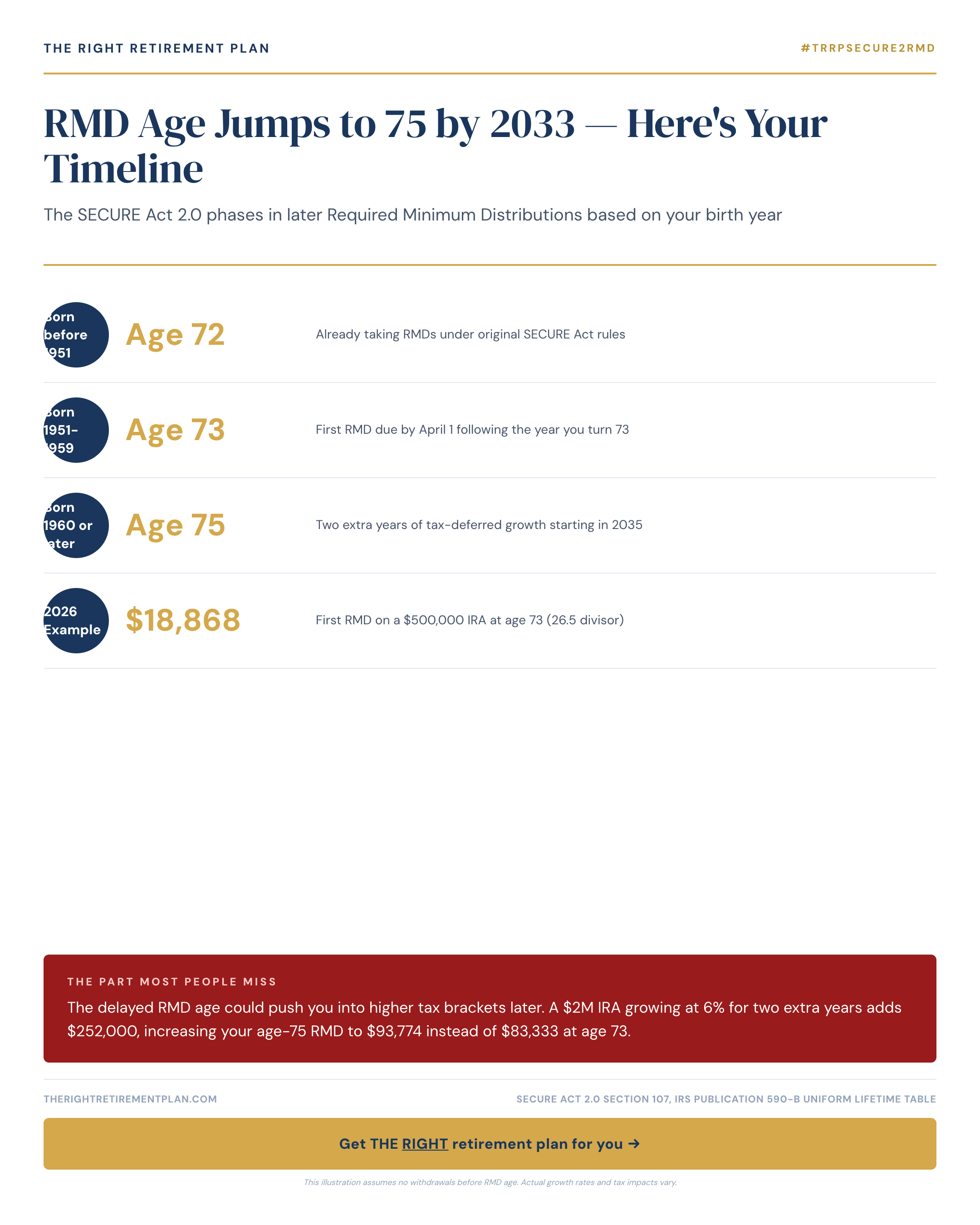

The transition happens gradually:

- Born 1951–1959: RMD age remains 72

- Born 1960 or later: RMD age jumps to 73 in 2026

- Born 1962 or later: RMD age increases to 74 in 2030

- Born 1965 or later: RMD age reaches 75 in 2033

The Hidden Tax Impact

While delayed RMDs sound beneficial, they create a double-edged sword. Your retirement accounts get extra years to grow tax-free, but those larger balances eventually trigger bigger required minimum distributions.

Consider this example: A $2 million IRA growing at 6% annually gains an extra $252,000 over two additional years. Instead of taking your first RMD of $83,333 at age 73, you'd face $93,774 at age 75. That extra $10,441 could push you into a higher tax bracket, especially when combined with Social Security and other retirement income.

The math gets more dramatic over time. Larger account balances mean larger RMDs, which mean higher tax bills throughout your retirement years.

Strategic Planning Opportunities

The delayed timeline creates new planning windows. You have extra years to execute Roth conversions when your income might be lower. This strategy can reduce future required minimum distributions while locking in today's tax rates.

You might also consider charitable giving strategies or tax-loss harvesting in taxable accounts to offset the eventual RMD increases.

Understanding these timeline changes helps you make better decisions about when to retire, how to structure withdrawals, and whether Roth conversions make sense for your situation. If you want personalized guidance on how these RMD changes affect your specific retirement timeline, consider taking our Retire Ready Score for tailored recommendations.