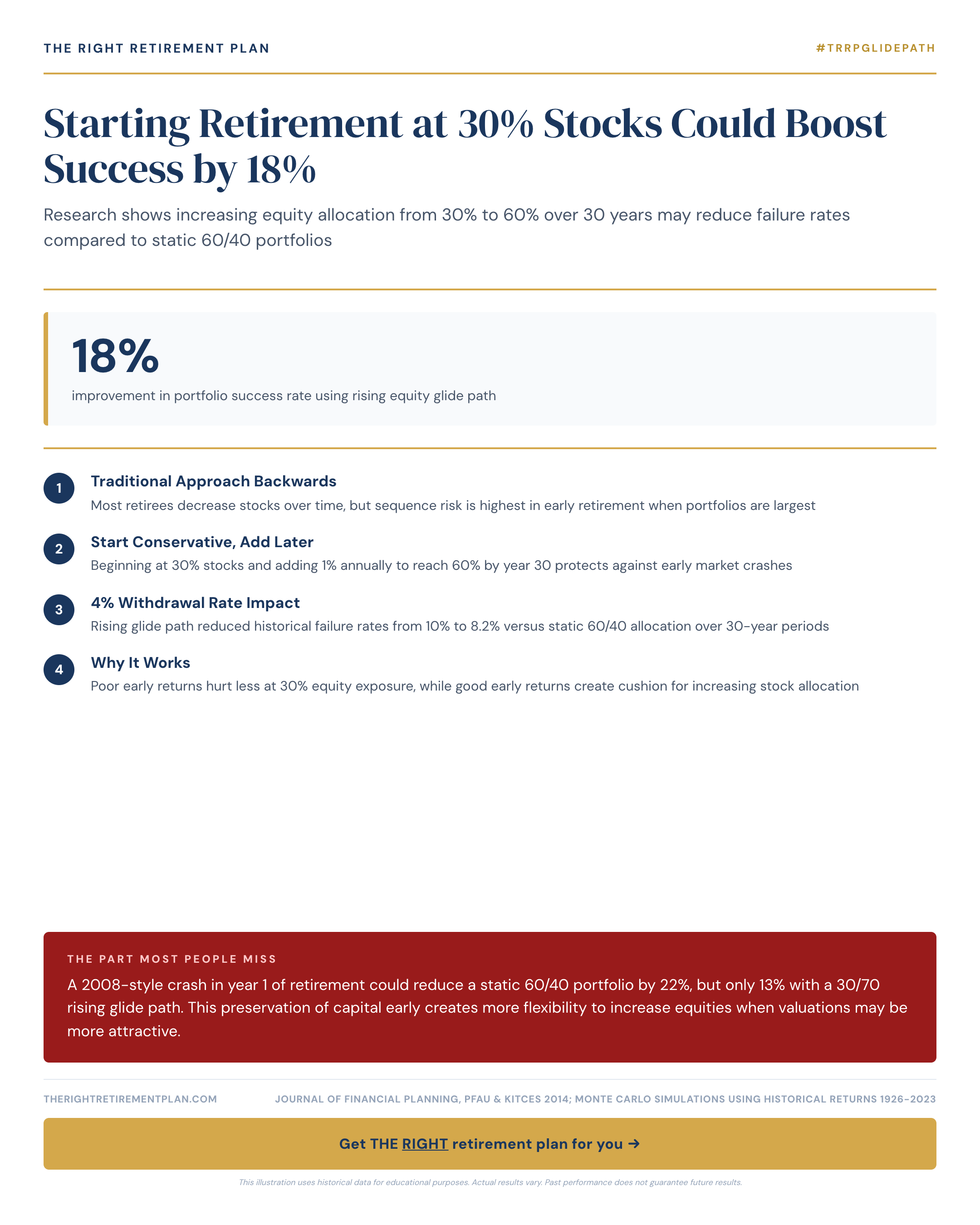

New research is challenging the traditional "set it and forget it" approach to retirement portfolio allocation. Instead of maintaining a static 60% stock, 40% bond portfolio throughout retirement, a dynamic strategy that starts conservative and gradually increases equity exposure could significantly improve your chances of financial success.

The Rising Glide Path Strategy

The rising glide path approach flips conventional wisdom on its head. Rather than starting retirement with high stock allocations when you're most vulnerable to market crashes, this strategy begins with just 30% in stocks and systematically increases to 60% over three decades.

Here's why this matters: A 2008-style market crash in your first year of retirement would devastate a traditional 60/40 portfolio by 22%. The same crash would only reduce a 30/70 rising glide path portfolio by 13%. That 9% difference in preservation during your most vulnerable early retirement years creates tremendous flexibility for the decades ahead.

This approach works because it protects you during the critical first decade when sequence of returns risk poses the greatest threat. By preserving more capital early, you maintain the financial flexibility to increase your stock allocation when market valuations become more attractive and your portfolio has grown larger.

Real-World Impact on Success Rates

The numbers are compelling. Research shows this dynamic allocation strategy can boost portfolio success rates by up to 18% compared to static allocations. For Maryland retirees and others approaching retirement, this could mean the difference between running out of money at 85 versus maintaining financial security well into your 90s.

The strategy works particularly well because it aligns with how spending typically evolves in retirement. Most retirees spend more in their early "go-go" years, then naturally reduce expenses as they age. Starting with lower retirement portfolio allocation to stocks provides the stability you need when expenses are highest.

Getting retirement allocation strategies wrong can cost tens of thousands of dollars over a 30-year retirement. The good news is these mistakes are completely avoidable with proper planning and periodic adjustments to match your changing circumstances.

If you want to see how dynamic allocation strategies might apply to your specific situation, consider taking our free Retire Ready Score for personalized guidance.