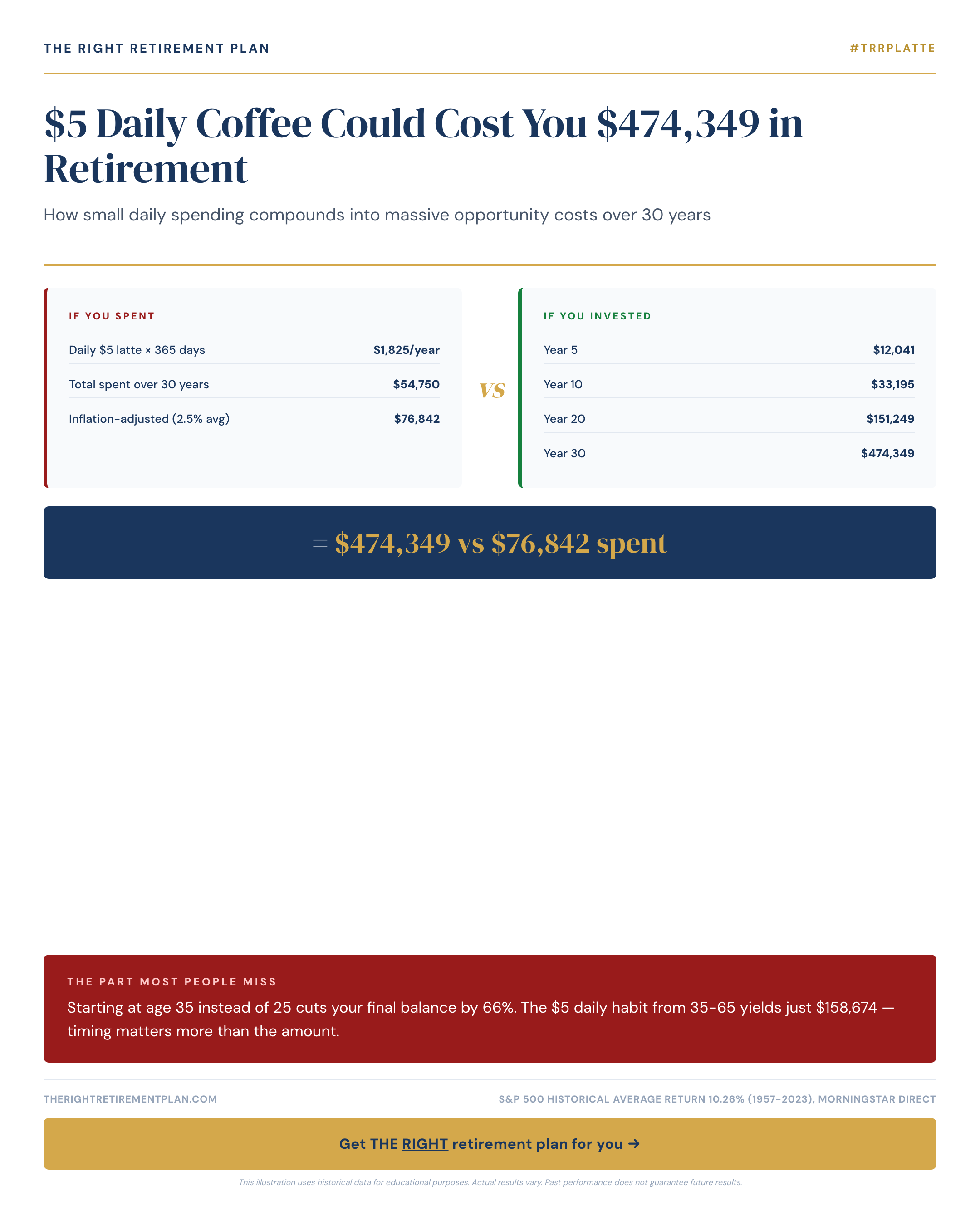

That morning coffee ritual might seem harmless, but the numbers tell a sobering story. A simple $5 daily expense could represent $474,349 in lost retirement wealth when you factor in compound interest and timing.

The Math Behind the Coffee Crisis

The difference isn't just about the coffee money itself—it's about when you start investing. Consider two scenarios:

Starting at 25: Investing $150 monthly (that $5 daily coffee money) from age 25 to 65 with a 7% annual return yields approximately $633,000.

Starting at 35: The same $150 monthly investment from age 35 to 65 generates only $158,674.

That 10-year delay costs you $474,349—a staggering 66% reduction in your final balance. Even though the later starter contributes for 30 years instead of 40, compound interest heavily favors the early bird.

For Maryland retiires and others approaching their golden years, this example illustrates why small spending decisions made decades ago continue to impact your financial security today.

Why Timing Trumps Amount

Compound interest rewards time more than contribution size. Each dollar invested at 25 has 40 years to grow, doubling approximately every 10 years at 7% returns. By contrast, dollars invested at 35 only have 30 years to compound.

The lesson extends beyond coffee to any recurring expense:

- Daily lunch out: $12 × 365 = $4,380 annually

- Premium cable package: $100 monthly = $1,200 annually

- Subscription services: $50 monthly = $600 annually

These seemingly modest expenses, when redirected to retirement accounts, could significantly boost your nest egg when compound growth has decades to work.

The good news? Whether you're 35, 55, or beyond, it's never too late to harness compound interest. While you can't reclaim those early years, you can maximize the time you have left by avoiding common retirement planning mistakes and optimizing your current strategy.

If you want personalized guidance on how these principles apply to your specific situation, consider taking our Retire Ready Score for insights tailored to your retirement timeline.