Understanding the 2026 Tax Bracket Reality

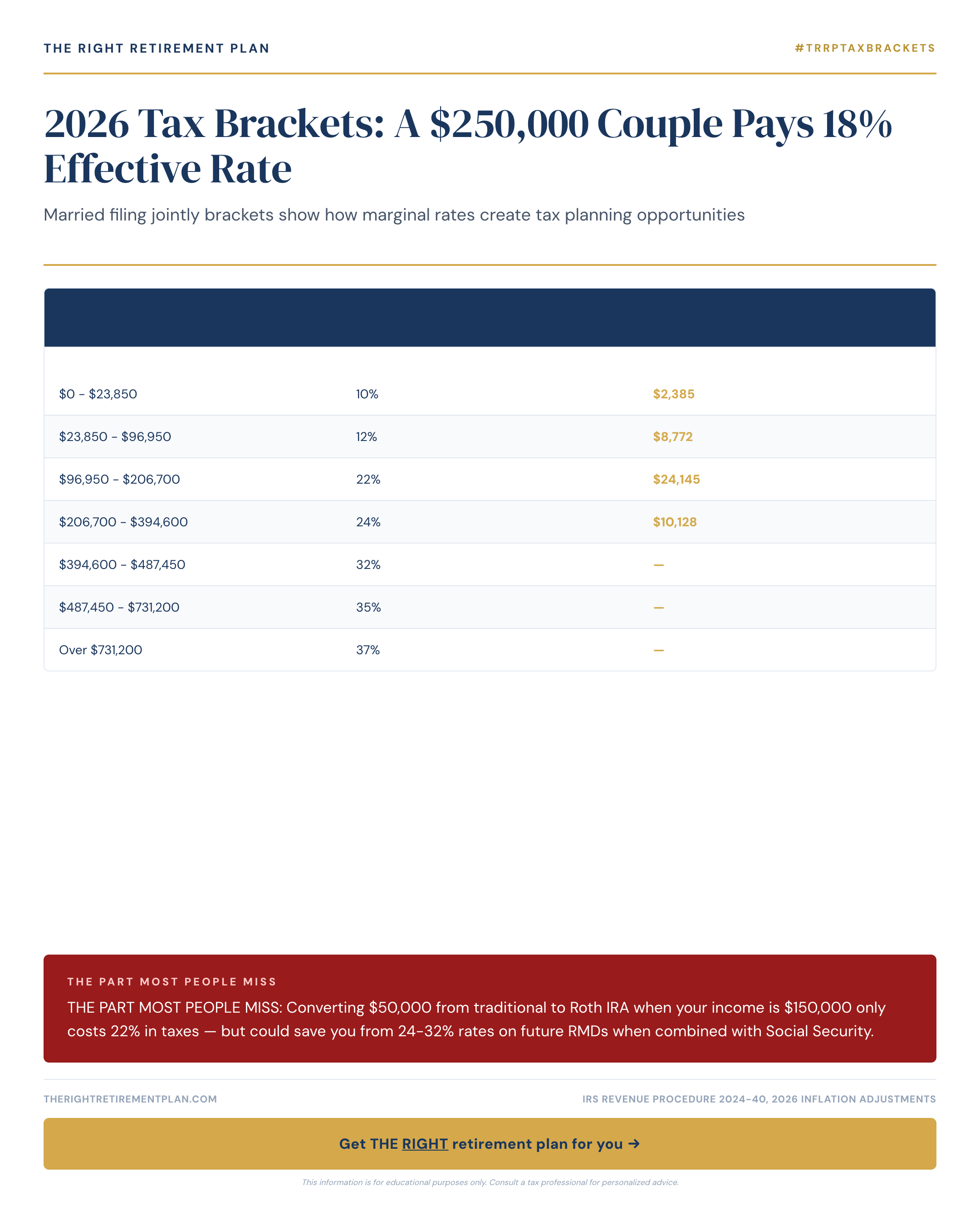

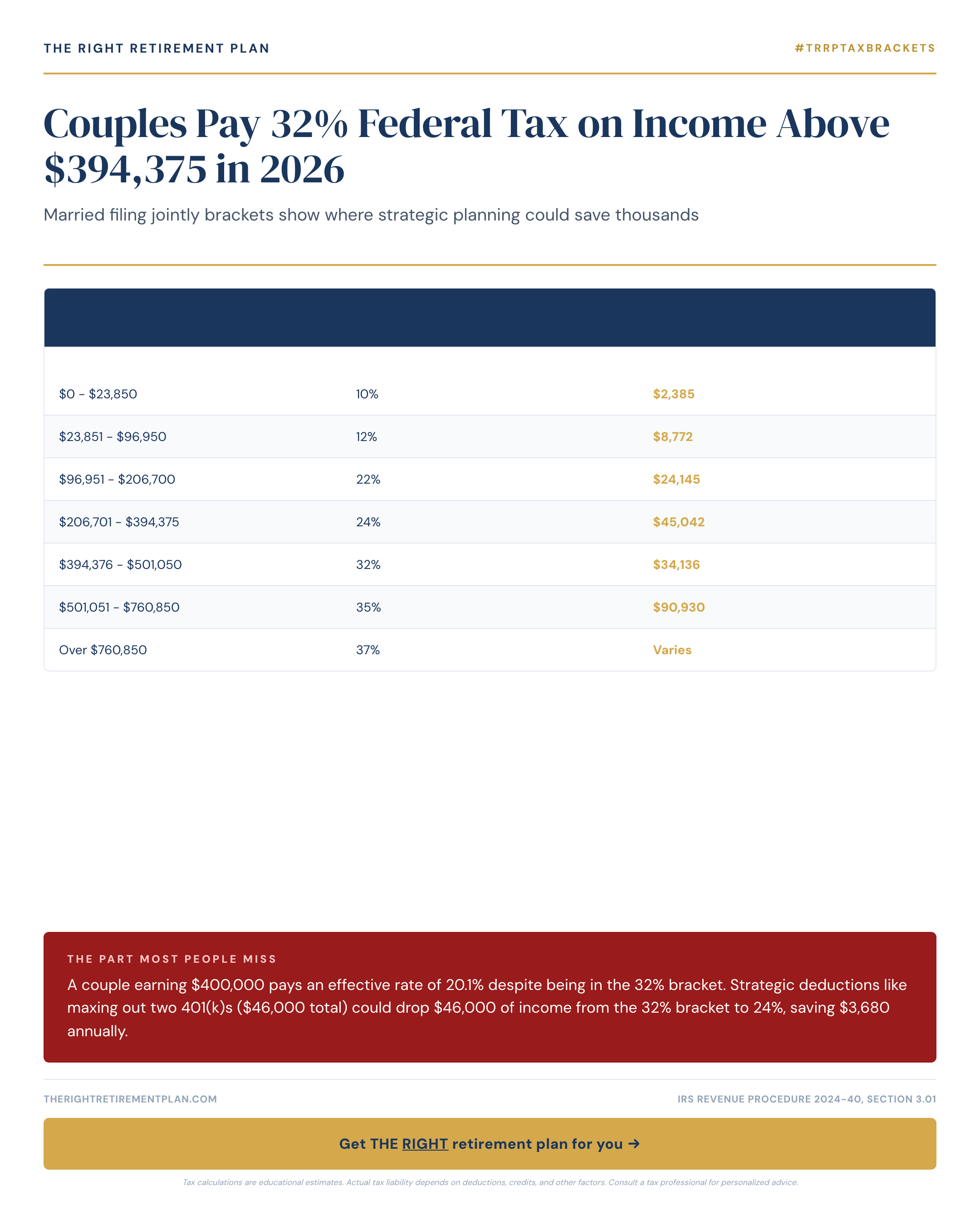

When married couples filing jointly earn $250,000, they don't pay 24% on every dollar—despite being in the 24% bracket. Thanks to how 2026 tax brackets work, their effective rate is actually around 18%.

Here's why: The first $23,200 is taxed at 10%, the next $70,700 at 12%, then $89,450 at 22%, and only the remaining dollars hit 24%. This progressive structure creates significant planning opportunities that many couples overlook.

For 2026, married filing jointly brackets are:

- 10%: $0 to $23,200

- 12%: $23,201 to $93,900

- 22%: $93,901 to $183,350

- 24%: $183,351 to $365,600

- 32%: $365,601 to $462,700

Understanding these thresholds helps Maryland retirees and couples nationwide make smarter decisions about timing income, deductions, and retirement account withdrawals.

Strategic Moves for High-Earning Couples

The gap between marginal and effective rates opens doors for tax-efficient strategies. Consider these moves before you retire:

Roth IRA conversions become attractive when you can fill lower brackets. Converting $50,000 from traditional to Roth when your income sits at $150,000 costs just 22% in current taxes—potentially saving you from 24-32% rates on future required minimum distributions.

Tax-loss harvesting in taxable accounts can offset gains while you're in higher brackets. Charitable giving strategies like donor-advised funds or qualified charitable distributions from IRAs (starting at age 70½) can reduce taxable income efficiently.

HSA maximization offers triple tax benefits: deductible contributions, tax-free growth, and tax-free qualified withdrawals. For 2026, contribution limits are $4,550 for individuals and $9,100 for families.

Building Your Tax-Smart Retirement Plan

Effective retirement tax planning requires looking beyond current brackets to future income scenarios. Consider how pension payments, Social Security benefits, required minimum distributions, and part-time work income will combine in retirement.

Working with qualified advisors who understand these interactions can save thousands over your retirement years. The key is starting these conversations before you need the money.

If you want to see how these tax strategies apply to your specific situation, take our free Retire Ready Score—a quick assessment that evaluates your current plan across income, taxes, healthcare, and protection needs.