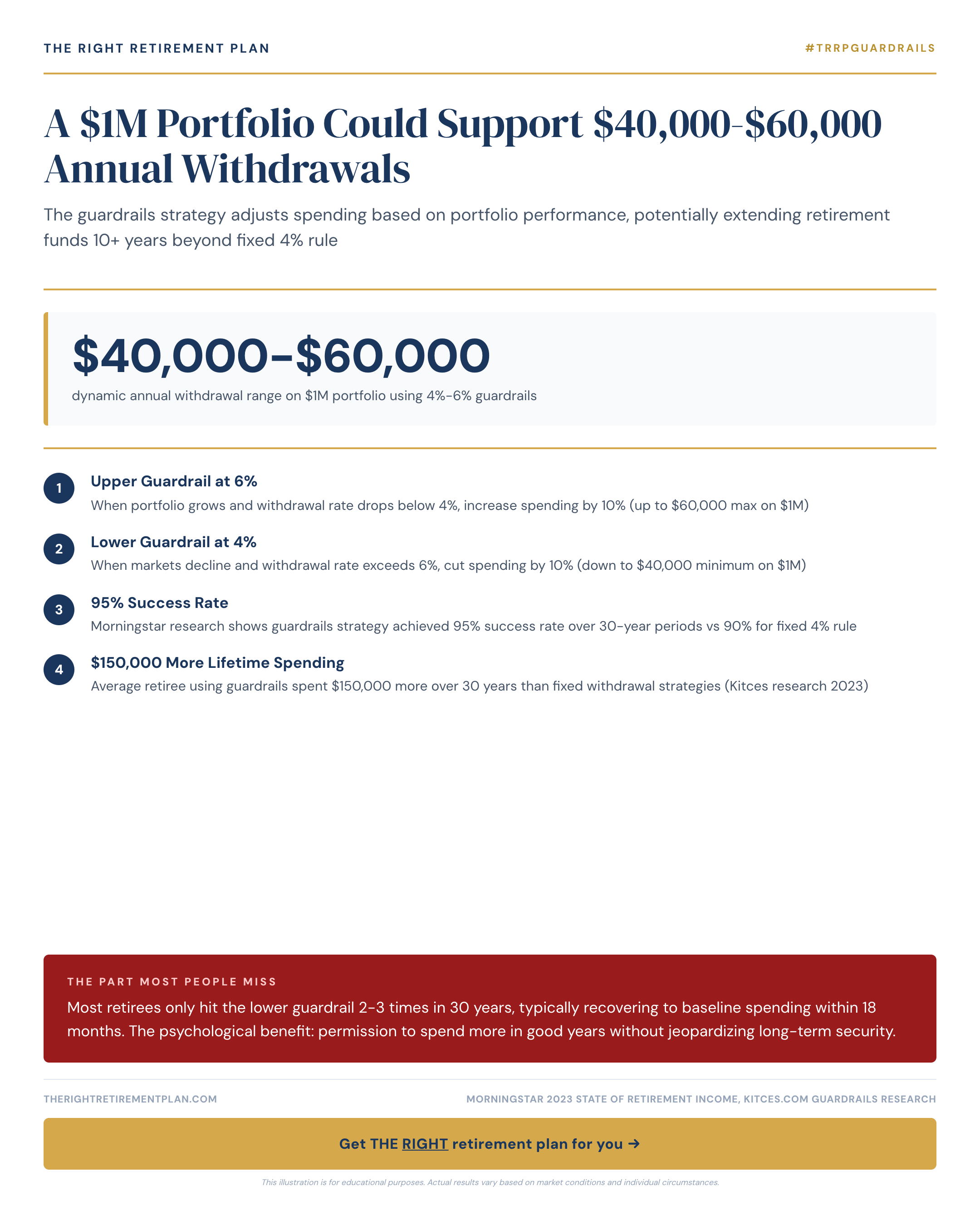

Most retirees stick to the traditional 4% withdrawal rule, limiting themselves to $40,000 annually from a $1 million portfolio. But the guardrails strategy offers a smarter approach that could boost your annual withdrawals to $50,000-$60,000 while actually protecting your money longer.

How the Guardrails Strategy Works

The guardrails strategy adjusts your retirement income based on how your portfolio performs each year. Instead of withdrawing a fixed percentage regardless of market conditions, you increase spending when markets are strong and reduce it slightly when they're weak.

Here's how it typically works:

- Upper guardrail: When your portfolio grows significantly, increase spending by 10-20%

- Lower guardrail: If your portfolio drops below a threshold, reduce spending by 10-15%

- Baseline years: Maintain your target withdrawal rate during normal market conditions

The Psychology Behind Higher Withdrawals

The guardrails strategy addresses a common retirement dilemma: the fear of spending too much early on. By building in automatic adjustments, you get permission to spend more during good market years without jeopardizing long-term security.

Most retirees only hit the lower guardrail 2-3 times over a 30-year retirement. When they do reduce spending, they typically return to baseline levels within 18 months as markets recover. This creates a dynamic withdrawal strategy that balances enjoying your money today with preserving it for tomorrow.

The psychological benefit is enormous. Instead of constantly worrying about market volatility, you have a predetermined plan that adapts to changing conditions automatically.

Retirement planning decisions compound over time, and getting withdrawal strategies wrong can cost tens of thousands of dollars over a retirement. The good news is that these mistakes are completely avoidable when you understand how flexible withdrawal strategies actually work.

If you want to see how the guardrails approach applies to your specific situation, consider taking the Retire Ready Score for personalized guidance on optimizing your withdrawal strategy.