Understanding Medicare Savings Programs

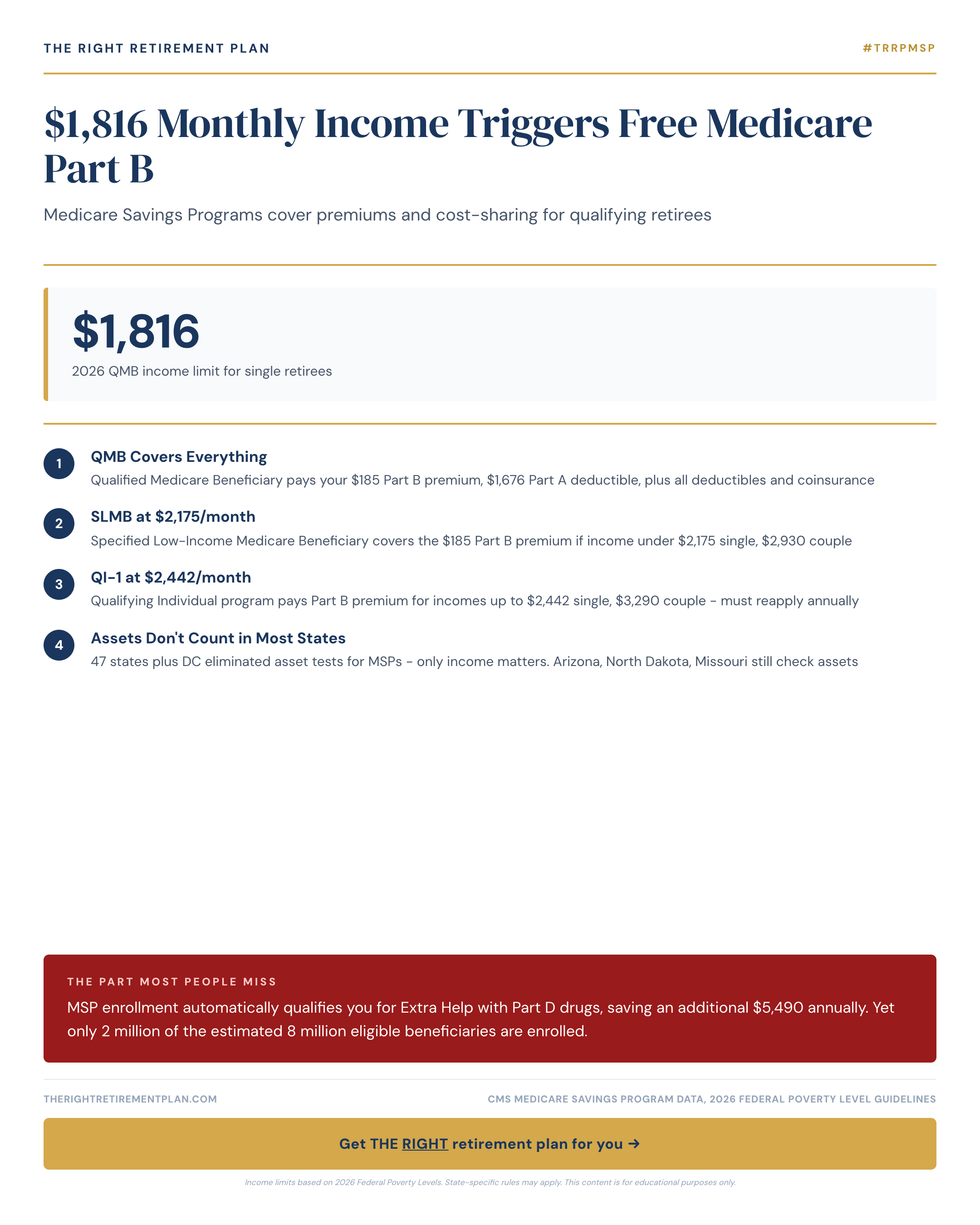

Medicare Savings Programs (MSPs) represent one of retirement's best-kept secrets. If your monthly income falls around $1,816 as an individual (or $2,448 for couples), you could qualify for completely free Medicare Part B coverage through these state-administered programs.

The income thresholds vary slightly by state, but most follow federal guidelines closely. For 2026, the Qualified Medicare Beneficiary (QMB) program covers individuals earning up to 100% of the Federal Poverty Level, while other MSP categories extend coverage to those earning up to 135% or 120% of poverty guidelines.

These programs don't just cover your Medicare Part B premiums—they also eliminate deductibles, copayments, and coinsurance. For many Maryland retirees, this represents savings of $2,000 to $3,000 annually on Medicare costs alone.

The Extra Help Bonus

Here's where Medicare Savings Programs become truly valuable: MSP enrollment automatically qualifies you for Extra Help with Medicare Part D prescription drug costs. This benefit alone saves eligible beneficiaries an average of $5,490 per year in 2026.

Extra Help covers:

- Monthly Part D premiums (often $0)

- Annual deductibles (eliminated)

- Copayments reduced to $4.50 for generics and $11.20 for brand names

- No coverage gap ("donut hole")

- No late enrollment penalties

The combination of free Medicare Part B through MSPs and automatic Extra Help creates substantial healthcare savings that compound throughout retirement.

The Enrollment Gap

Despite these significant benefits, only about 2 million of the estimated 8 million eligible Americans are enrolled in Medicare Savings Programs. This enrollment gap represents billions in unclaimed benefits annually.

Many retirees don't realize they qualify, while others assume the application process is too complicated. In reality, you can apply through your state Medicaid office, and many states have simplified online applications.

Understanding how Medicare Savings Programs work alongside your overall retirement strategy can prevent costly healthcare surprises and preserve more of your retirement savings for the things you actually want to do. If you'd like personalized guidance on how these programs might fit your situation, consider taking our Retire Ready Score for a comprehensive assessment.