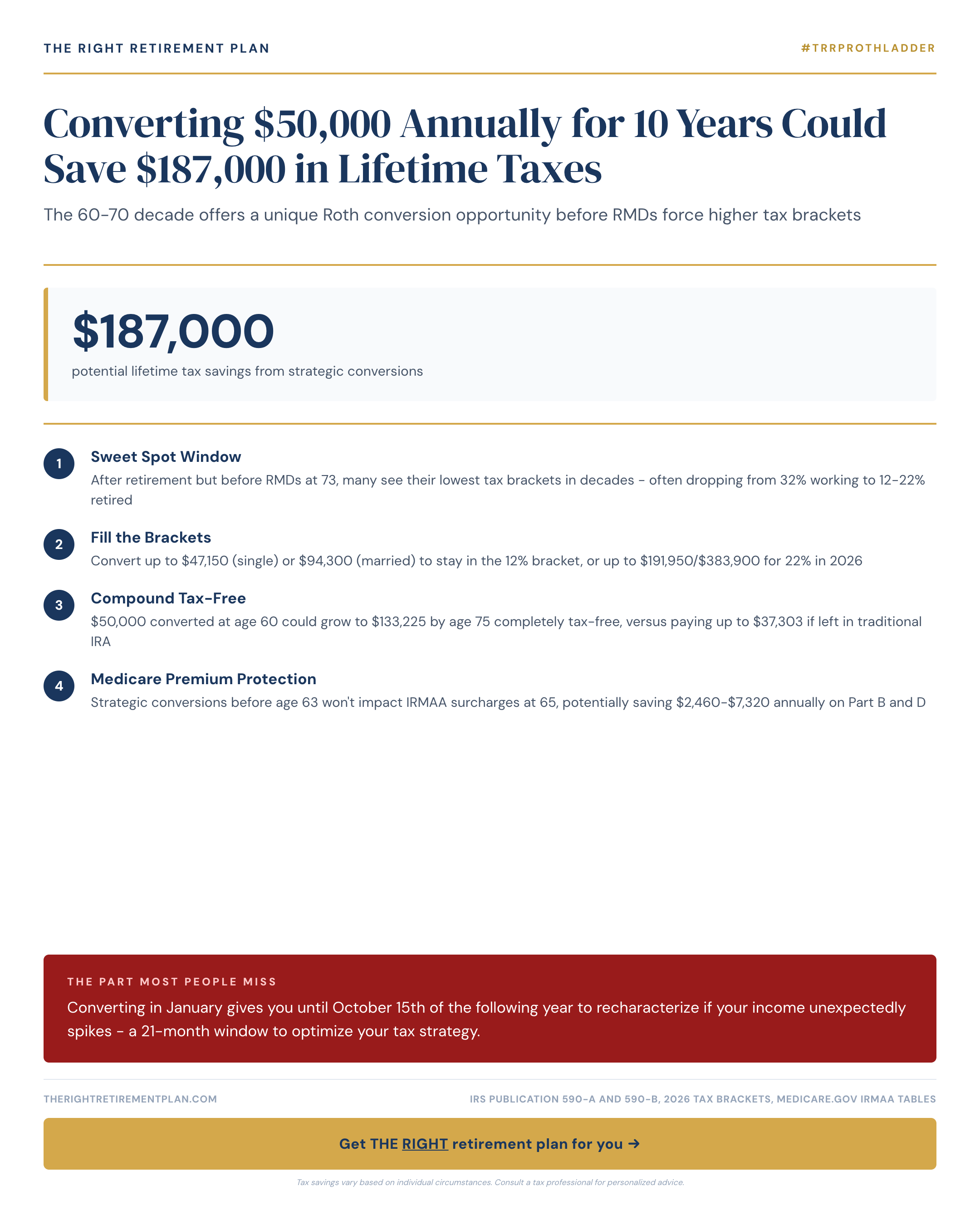

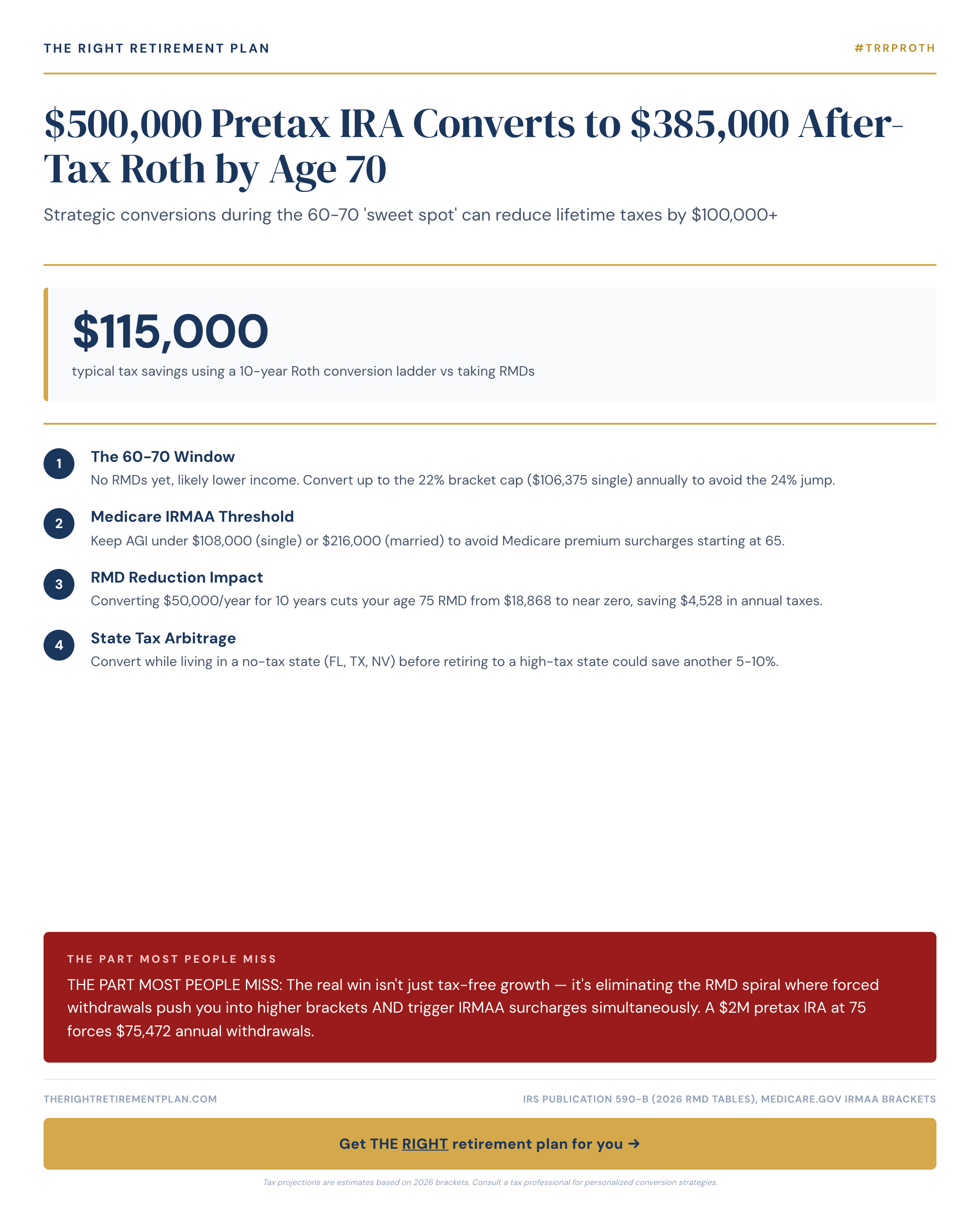

The decade between ages 60 and 70 represents a golden window for Roth IRA conversions. For many pre-retirees, converting $50,000 annually during this period could save an estimated $187,000 in lifetime taxes compared to waiting until required minimum distributions (RMDs) force withdrawals at higher tax rates.

Why the 60-70 Window Works

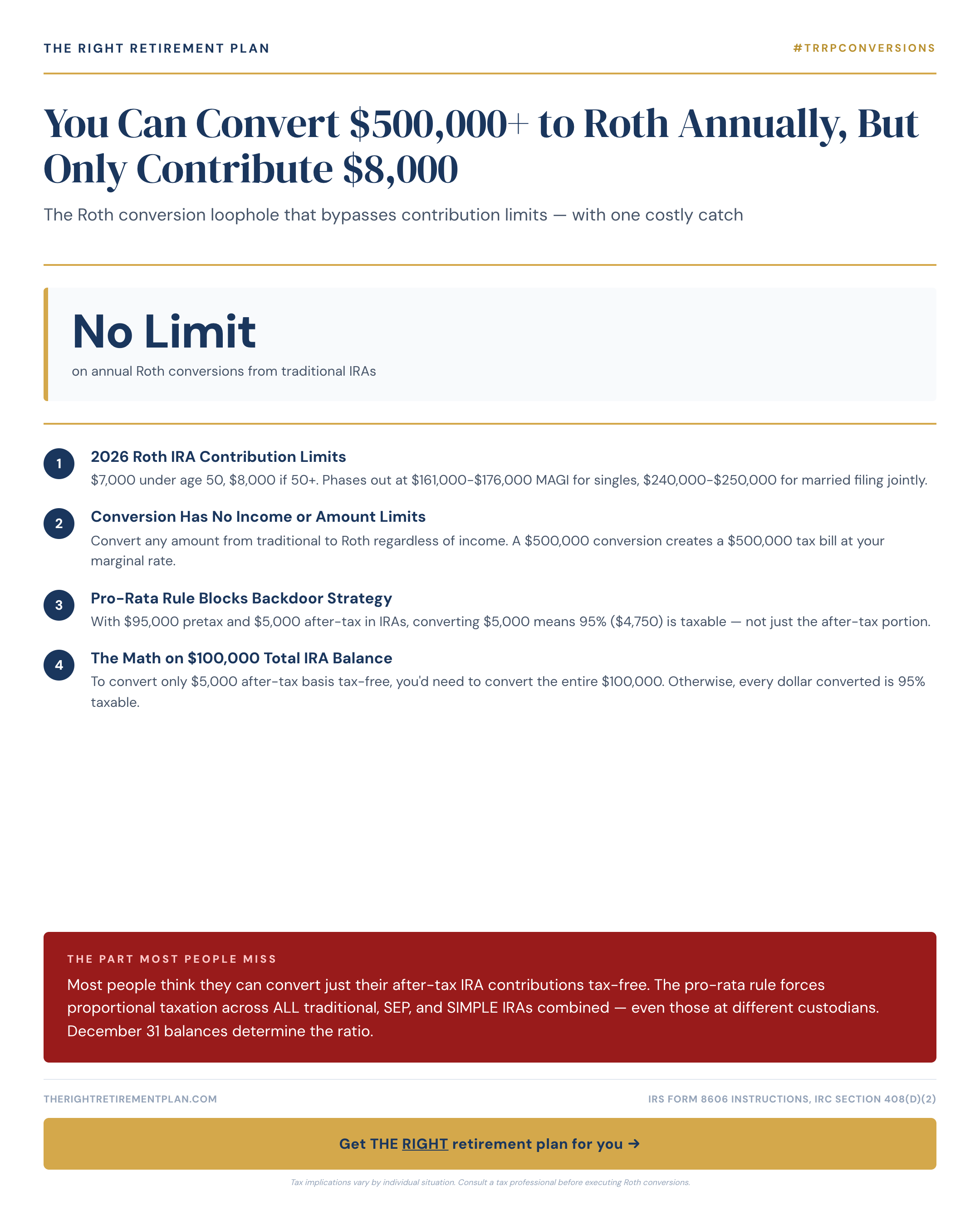

When you reach age 75 in 2026, required minimum distributions kick in, potentially pushing you into higher tax brackets just when you have less control over your income. By converting traditional IRA or 401(k) funds to a Roth IRA during your 60s, you pay taxes now at potentially lower rates and eliminate future RMDs on converted amounts.

The math is compelling for many Maryland retirees and those nationwide. Consider someone with $500,000 in traditional retirement accounts:

• Converting $50,000 annually for 10 years at a 22% tax rate costs $110,000 in taxes

• Without conversions, RMDs starting at 75 could push income into the 24% or 32% brackets

• The tax savings on growth and future withdrawals can exceed $187,000 over a lifetime

Strategic Timing Advantages

Roth conversion strategies offer built-in flexibility that many people overlook. When you convert in January, you have until October 15th of the following year to recharacterize the conversion if your income unexpectedly spikes. That's a 21-month window to optimize your tax strategy.

This extended timeline allows you to:

• Monitor your actual income throughout the year

• Adjust conversion amounts based on market performance

• Reverse conversions if tax situations change unexpectedly

Converting systematically during your 60s—regardless of market ups and downs—often produces better outcomes than trying to time perfect conversion opportunities. The key is finding your optimal annual conversion amount based on your current tax bracket, future income projections, and overall retirement timeline.

Retirement tax planning decisions compound over decades. Getting the conversion strategy wrong can cost tens of thousands of dollars, but understanding how these rules work makes most mistakes completely avoidable.

If you want to see how Roth conversions apply to your specific situation, take our free Retire Ready Score for personalized guidance.