When you reach age 73, the IRS requires you to start taking required minimum distributions (RMDs) from your retirement accounts. But here's where it gets tricky: the aggregation rules differ dramatically between account types, and mixing them up can trigger hefty penalties.

IRA vs. 401(k) Aggregation Rules

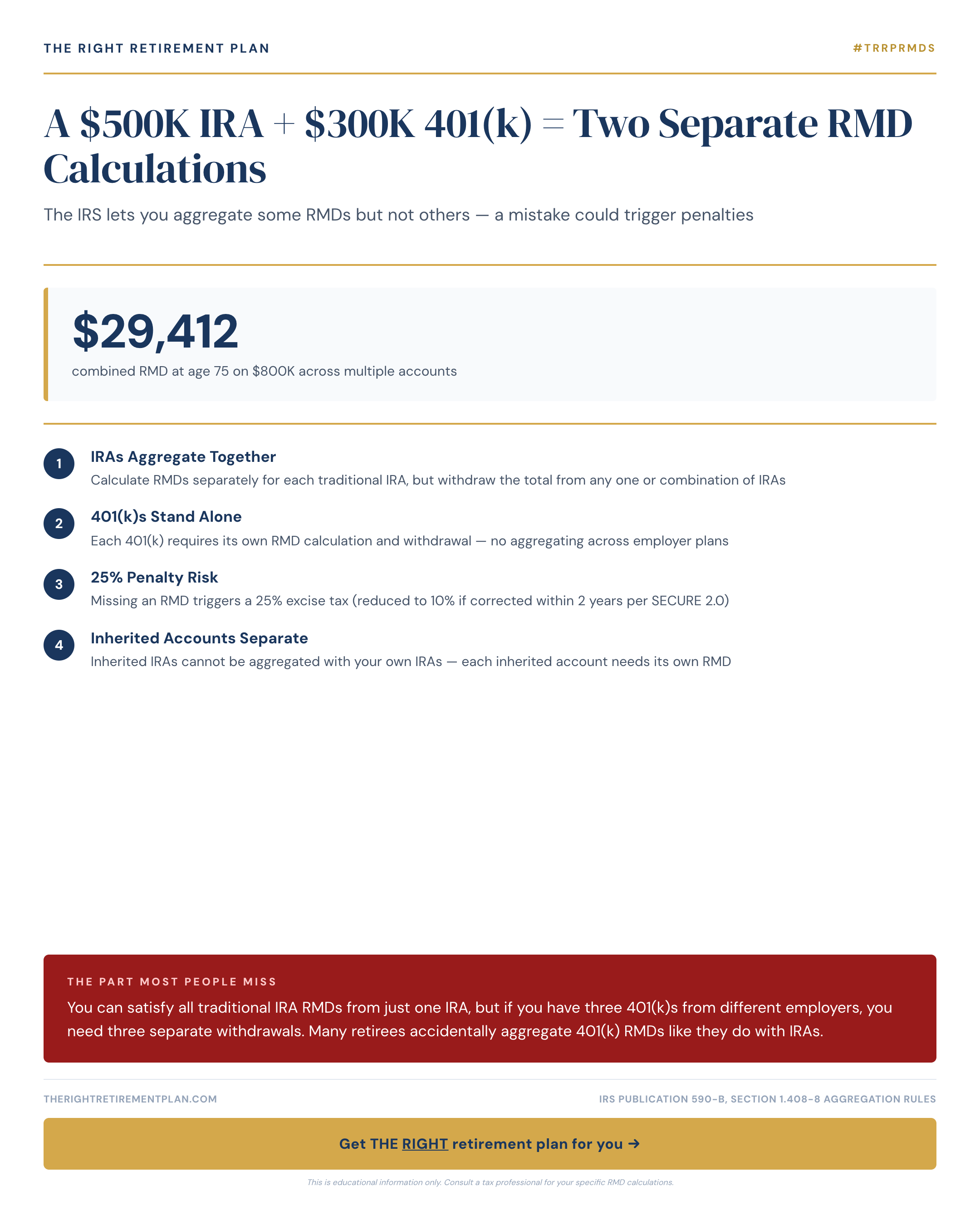

Traditional IRAs offer flexibility. If you have multiple traditional IRAs, you can calculate each account's RMD separately but withdraw the total amount from just one IRA. For example, if your $300,000 IRA requires a $12,000 RMD and your $200,000 IRA requires $8,000, you can take the full $20,000 from either account.

401(k) plans require separate withdrawals. Each 401(k) from different employers demands its own distribution. If you have three 401(k) accounts from previous jobs, you must calculate and withdraw the RMD from each account individually. You cannot combine these withdrawals like you can with IRAs.

This distinction catches many Maryland retirees off guard, especially those who worked for multiple employers throughout their careers.

Common RMD Mistakes That Cost Money

The penalty for missing an RMD is severe: 50% of the amount you should have withdrawn. Here are the most expensive mistakes:

- Taking your entire 401(k) RMD from just one account when you have multiple plans

- Forgetting about an old 401(k) from a previous employer

- Miscalculating the RMD amount using outdated life expectancy tables

- Missing the December 31st deadline (except for your first RMD, which can be delayed until April 1st of the following year)

Smart Strategies for Multiple Accounts

Consider consolidating old 401(k)s into a single IRA rollover before you turn 73. This simplifies your RMD calculations and gives you more withdrawal flexibility. However, evaluate any special benefits your current 401(k) offers, such as low-cost institutional funds or loan options, before rolling over.

You might also coordinate RMD timing with your tax planning strategy, spreading withdrawals throughout the year rather than taking one large distribution in December.

Getting your required minimum distribution strategy right from the start can save you thousands in penalties and taxes over your retirement years. If you want personalized guidance on how these rules apply to your specific situation, consider taking our Retire Ready Score for a comprehensive assessment of your retirement readiness.