Understanding the Net Investment Income Tax Cliff

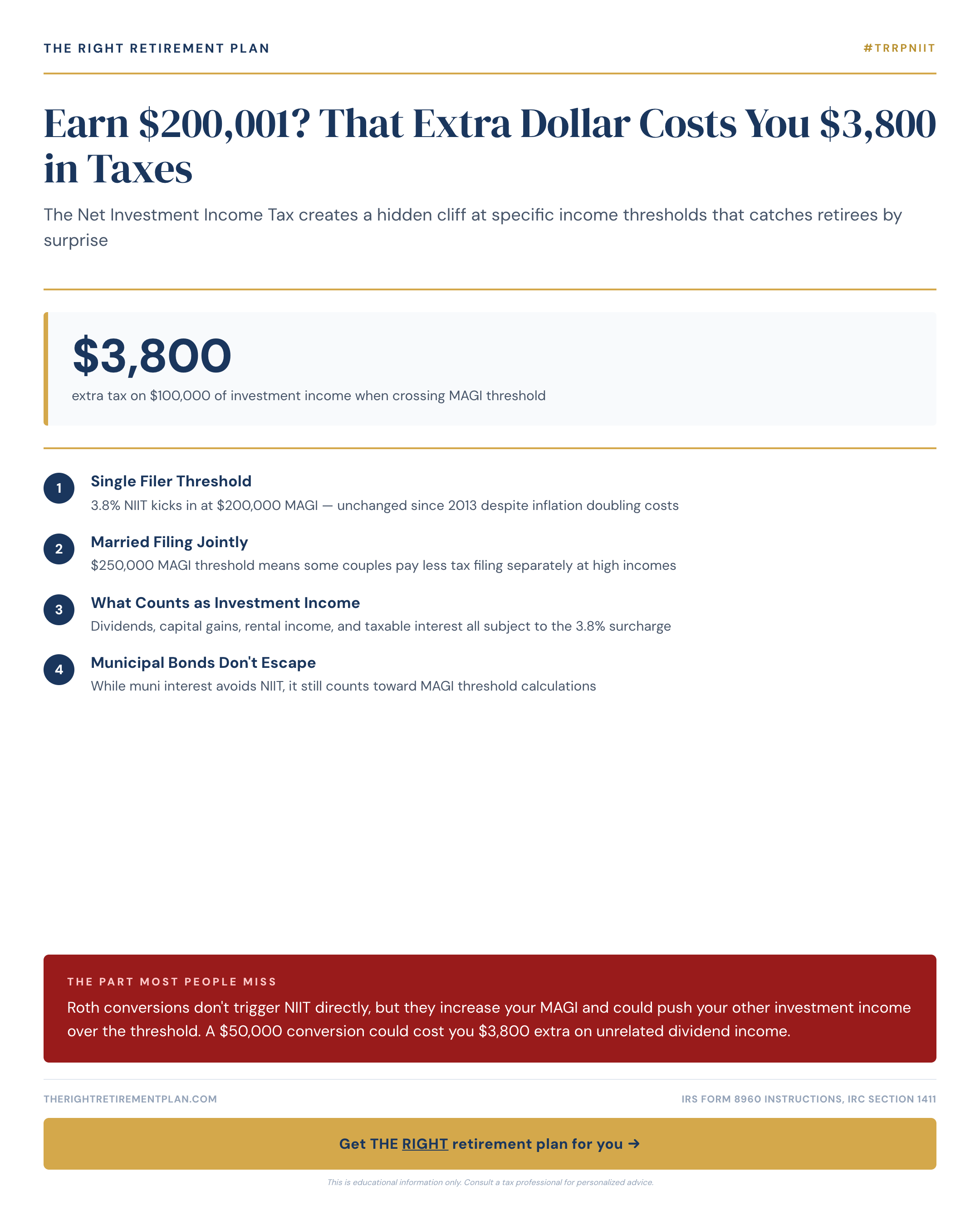

The Net Investment Income Tax (NIIT) creates one of retirement's most expensive surprises. Cross the $200,000 income threshold as a single filer (or $250,000 married filing jointly), and you'll owe an additional 3.8% tax on investment income like dividends, capital gains, and rental income.

Here's where it gets costly: that extra dollar doesn't just cost you regular income tax. It can trigger NIIT on all your investment income, potentially adding thousands to your tax bill.

For example, if you earn $199,999 in modified adjusted gross income (MAGI) plus $100,000 in investment income, you owe zero NIIT. But earn $200,001 plus that same $100,000 in investment income? You'll pay 3.8% on the entire investment amount—an extra $3,800 in taxes.

How Retirement Strategies Can Backfire

The net investment income tax becomes particularly tricky when planning retirement moves. Roth conversions, while valuable for long-term tax planning, increase your MAGI and can inadvertently push you over the NIIT threshold.

Consider this scenario: You're a Maryland retiree with $180,000 in pension and Social Security income, planning a $50,000 Roth conversion. You also receive $75,000 annually in dividend income from your investment portfolio.

Without the conversion, your total income stays under $200,000—no NIIT applies. But that $50,000 Roth conversion pushes your MAGI to $230,000, triggering NIIT on your entire $75,000 in dividend income. The result? An unexpected $2,850 tax bill on top of the conversion taxes.

Other retirement decisions that can trigger the threshold include:

- Taking larger IRA distributions

- Selling appreciated real estate

- Realizing capital gains from rebalancing portfolios

Strategic Planning Makes the Difference

Smart retirement planning means understanding these tax cliffs before making major financial moves. Consider spreading large Roth conversions across multiple years, timing asset sales strategically, or adjusting your investment income sources.

Working with advisors who understand these nuances—whether you're in Annapolis or anywhere across the Mid-Atlantic—can save you thousands in unnecessary taxes while still achieving your retirement goals.

If you want personalized guidance on how the Net Investment Income Tax might affect your retirement strategy, consider taking our Retire Ready Score for insights tailored to your situation.