The Windfall Elimination Provision (WEP) represents one of Social Security's most misunderstood rules, catching thousands of retirees off guard each year. If you've worked in both private sector jobs and government positions with non-covered pensions, WEP could significantly reduce your expected Social Security benefits.

How WEP Slashes Your Benefits

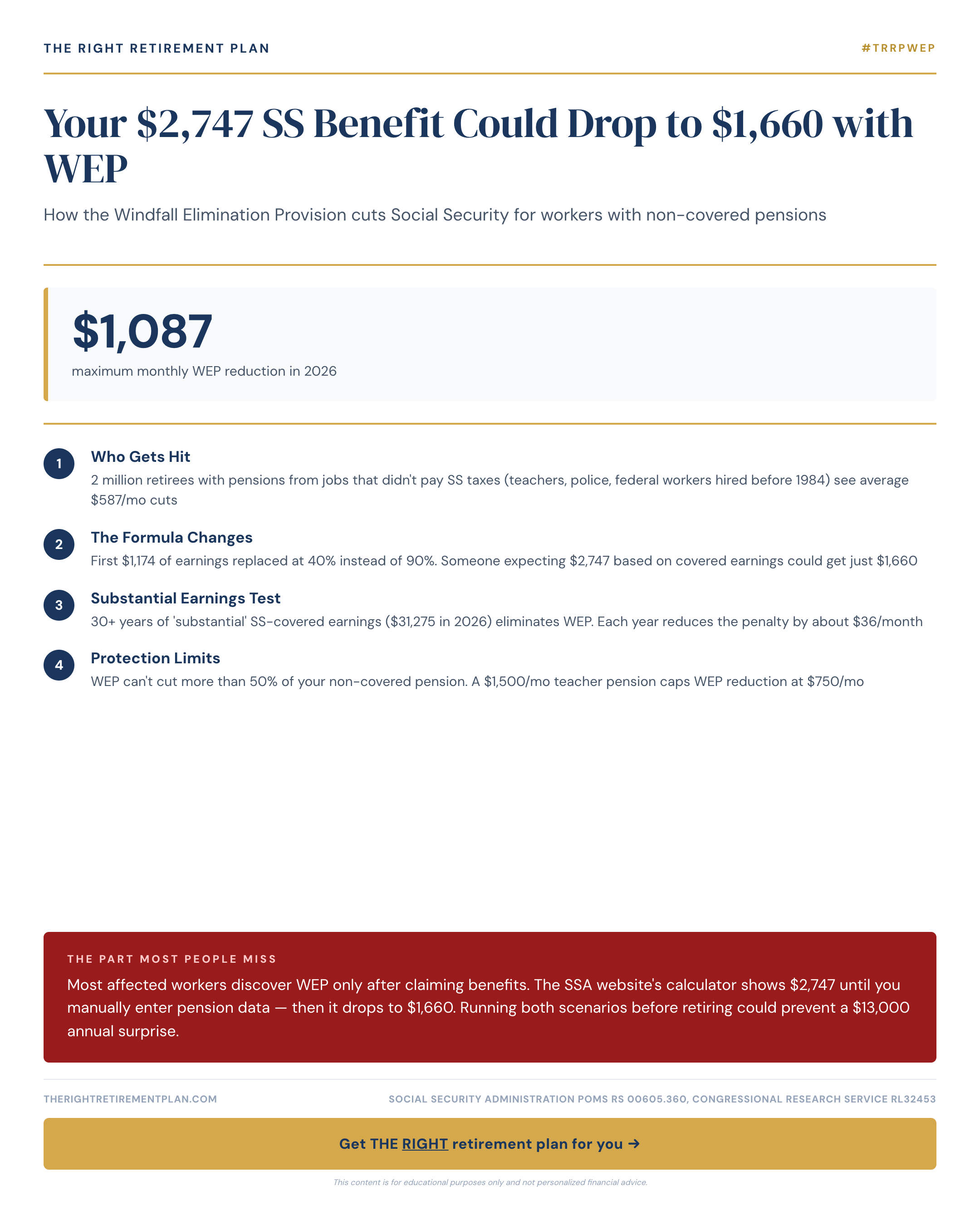

WEP affects workers who receive pensions from employment where they didn't pay Social Security taxes — typically government jobs, some railroad positions, or certain overseas employment. The provision can reduce your Social Security benefit by up to $587 per month in 2026.

Here's the shocking reality: Many affected workers only discover WEP after claiming benefits. The Social Security Administration's online calculator initially shows your full benefit amount — perhaps $2,747 monthly. But enter your pension information, and that figure can plummet to $1,660, creating an unexpected $13,000 annual shortfall.

The reduction depends on your "years of substantial earnings" under Social Security. If you have fewer than 20 years of substantial earnings (defined as $29,700 or more in 2026), you'll face the maximum WEP reduction. Workers with 30 or more years of substantial earnings avoid WEP entirely.

Who Gets Hit Hardest

WEP disproportionately affects specific groups:

- Teachers who worked in private sector jobs before entering education

- Federal employees hired before 1984

- State and local government workers in non-Social Security covered positions

- Military personnel with civilian government careers

Maryland retirees in government positions often fall into this category, particularly those who split careers between private sector work and state employment.

Planning Strategies That Work

Smart planning can minimize WEP's impact on your retirement security. Consider these approaches:

Timing matters: If you're close to reaching 30 years of substantial earnings, working a few additional years in Social Security-covered employment could eliminate WEP entirely.

Run the numbers early: Use Social Security's detailed calculator with your pension information well before retirement. Don't rely on the basic estimate.

Coordinate with spousal benefits: WEP affects your own Social Security benefit but doesn't impact spousal or survivor benefits your spouse might receive based on your record.

Understanding WEP rules early prevents costly retirement planning mistakes that compound over decades. If you want personalized guidance on how WEP might affect your specific situation, consider taking our Retire Ready Score for a comprehensive assessment of your retirement readiness.