How Single Premium Immediate Annuities Work

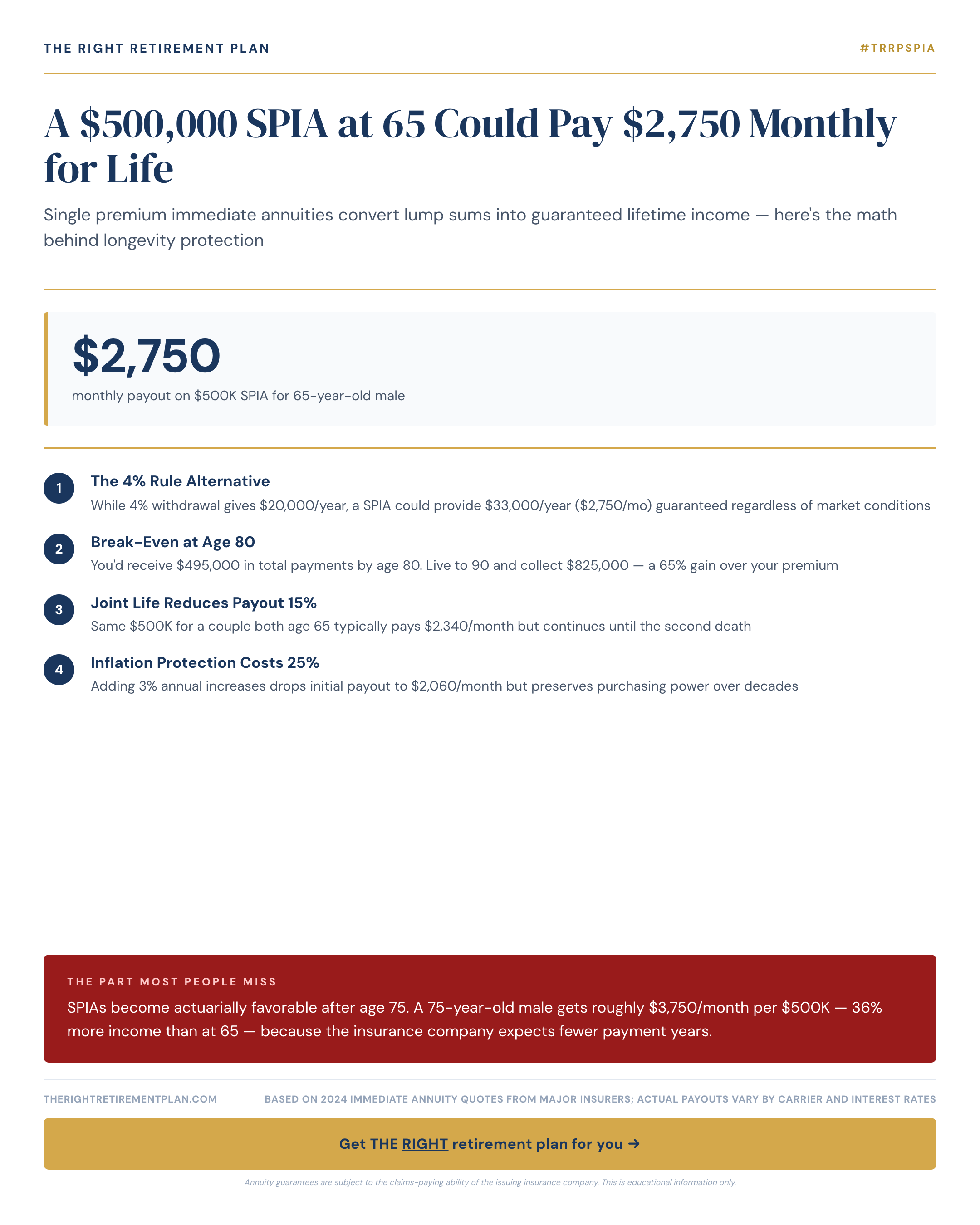

A single premium immediate annuity (SPIA) converts a lump sum into guaranteed monthly income for life. Think of it as purchasing a personal pension. You hand over a chunk of your retirement savings—say $500,000—and the insurance company promises to pay you a fixed amount every month until you die.

At age 65, that $500,000 SPIA typically generates around $2,750 monthly for a male purchaser. The exact amount varies by insurer, current interest rates, and your health status, but this gives you a baseline for planning purposes.

The appeal is straightforward: no market risk, no management fees, and no worrying about outliving your money. Maryland retirees often appreciate this certainty, especially those who lived through the 2008 financial crisis or recent market volatility.

The Age Factor Changes Everything

Here's where SPIA timing gets interesting. That same $500,000 investment becomes much more generous as you age. A 75-year-old male receives roughly $3,750 monthly—36% more income than the 65-year-old.

Why the dramatic difference? Insurance companies use life expectancy tables. They expect to make payments to a 65-year-old for approximately 20 years, but only 12-15 years for a 75-year-old. Shorter payment period equals higher monthly amounts.

This creates a genuine dilemma:

- Buy early for longer income security

- Wait for higher monthly payments but fewer total years

- Risk dying before purchase (getting zero benefit)

Making the Right Choice for You

Your SPIA decision depends on several personal factors. Family longevity history matters—if your parents lived to 95, buying at 65 might make sense. Current health, other income sources, and risk tolerance all play roles.

Consider using SPIAs for a portion of your portfolio rather than all-or-nothing approaches. Many financial advisors in the Annapolis area suggest covering basic living expenses with guaranteed sources (Social Security plus a SPIA), then investing remaining assets for growth.

The 2026 landscape offers some attractive options, with interest rates higher than the previous decade making immediate annuities more compelling than they've been in years.

If you want personalized guidance on whether a SPIA fits your retirement picture, consider taking our Retire Ready Score for insights tailored to your situation.