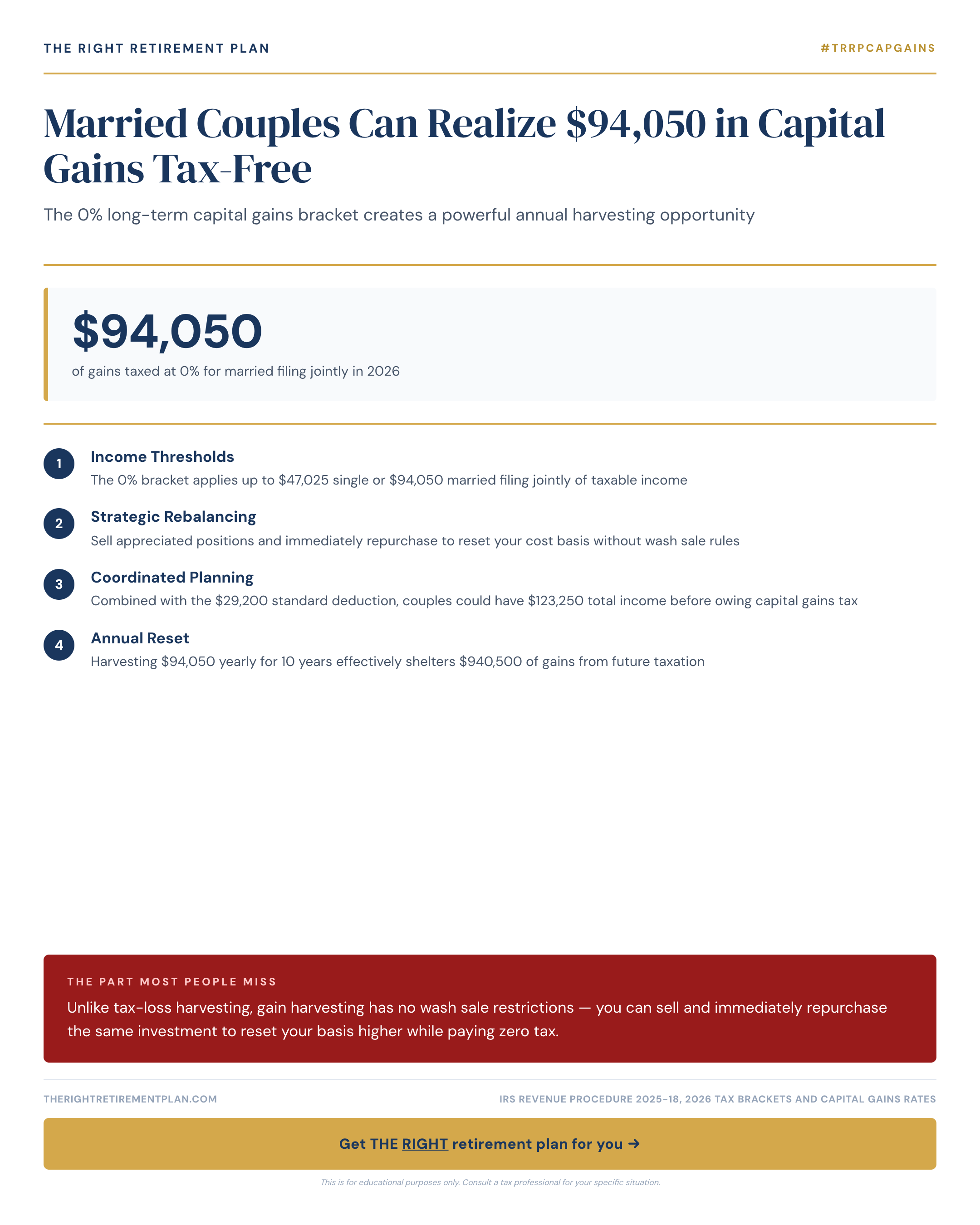

The 0% long-term capital gains bracket represents one of retirement planning's best-kept secrets. For 2026, married couples filing jointly can realize up to $94,050 in capital gains without paying a penny in federal tax — a strategy called gain harvesting that many pre-retirees overlook.

How the 0% Capital Gains Bracket Works

Unlike ordinary income, long-term capital gains (investments held over one year) receive preferential tax treatment. The 0% bracket applies to married couples with taxable income up to $94,050 in 2026, creating a substantial tax-free zone for investment gains.

Here's what makes gain harvesting particularly powerful:

- No wash sale restrictions — unlike tax-loss harvesting, you can sell and immediately repurchase the same investment

- Basis reset — your new cost basis becomes the higher sale price, reducing future tax liability

- Annual opportunity — you can repeat this strategy every year within the bracket limits

For single filers, the 2026 limit is $47,025, still providing meaningful tax savings for individual retirement accounts.

Strategic Implementation for Retirees

Smart capital gains tax planning becomes crucial during the early retirement years when you have more control over your income. Many Maryland retirees find themselves in lower tax brackets after leaving high-earning careers, creating the perfect window for gain harvesting.

Consider this example: A retired couple with $60,000 in Social Security and pension income could harvest an additional $34,050 in capital gains tax-free, staying within the bracket limit.

Key timing considerations include:

- Bridge years — the gap between retirement and required minimum distributions (RMDs)

- Roth conversion coordination — balance gain harvesting with Roth IRA conversions

- Healthcare subsidies — higher income might affect Affordable Care Act premium tax credits

Effective retirement tax strategies require viewing your entire financial picture holistically. The 0% capital gains bracket works best when integrated with Social Security timing, Roth conversions, and withdrawal sequencing from different account types.

Getting these coordination details wrong can cost tens of thousands over retirement, but the good news is these mistakes are completely avoidable with proper planning.

If you want to see how capital gains harvesting fits into your specific retirement strategy, take our free Retire Ready Score — a brief assessment that evaluates your current plan across income, taxes, healthcare, and protection.