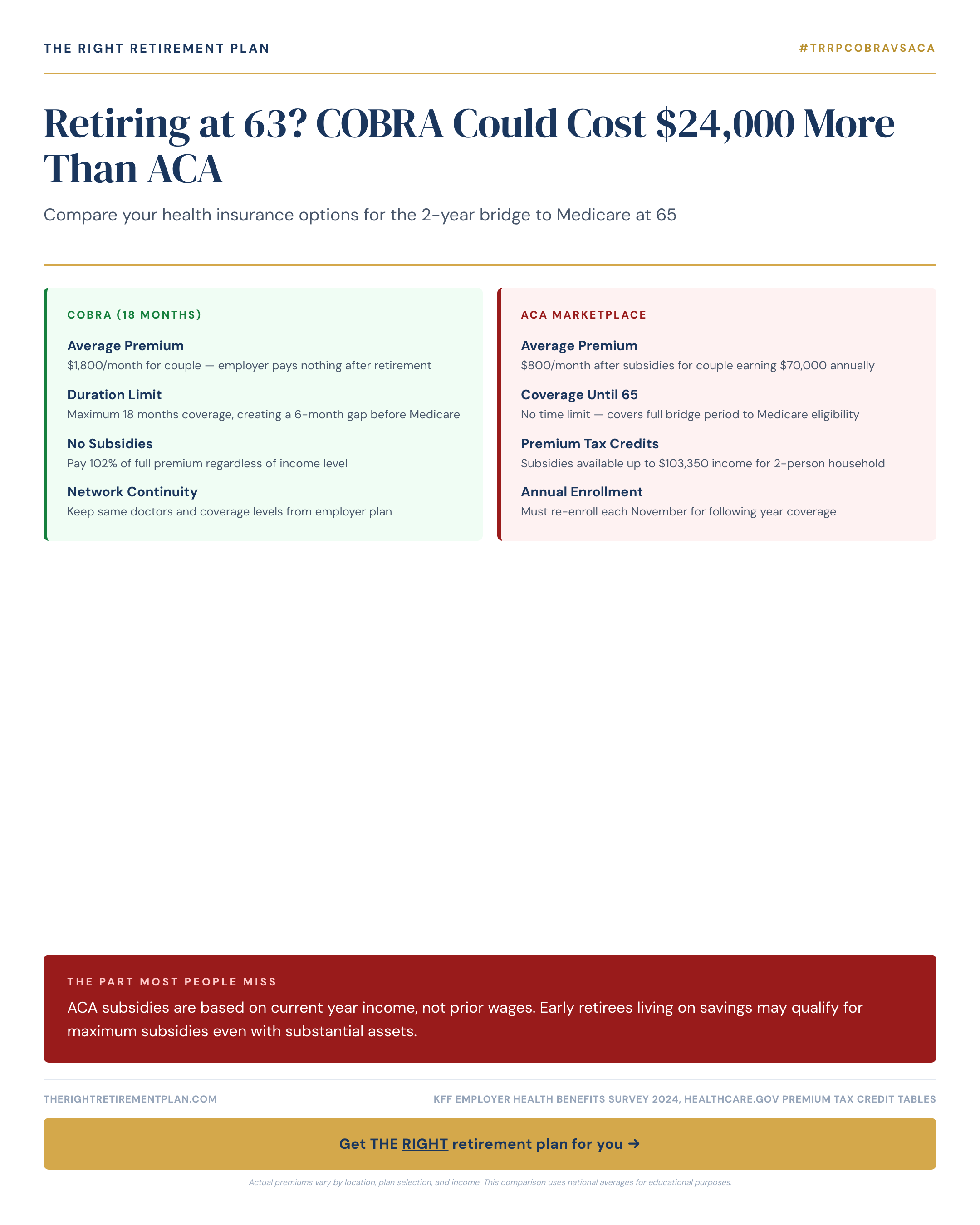

When you retire at 63, you face a challenging two-year gap before Medicare eligibility begins at 65. During this period, retiring at 63 health insurance becomes a critical financial decision that could save or cost you tens of thousands of dollars.

COBRA vs. ACA Marketplace: The $24,000 Difference

COBRA continuation coverage typically costs $800-1,200 monthly for individual coverage, since you pay the full premium plus a 2% administrative fee. Over 24 months, that's $19,200-28,800 out of pocket.

ACA marketplace plans offer a dramatically different picture. With income-based subsidies, many early retirees pay just $200-400 monthly for comparable coverage. The potential savings? Up to $24,000 over the two-year bridge to Medicare.

The key difference lies in how early retirement health coverage subsidies work. Unlike COBRA, which bases costs on your former employer's group rates, ACA subsidies depend entirely on your current year income.

The Income Strategy Most Miss

Here's where early retirees gain a huge advantage: ACA subsidies are based on current income, not your previous salary or accumulated savings. If you're living off retirement accounts, investment income, or savings, your reportable income may be surprisingly low.

For 2026, ACA premium tax credits are available for individuals earning up to $58,320 (400% of federal poverty level). Many Maryland retirees discover their post-employment income falls well within this range, qualifying them for substantial subsidies regardless of their net worth.

retirement healthcare options become even more attractive when you consider:

- Maximum out-of-pocket limits provide catastrophic protection

- Prescription drug coverage is included

- Preventive care is covered at 100%

- Network flexibility often exceeds COBRA options

Making the Right Choice

Compare all available options before your COBRA election period expires. Consider your anticipated medical needs, prescription requirements, and preferred providers. Don't forget to account for potential subsidy eligibility when calculating true costs.

Getting this decision right protects both your health and retirement savings during a vulnerable period. If you want personalized guidance on how these healthcare options fit into your broader retirement strategy, consider taking our Retire Ready Score for a comprehensive assessment of your retirement readiness.