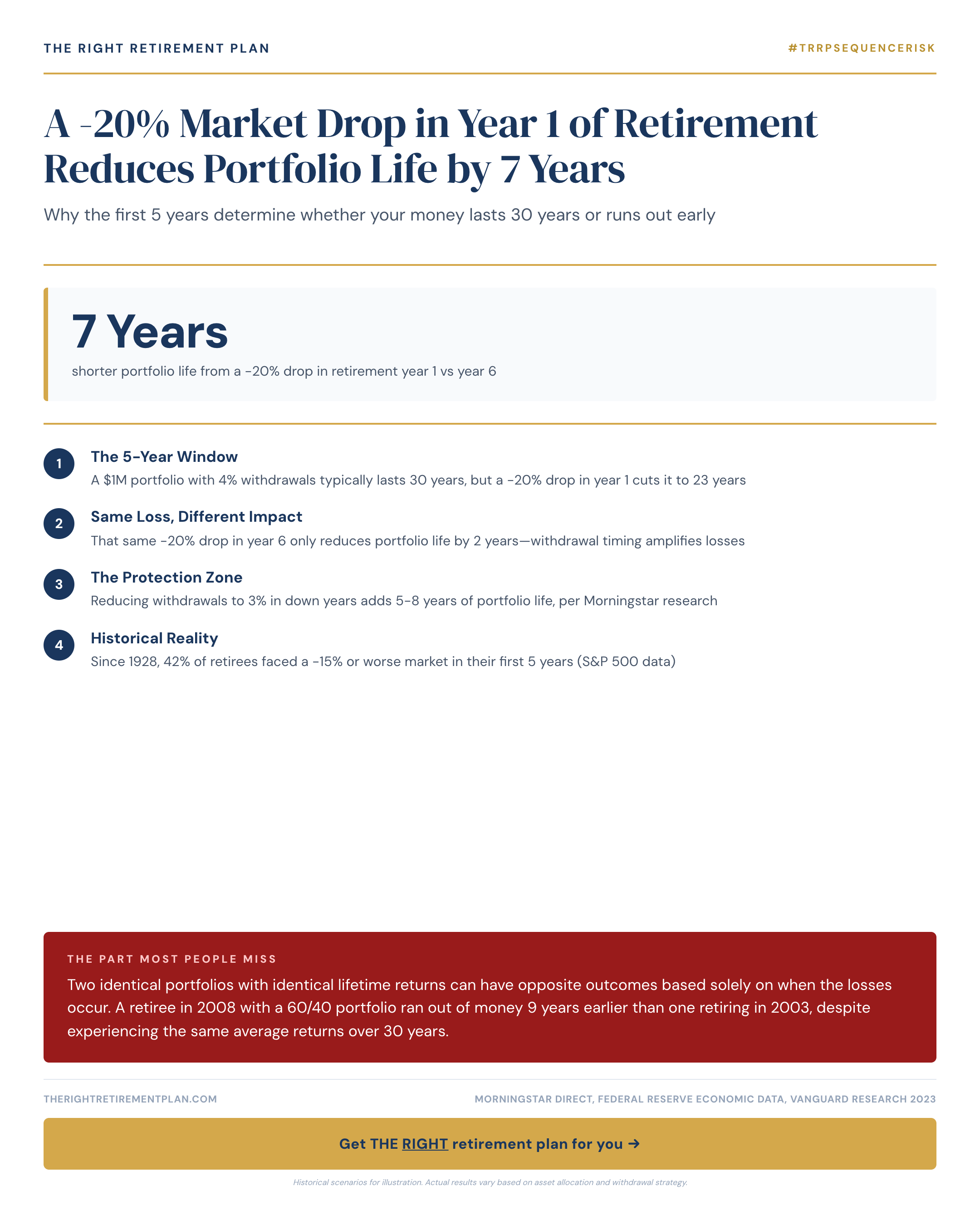

Why Market Timing Matters More in Retirement

The sequence of returns—when gains and losses occur—becomes critically important once you start withdrawing money from your portfolio. A 20% market drop in year 1 of retirement can reduce your portfolio's lifespan by up to 7 years, even if your long-term average returns remain solid.

This phenomenon, called sequence of returns risk, explains why two retirees with identical portfolios and identical lifetime returns can have drastically different outcomes. The timing of market volatility makes all the difference when you're taking regular withdrawals.

Consider this stark example: A retiree who started in 2008 with a traditional 60/40 portfolio saw their money run out 9 years earlier than someone who retired in 2003—despite both experiencing the same average returns over 30 years. The 2008 retiree faced the financial crisis immediately, while the 2003 retiree enjoyed several good years before the downturn.

The Mathematics Behind Portfolio Depletion

When markets drop early in retirement, you're forced to sell more shares to maintain your withdrawal rate. Those shares are gone forever and can't participate in future market recovery. This creates a mathematical hole that becomes nearly impossible to climb out of.

For 2026, many financial planners recommend having 1-2 years of expenses in cash or short-term bonds before retiring. This creates a buffer against early market volatility, allowing your portfolio time to potentially recover before you need to sell at depressed prices.

Maryland retirees and others approaching retirement should also consider:

- Flexible withdrawal strategies that adjust based on market performance

- Diversification beyond traditional stock/bond allocations

- Healthcare cost planning (average couple needs $315,000 for medical expenses in retirement)

- Social Security optimization timing

Your retirement success depends on understanding these sequence of returns risks before you retire, not after. Small adjustments to timing, withdrawal rates, or asset allocation can mean the difference between financial security and running short of money in your later years.

If you want personalized guidance on how these principles apply to your specific situation, consider taking our Retire Ready Score assessment.